US Macro Daily(Beta Mode)

Retail Beats, Stocks Slip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,064.01 | -0.63% |

| Nasdaq 100 | 26,479.47 | -0.42% |

| Dow Jones | 49,149.38 | -0.59% |

| Russell 2000 | 2,764.97 | -1.00% |

| USD/JPY | 159.33 | +0.31% |

| EUR/USD | 1.17 | -0.47% |

| GBP/USD | 1.35 | -0.28% |

| Gold | 4,767.20 | +1.46% |

| WTI Crude | 90.92 | -1.31% |

| Bitcoin | 78,218.59 | +2.44% |

| US 2Y Treasury | 3.72% | +0.27% |

| US 10Y Treasury | 4.26% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 40,250 | - | 54,750 |

| Retail Sales Month-over-Month | 0.70 | 1.40 | 1.70 |

| Retail Sales Control Group Month-over-Month | 0.60 | 0.20 | 0.70 |

| Retail Sales Excluding Autos Month-over-Month | 0.70 | 1.40 | 1.90 |

| Business Inventories Month-over-Month | 0 | 0.30 | 0.40 |

| Fed Chair Nominee Kevin Warsh Confirmation Hearing | - | - | - |

| Pending Home Sales Month-over-Month | 2.50 | 0.10 | 1.50 |

| Pending Home Sales Year-over-Year | -0.80 | - | -1.10 |

| Speech by Fed's Waller | - | - | - |

| API Weekly Crude Oil Stocks | 6.1m | -1m | -4.4m |

US Retail Sales YoY | Type: macro_line | YoY % Change: 3.969 (2026-03-01) | Range: 0.02984–26.51 | Trend(6pt): 26.51,9.593,4.162,3.87,3.268,3.969

US Retail Sales YoY | Type: macro_line | YoY % Change: 3.969 (2026-03-01) | Range: 0.02984–26.51 | Trend(6pt): 26.51,9.593,4.162,3.87,3.268,3.969

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| EIA Weekly Crude Oil Inventory | -913,000 | -1m | 06:30 |

| EIA Weekly Gasoline Inventory | -6.3m | - | 06:30 |

| Thursday (2026-04-23) | |||

| Chicago Fed National Activity Index | -0.11 | - | 04:30 |

| Weekly Jobless Claims | 207,000 | 212,000 | 04:30 |

| S&P Global Composite PMI Flash | 50.30 | - | 05:45 |

| S&P Global Manufacturing PMI Flash | 52.30 | 52.50 | 05:45 |

| S&P Global Services PMI Flash | 49.80 | 50 | 05:45 |

| Friday (2026-04-24) | |||

| Michigan Consumer Sentiment Final | 53.30 | 47.60 | 06:00 |

- Retail sales exceeded forecasts, signaling robust consumer spending amid economic resilience.

- Housing data showed strength with pending sales rising more than expected, despite high rates.

- Markets dipped on profit-taking, while Fed nominee hearing added policy uncertainty.

Yesterday's Recap

US retail sales for March rose 1.7% month-over-month, surpassing the 1.4% consensus and prior 0.7%, driven by broad-based gains excluding autos at 1.9% versus 1.4% expected. The control group advanced 0.7% against a 0.2% forecast, bolstering views of solid consumer demand. Pending home sales climbed 1.5% month-over-month, beating the 0.1% estimate but with year-over-year at -1.1%, reflecting affordability pressures from elevated mortgage rates, which eased slightly to 6.35% per MBA data.

