US Macro Daily(Beta Mode)

Stocks Rally, Oil Jumps

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,126.06 | +1.20% |

| Nasdaq 100 | 26,672.43 | +1.29% |

| Dow Jones | 49,447.43 | +1.79% |

| Russell 2000 | 2,776.90 | +2.11% |

| USD/JPY | 158.90 | -0.19% |

| EUR/USD | 1.18 | +0.01% |

| GBP/USD | 1.35 | +0.05% |

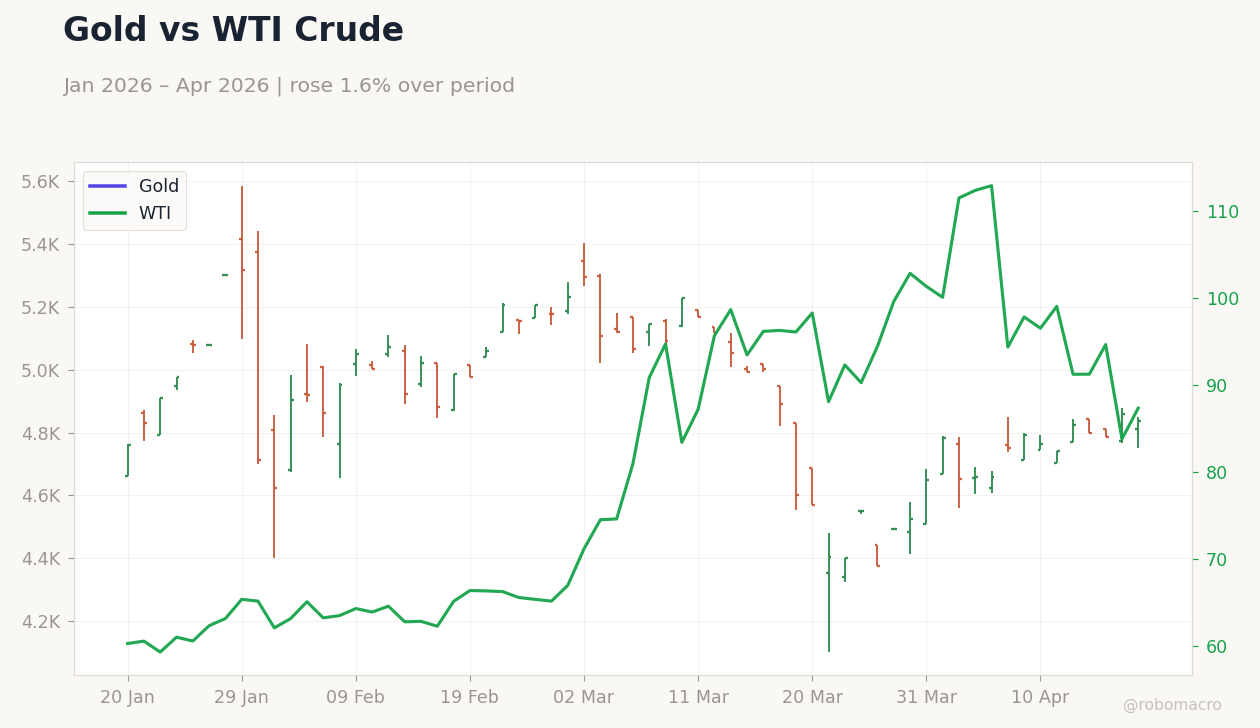

| Gold | 4,835.70 | -0.45% |

| WTI Crude | 87.40 | +4.23% |

| Bitcoin | 76,437.13 | +3.49% |

| US 2Y Treasury | 3.78% | +0.53% |

| US 10Y Treasury | 4.32% | +0.70% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

US WTI Crude Oil Price | Type: macro_line | WTI Crude ($/Barrel): 100.7 (2026-04-13) | Range: 55.44–123.6 | Trend(6pt): 61.34,99.59,85.89,73.99,99.62,100.7

