US Macro Daily(Beta Mode)

Stocks Rally Amid Mixed Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,022.95 | +0.80% |

| Nasdaq 100 | 26,204.58 | +1.40% |

| Dow Jones | 48,463.72 | -0.15% |

| Russell 2000 | 2,713.66 | +0.30% |

| USD/JPY | 158.98 | +0.12% |

| EUR/USD | 1.18 | -0.13% |

| GBP/USD | 1.35 | -0.23% |

| Gold | 4,830.60 | +0.64% |

| WTI Crude | 89.28 | -2.20% |

| Bitcoin | 74,341.17 | -0.62% |

| US 2Y Treasury | 3.76% | -0.53% |

| US 10Y Treasury | 4.26% | -0.93% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Existing Home Sales | 4.1m | 4.1m | 4.0m |

| Existing Home Sales Month-over-Month | 2.70 | - | -3.60 |

| Speech by Fed's Miran | - | - | - |

| ADP Employment Change Weekly | 26,000 | - | 39,000 |

| Producer Price Index Month-over-Month | 0.50 | 1.10 | 0.50 |

| Core Producer Price Index Month-over-Month | 0.30 | 0.50 | 0.10 |

| Fed Goolsbee Speech | - | - | - |

| Speech by Fed's Barr | - | - | - |

| Speech by Fed's Collins | - | - | - |

| API Weekly Crude Oil Stocks | 3.7m | -1.3m | 6.1m |

US 10Y Treasury Yield | Type: macro_line | 10-Year Treasury Yield: 4.26 (2026-04-14) | Range: 1.19–4.98 | Trend(6pt): 1.61,2.93,4.7,4.77,4.31,4.26 | Fed Funds Rate: 3.64 (2026-03-01) | Range: 0.06–5.33 | Trend(5pt): 0.06,1.68,5.33,4.64,3.64

US 10Y Treasury Yield | Type: macro_line | 10-Year Treasury Yield: 4.26 (2026-04-14) | Range: 1.19–4.98 | Trend(6pt): 1.61,2.93,4.7,4.77,4.31,4.26 | Fed Funds Rate: 3.64 (2026-03-01) | Range: 0.06–5.33 | Trend(5pt): 0.06,1.68,5.33,4.64,3.64

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Philadelphia Fed Manufacturing Index | 18.10 | 10 | 04:30 |

| Weekly Jobless Claims | 219,000 | 215,000 | 04:30 |

| Speech by Fed's Williams | - | - | 04:35 |

| Industrial Production Month-over-Month | 0.20 | 0.10 | 05:15 |

| Speech by Fed's Miran | - | - | 06:35 |

- US stocks climbed with S&P 500 +0.80% to 7,022.95 and Nasdaq +1.40% to 26,204.58, buoyed by positive manufacturing signals despite housing weakness.

- Treasury yields declined, 10Y to 4.26% (-0.93%) on softer inflation data, while WTI crude fell 2.20% to $89.28 amid inventory builds.

- Fed's Beige Book noted Iran war sparking business caution, but NY Empire index beat expectations sharply.

Yesterday's Recap

US existing home sales missed at 3.98 million annualized, below 4.06 million consensus and down 3.6% month-over-month from prior 2.7%, highlighting housing softness amid elevated rates, though MBA 30-year mortgage rate dipped to 6.42% from 6.51%. Producer prices increased 0.5% month-over-month, matching previous but under 1.1% forecast, with core PPI slowing to 0.1% versus 0.5% expected, alleviating inflation worries and aiding bond rallies. NY Empire State Manufacturing Index jumped to 11.0, surpassing -0.5 consensus and -0.2 prior, pointing to regional factory strength.

Import prices rose 0.8% month-over-month, below 2% estimate and prior 0.9%, while export prices gained 1.6% against 1.5% expected, showing tempered trade pressures. ADP weekly employment rose to 39,000 from 26,000, indicating solid hiring. API crude stocks built by 6.1 million barrels versus -1.3 million consensus, weighing on oil.

