US Macro Daily(Beta Mode)

Retail Sales Beat, Stocks Ease

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,109.14 | -0.24% |

| Nasdaq 100 | 26,590.34 | -0.31% |

| Dow Jones | 49,442.56 | -0.01% |

| Russell 2000 | 2,792.96 | +0.58% |

| USD/JPY | 159.06 | -0.06% |

| EUR/USD | 1.18 | +0.25% |

| GBP/USD | 1.35 | +0.27% |

| Gold | 4,788.40 | -0.38% |

| WTI Crude | 87.18 | -2.71% |

| Bitcoin | 76,060.02 | +0.25% |

| US 2Y Treasury | 3.71% | -1.85% |

| US 10Y Treasury | 4.26% | -1.39% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 40,250 | - | 54,750 |

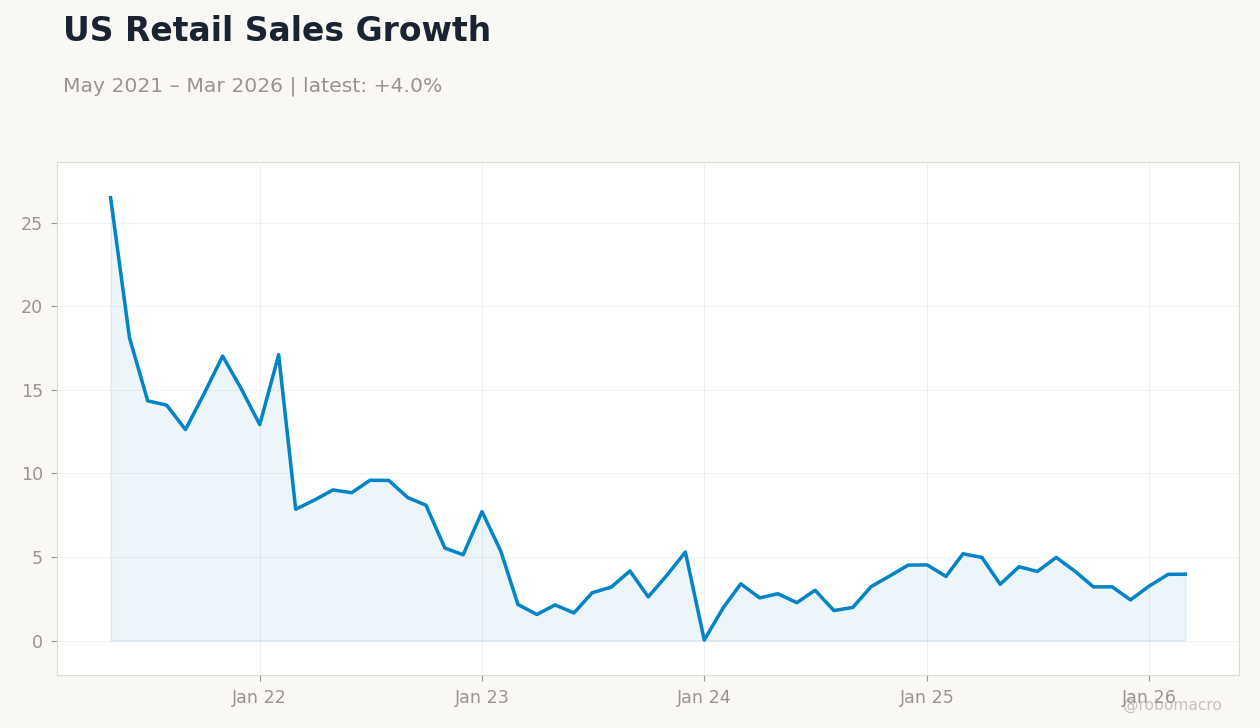

| Retail Sales Month-over-Month | 0.60 | 1.40 | 1.70 |

| Retail Sales Control Group Month-over-Month | 0.50 | 0.20 | 0.70 |

| Retail Sales Excluding Autos Month-over-Month | 0.50 | 1.40 | 1.90 |

US Nonfarm Payrolls | Type: macro_line | Nonfarm Payrolls (Thous.): 0.1642 (2026-03-01) | Range: 0.07327–9.039 | Trend(6pt): 9.039,4.299,1.846,0.8781,0.2047,0.1642

US Nonfarm Payrolls | Type: macro_line | Nonfarm Payrolls (Thous.): 0.1642 (2026-03-01) | Range: 0.07327–9.039 | Trend(6pt): 9.039,4.299,1.846,0.8781,0.2047,0.1642

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Inventories Month-over-Month | -0.10 | 0.30 | 06:00 |

| Fed Chair Nominee Kevin Warsh Confirmation Hearing | - | - | 06:00 |

| Pending Home Sales Month-over-Month | 1.80 | 0.10 | 06:00 |

| Pending Home Sales Year-over-Year | -0.80 | - | 06:00 |

| Speech by Fed's Waller | - | - | 10:30 |

| API Weekly Crude Oil Stocks | 6.1m | -1m | 12:30 |

- Retail sales exceeded expectations, signaling robust consumer spending amid steady job growth.

- Equity markets dipped slightly, with tech under pressure, while Treasuries rallied on rate cut bets.

- Fed nominee Warsh's hearing looms, alongside upcoming data that could shape policy outlook.

Yesterday's Recap

US retail sales advanced 1.7% month-over-month, surpassing the 1.4% consensus and highlighting resilient consumer demand despite elevated rates. The control group rose 0.7% against a 0.2% forecast, while sales excluding autos climbed 1.9% versus 1.4% expected, boosting Q2 GDP prospects. ADP employment change came in at 54,750, stronger than the prior 40,250, underscoring labor market strength with unemployment at 4.30%.

Major indices closed lower: S&P 500 fell 0.24% to 7,109.14, Nasdaq 100 dropped 0.31% to 26,590.34, and Dow Jones edged down 0.01% to 49,442.56, amid profit-taking in tech. Russell 2000 bucked the trend, rising 0.58% to 2,792.96 on small-cap rotation. Treasury yields declined, with the 2-year falling 1.85% to 3.71% and 10-year dropping 1.39% to 4.26%, as markets priced in softer policy ahead.

WTI crude slid 2.71% to $87.18, while gold dipped 0.38% to $4,788.40, reflecting mixed commodity sentiment.

The Day Ahead

Business inventories are expected to rise 0.3% month-over-month, providing insights into supply chain dynamics and potential GDP drag if below consensus. Pending home sales may edge up 0.1% month-over-month, with year-over-year figures watched for housing recovery signals amid high mortgage rates. Fed Chair nominee Kevin Warsh's confirmation hearing at 6:00 ET could reveal his stance on monetary policy independence, influencing market bets on future rate paths.

Fed Governor Waller's speech at 10:30 ET may offer clues on inflation and labor data, potentially moving Treasury yields. API weekly crude oil stocks, forecasted at -1 million barrels, could impact energy prices if inventories surprise. These events collectively shape near-term views on growth and Fed timing.

Other Economic Notes

UnitedHealth Group's quarterly profit beat estimates, raising its annual forecast and signaling a healthcare sector turnaround amid broader economic resilience, as noted by CEO comments on strong US fundamentals. Wells Fargo's Charlie Scharf described the US economy as "extremely strong," aligning with recent data like robust retail sales and low unemployment at 4.30%, though CPI at 2.31% YoY suggests inflation cooling toward target. Broader themes include fiscal pressures, with states facing borrowing needs and capex slowdowns, potentially weighing on infrastructure spending and regional growth.