US WTI Crude Oil Price | Type: macro_line | WTI Crude ($/Barrel): 100.7 (2026-04-13) | Range: 55.44–123.6 | Trend(6pt): 61.34,99.59,85.89,73.99,99.62,100.7

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-04-21) | |||

| ADP Employment Change Weekly | 39,000 | - | 04:15 |

| Retail Sales Month-over-Month | 0.60 | 1.40 | 04:30 |

| Retail Sales Control Group Month-over-Month | 0.50 | 0.20 | 04:30 |

| Retail Sales Excluding Autos Month-over-Month | 0.50 | 1.40 | 04:30 |

| Business Inventories Month-over-Month | -0.10 | 0.30 | 06:00 |

| Pending Home Sales Month-over-Month | 1.80 | 0.10 | 06:00 |

| Pending Home Sales Year-over-Year | -0.80 | - | 06:00 |

| Speech by Fed's Waller | - | - | 10:30 |

| API Weekly Crude Oil Stocks | 6.1m | -1m | 12:30 |

- US equities climbed broadly, with Dow up 1.79% and Russell 2000 leading at 2.11%, amid easing geopolitical tensions.

- WTI crude surged 4.23% to $87.40, while Treasury yields rose, with 10Y at 4.32% (+0.70%).

- Dollar weakened slightly against yen, but gold dipped 0.45% as risk appetite returned.

Yesterday's Recap

US markets posted strong gains on April 19, with the S&P 500 rising 1.20% to 7,126.06, driven by tech and cyclical sectors amid reduced Middle East risks. The Nasdaq 100 advanced 1.29% to 26,672.43, fueled by AI enthusiasm, while the Dow Jones jumped 1.79% to 49,447.43 on industrial strength. Small caps outperformed as the Russell 2000 gained 2.11% to 2,776.90, reflecting broader risk-on sentiment.

Treasury yields increased, with the 2Y up 0.53% to 3.78% and 10Y up 0.70% to 4.32%, as investors priced in resilient growth. WTI crude oil rallied 4.23% to $87.40, boosted by Strait of Hormuz reopening, while gold fell 0.45% to 4,835.70 on fading haven demand. The USD/JPY pair eased 0.19% to 158.90, with EUR/USD and GBP/USD edging higher by 0.01% and 0.05%, respectively.

Bitcoin climbed 3.49% to 76,437.13, tracking equity momentum, though no major US data releases occurred to sway sentiment.

The Day Ahead

Tuesday brings key US data, starting with ADP Employment Change at 4:15 ET, expected to show weekly shifts after a prior 39K gain, potentially signaling labor trends. Retail Sales MoM at 4:30 ET is forecast at 1.4% versus prior 0.6%, with Control Group at 0.2% and Ex-Autos at 1.4%, offering insights into consumer spending amid inflation moderation. Business Inventories and Pending Home Sales release at 6:00 ET, with inventories eyed at 0.3% MoM and home sales at 0.1% MoM, highlighting inventory builds and housing demand.

Fed's Waller speaks at 10:30 ET, which could provide guidance on rates, while API Crude Stocks at 12:30 ET consensus -1M barrels may influence energy markets. Wednesday features MBA Mortgage Rate at 3:00 ET after prior 6.42%, alongside EIA inventories at 6:30 ET for crude (-1M consensus) and gasoline. Thursday's Chicago Fed Activity Index at 4:30 ET follows prior -0.11, gauging national growth momentum.

Other Economic Notes

Broader US themes point to sustained growth with CPI YoY at 2.31% as of April 2025, supporting disinflation progress toward the Fed's target. Unemployment at 4.30% as of March 2026 reflects a stable labor market, though risks from geopolitical shifts could pressure supply chains. Corporate earnings revisions, led by one firm accounting for half of S&P 500 upgrades since the Iran conflict, underscore narrow market drivers amid record highs.