US Macro Daily(Beta Mode)

Stocks Rally on Iran Peace Hopes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,886.24 | +1.02% |

| Nasdaq 100 | 25,383.72 | +1.06% |

| Dow Jones | 48,218.25 | +0.63% |

| Russell 2000 | 2,670.49 | +1.52% |

| USD/JPY | 158.82 | -0.54% |

| EUR/USD | 1.18 | +1.06% |

| GBP/USD | 1.36 | +1.23% |

| Gold | 4,791.60 | +1.04% |

| WTI Crude | 97.31 | -1.79% |

| Bitcoin | 74,423.45 | -0.08% |

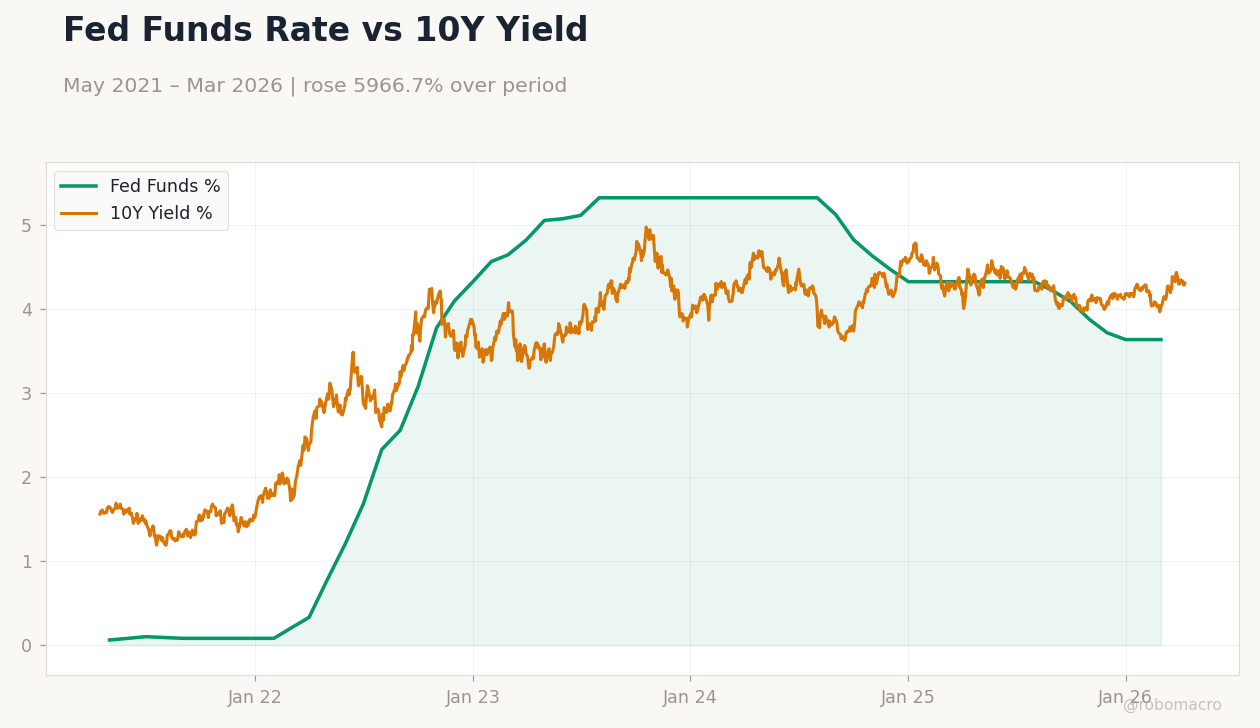

| US 2Y Treasury | 3.81% | +0.79% |

| US 10Y Treasury | 4.31% | +0.47% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

WTI Crude Oil Price | Type: macro_line | WTI $/bbl: 114 (2026-04-06) | Range: 55.44–123.6 | Trend(6pt): 63.42,106.1,89.26,73.79,113.2,114

WTI Crude Oil Price | Type: macro_line | WTI $/bbl: 114 (2026-04-06) | Range: 55.44–123.6 | Trend(6pt): 63.42,106.1,89.26,73.79,113.2,114

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- US equities surged over 1% as investors bet on de-escalation in Iran conflict, erasing war-related losses.

- Treasury yields rose modestly amid risk-on sentiment, while oil dipped on tanker rerouting reports.

- Fed officials signal caution on rates, with Treasury Secretary Bessent advocating a wait-and-see approach.

Yesterday's Recap

US markets saw broad gains with the S&P 500 climbing 1.02% to 6,886.24, driven by optimism over potential US-Iran peace proposals that could ease energy disruptions. The Nasdaq 100 advanced 1.06% to 25,383.72, buoyed by tech sector strength, while the Dow Jones rose 0.63% to 48,218.25 and Russell 2000 jumped 1.52% to 2,670.49, reflecting small-cap outperformance. Treasury yields edged higher, with the 2-year up 0.79% to 3.81% and 10-year up 0.47% to 4.31%, as safe-haven demand waned.

Currency moves favored a weaker dollar, with EUR/USD up 1.06% to 1.18 and GBP/USD up 1.23% to 1.36, while USD/JPY fell 0.54% to 158.82. Gold rose 1.04% to 4,791.60 amid lingering geopolitical risks, but WTI crude dropped 1.79% to 97.31 on reports of tankers avoiding the Strait of Hormuz. Bitcoin held steady, dipping just 0.08% to 74,423.45, tracking equity resilience.

No major US data releases occurred, allowing markets to focus on global news flow.

The Day Ahead

With no scheduled US economic releases tomorrow, attention turns to ongoing geopolitical developments, particularly any updates on US-Iran negotiations that could influence energy markets and risk appetite. Markets may digest corporate earnings as the season ramps up, with potential volatility from airline merger talks involving United and American. Treasury auctions or ad-hoc Fed comments could emerge, especially following recent Powell-Trump discussions on economic policy.

Broader sentiment might hinge on oil price movements amid the impending US blockade on Hormuz. Investors should monitor currency pairs for shifts in dollar strength tied to global reserve trends. Overall, a quiet calendar could amplify reactions to news headlines.

Other Economic Notes

Broader US economic themes highlight persistent inflation pressures, with verified CPI YoY at 2.31% signaling moderation but sticky services components amid wage growth. Unemployment stands at 4.30%, supporting a resilient labor market that tempers recession fears yet complicates Fed easing paths. Tariff impacts from recent policies are confirmed by Fed research to have driven excess inflation in 2025, underscoring trade's role in price dynamics.