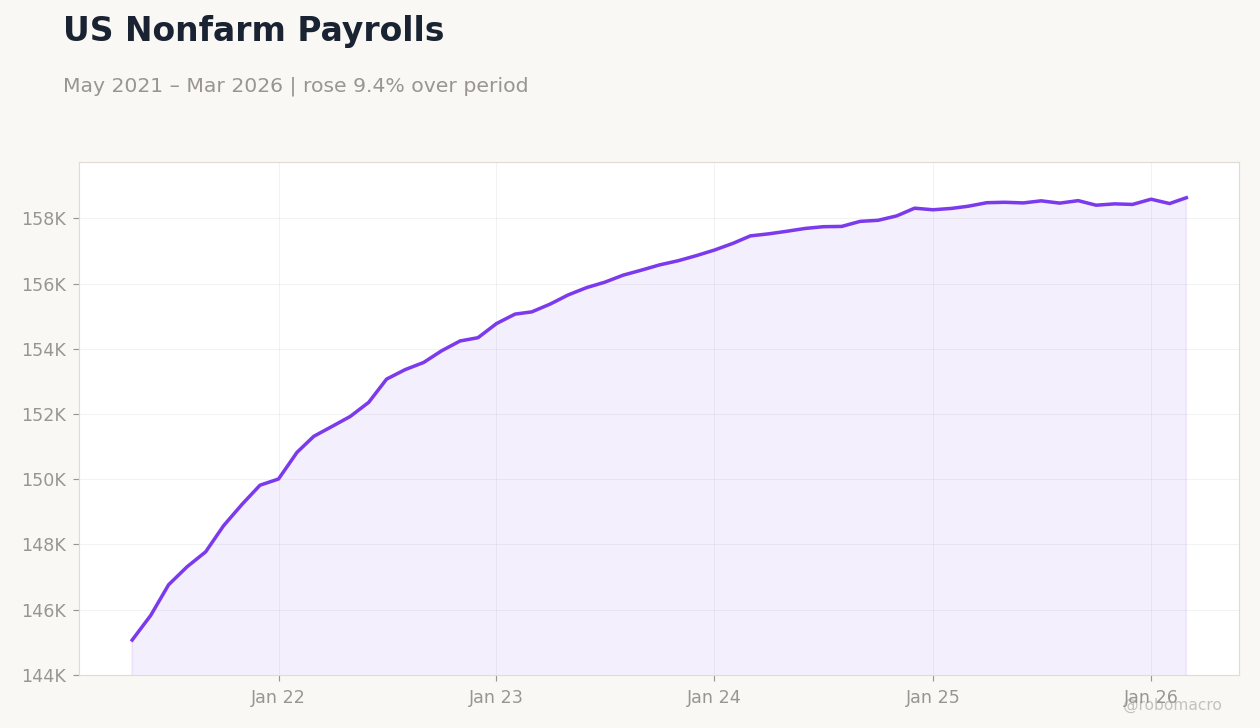

Business inventories increased 0.4% as anticipated, supporting inventory rebuild narratives. ADP weekly employment change jumped to 54,750 from 40,250, hinting at labor market vigor ahead of official payrolls. Equities declined, with S&P 500 down 0.63% to 7,064.01, Nasdaq 100 off 0.42% to 26,479.47, and Russell 2000 falling 1.00% to 2,764.97, amid sector rotation and Iran conflict jitters; Treasury yields were mixed, 2-year up 0.27% to 3.72% while 10-year held at 4.26%.

API crude stocks drew down by 4.4 million barrels, more than the 1 million expected, yet WTI crude slipped 1.31% to $90.92 on global demand concerns.

The Day Ahead

Attention turns to EIA weekly crude oil inventories at 6:30 ET, with consensus expecting a 1 million barrel draw following API's larger decline, potentially influencing energy prices and inflation outlooks. EIA gasoline inventories will also release simultaneously, providing insights into refining activity amid seasonal demand shifts. Thursday brings the Chicago Fed National Activity Index at 4:30 ET, where a reading above the prior -0.11 could affirm economic momentum.

Weekly jobless claims at 4:30 ET are forecast at 212,000 versus prior 207,000, offering a gauge of labor trends. No major Fed speeches are scheduled today, leaving markets to digest yesterday's Waller remarks and Warsh hearing. Broader focus remains on geopolitical risks from Iran tensions, which could sway safe-haven flows into Treasuries and gold.

Other Economic Notes

Broader US economic themes highlight persistent consumer resilience, as evidenced by strong retail figures, yet labor market softening persists with unemployment at 4.30% as of March. (cont...)