US Macro Daily(Beta Mode)

Retail Beats, Stocks Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,137.90 | +1.05% |

| Nasdaq 100 | 26,937.28 | +1.73% |

| Dow Jones | 49,490.03 | +0.69% |

| Russell 2000 | 2,785.38 | +0.74% |

| USD/JPY | 159.70 | +0.21% |

| EUR/USD | 1.17 | -0.49% |

| GBP/USD | 1.35 | -0.18% |

| Gold | 4,706.50 | -0.55% |

| WTI Crude | 94.42 | +1.57% |

| Bitcoin | 77,507.15 | -0.89% |

| US 2Y Treasury | 3.78% | +1.61% |

| US 10Y Treasury | 4.30% | +0.94% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 40,250 | - | 54,750 |

| Retail Sales Month-over-Month | 0.70 | 1.40 | 1.70 |

| Retail Sales Control Group Month-over-Month | 0.60 | 0.20 | 0.70 |

| Retail Sales Excluding Autos Month-over-Month | 0.70 | 1.40 | 1.90 |

| Business Inventories Month-over-Month | 0 | 0.30 | 0.40 |

| Fed Chair Nominee Kevin Warsh Confirmation Hearing | - | - | - |

| Pending Home Sales Month-over-Month | 2.50 | 0.10 | 1.50 |

| Pending Home Sales Year-over-Year | -0.80 | - | -1.10 |

| Speech by Fed's Waller | - | - | - |

| API Weekly Crude Oil Stocks | 6.1m | -1m | -4.4m |

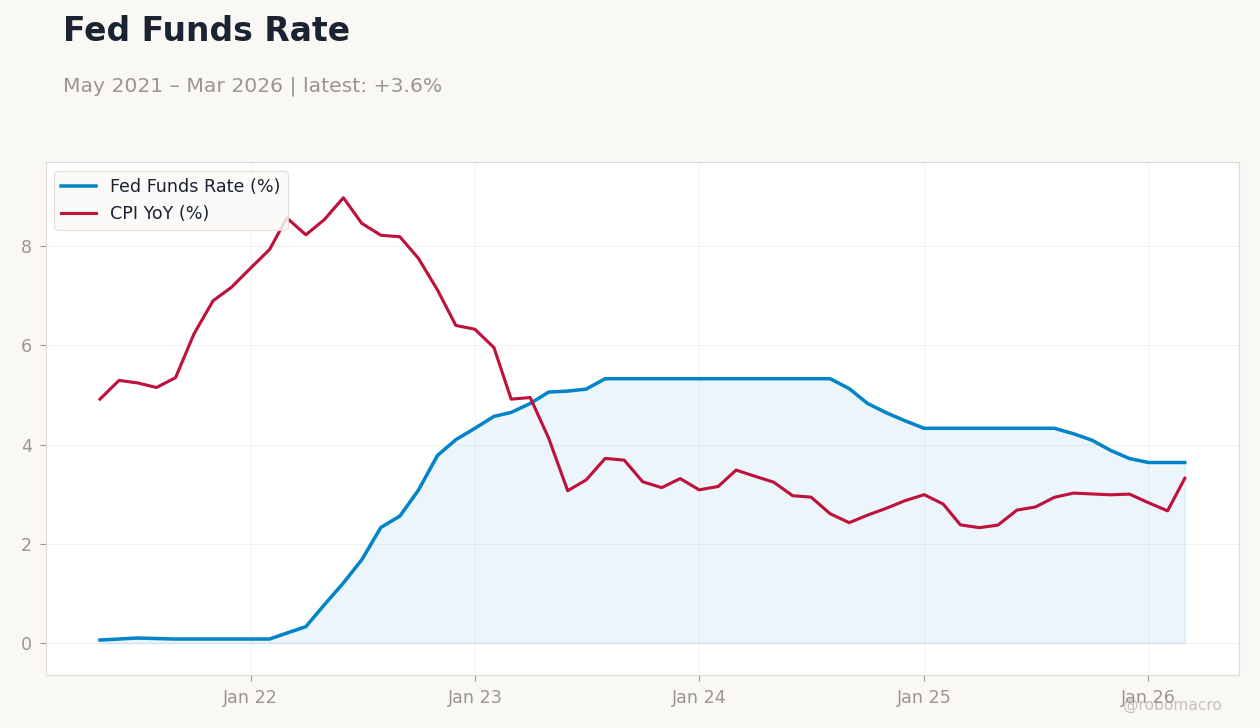

US CPI Inflation | Type: macro_line | CPI Index: 3.32 (2026-03-01) | Range: 2.325–8.979 | Trend(6pt): 4.918,8.463,3.687,2.719,2.665,3.32

US CPI Inflation | Type: macro_line | CPI Index: 3.32 (2026-03-01) | Range: 2.325–8.979 | Trend(6pt): 4.918,8.463,3.687,2.719,2.665,3.32

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Chicago Fed National Activity Index | -0.11 | - | 04:30 |

| Weekly Jobless Claims | 207,000 | 212,000 | 04:30 |

| S&P Global Composite PMI Flash | 50.30 | - | 05:45 |

| S&P Global Manufacturing PMI Flash | 52.30 | 52.50 | 05:45 |

| S&P Global Services PMI Flash | 49.80 | 50 | 05:45 |

- US retail sales exceeded expectations, signaling robust consumer spending amid cooling inflation.