Markets advanced: S&P 500 +0.80%, Nasdaq +1.40%, Dow -0.15%, Russell 2000 +0.30%; USD/JPY +0.12% to 158.98, EUR/USD -0.13% to 1.18, gold +0.64% to 4,830.60, Bitcoin -0.62% to 74,341.17. Fed speeches by Miran, Goolsbee, Barr (twice), and Collins stressed data-driven policy without altering rate expectations.

The Day Ahead

Philadelphia Fed Manufacturing Index at 4:30 ET, consensus 10 from prior 18.1, could lift sentiment if it confirms expansion. Other potential releases include housing starts and building permits around 8:30 ET, with starts eyed at 1.42 million versus 1.44 million prior, and permits at 1.51 million, gauging sector health. Leading Index at 10:00 ET forecast to drop 0.3%, signaling slowdown risks.

EIA crude inventories at 10:30 ET, consensus -1.2 million barrels, may sway energy amid geopolitical tensions.

Other Economic Notes

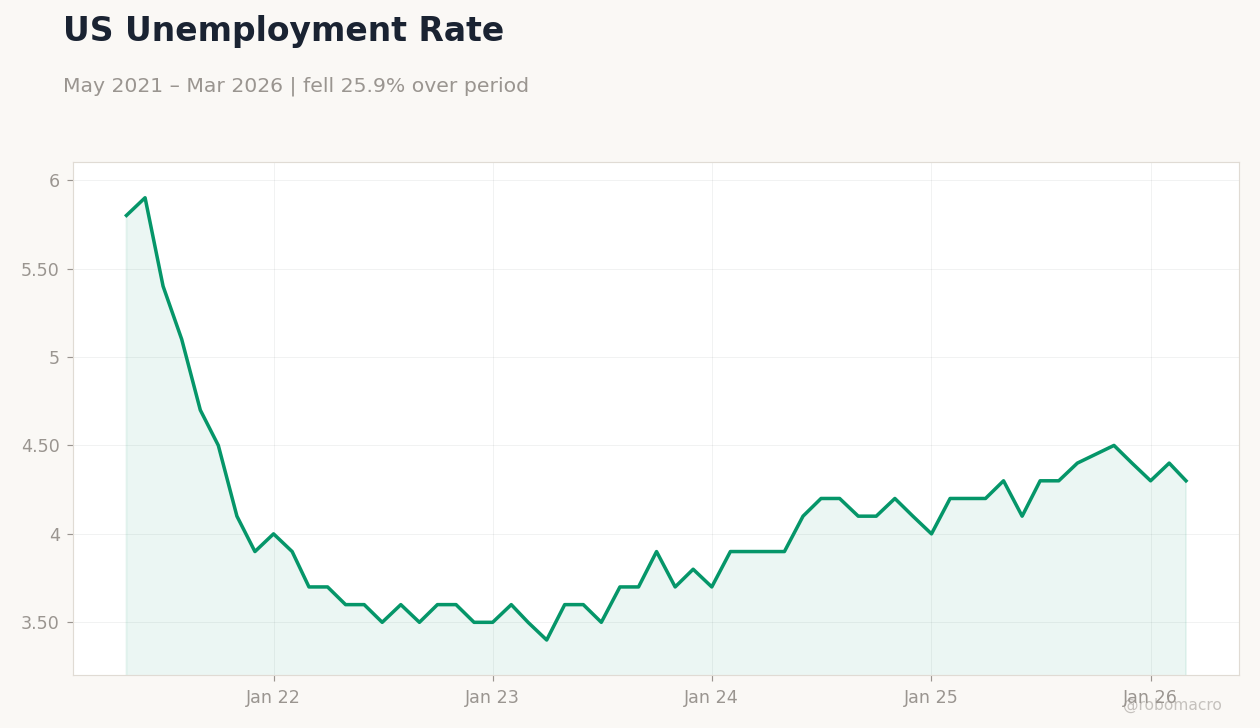

US economy displays mixed resilience, with manufacturing beats like NY Empire contrasting weak housing, as unemployment stands at 4.30% and CPI YoY at 2.31% bolsters soft landing views. IMF warns of rising US debt, calling for cuts equaling 4% of GDP to curb fiscal imbalances and contain spending. Consumer strength persists via job data, but Iran war uncertainties may hinder investment, per Beige Book.