- Equity markets rallied, with Nasdaq leading gains on tech optimism.

- Fed nominee Warsh's hearing highlighted potential balance sheet reduction focus.

Yesterday's Recap

US retail sales rose 1.7% month-over-month, surpassing the 1.4% consensus and prior 0.7%, driven by strong consumer demand despite high interest rates. Retail sales excluding autos climbed 1.9% versus the expected 1.4%, while the control group advanced 0.7% against a 0.2% forecast, underscoring resilient household spending. ADP weekly employment change jumped to 54,750 from 40,250 prior, indicating labor market strength.

Pending home sales increased 1.5% month-over-month, beating the 0.1% consensus but with year-over-year at -1.1%, reflecting housing sector challenges from elevated mortgage rates, which dipped to 6.35% per MBA data. Business inventories grew 0.4% versus 0.3% expected, supporting inventory rebuilding. Equity indices advanced, with S&P 500 up 1.05% to 7,137.90, Nasdaq 100 surging 1.73% to 26,937.28, Dow Jones gaining 0.69% to 49,490.03, and Russell 2000 rising 0.74% to 2,785.38, fueled by positive data beats.

Treasury yields climbed modestly, with 2-year at 3.78% (+1.61%) and 10-year at 4.30% (+0.94%), while WTI crude rose 1.57% to $94.42 amid cease-fire uncertainties, with API showing -4.4 million barrels versus -1 million expected and EIA reporting a crude build of 1.925 million barrels versus -1.2 million expected but gasoline draws of -4.57 million versus -1.5 million.

The Day Ahead

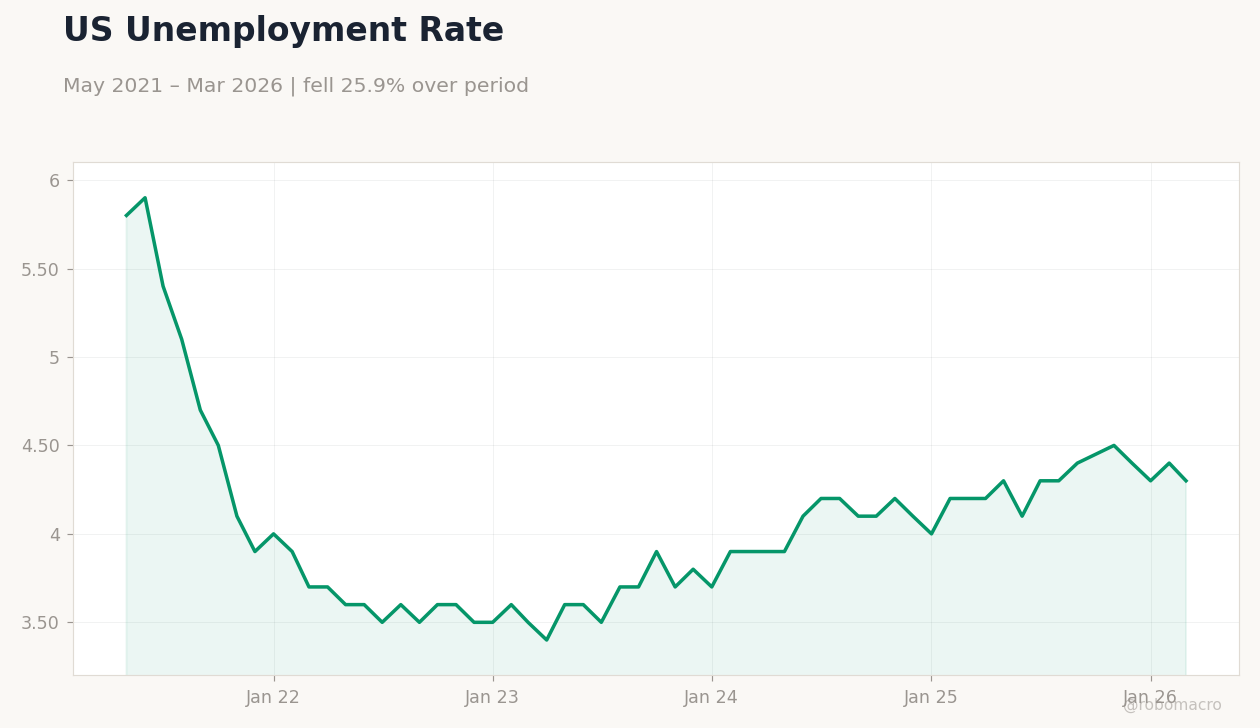

The Chicago Fed National Activity Index releases at 4:30 ET, with prior at -0.11, offering insights into overall economic momentum. Weekly jobless claims follow at 4:30 ET, with prior at 207,000 and consensus at 212,000, crucial for gauging labor market health amid the 4.30% unemployment rate as of March. S&P Global Composite PMI at 5:45 ET will provide flash readings on manufacturing and services activity, potentially influencing Fed rate-cut pricing.

Markets will watch these for signals on growth resilience versus softening, especially with CPI at 2.31% YoY as of April 2025.

Other Economic Notes

Broader US themes point to a soft landing, with consumer spending holding firm despite inventory adjustments and housing headwinds. Labor indicators like ADP's beat suggest unemployment at 4.30% as of March may stabilize, supporting wage growth without inflationary pressures. Energy sector volatility, evident in EIA's crude build, underscores supply dynamics amid geopolitical risks.

(cont...)