US Macro Daily(Beta Mode)

Stocks Climb on Iran Talks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,165.08 | +0.80% |

| Nasdaq 100 | 27,303.67 | +1.95% |

| Dow Jones | 49,230.71 | -0.16% |

| Russell 2000 | 2,787.00 | +0.43% |

| USD/JPY | 159.15 | -0.37% |

| EUR/USD | 1.17 | +0.56% |

| GBP/USD | 1.36 | +0.71% |

| Gold | 4,724.10 | +0.04% |

| WTI Crude | 95.32 | +0.97% |

| Bitcoin | 77,850.34 | -1.03% |

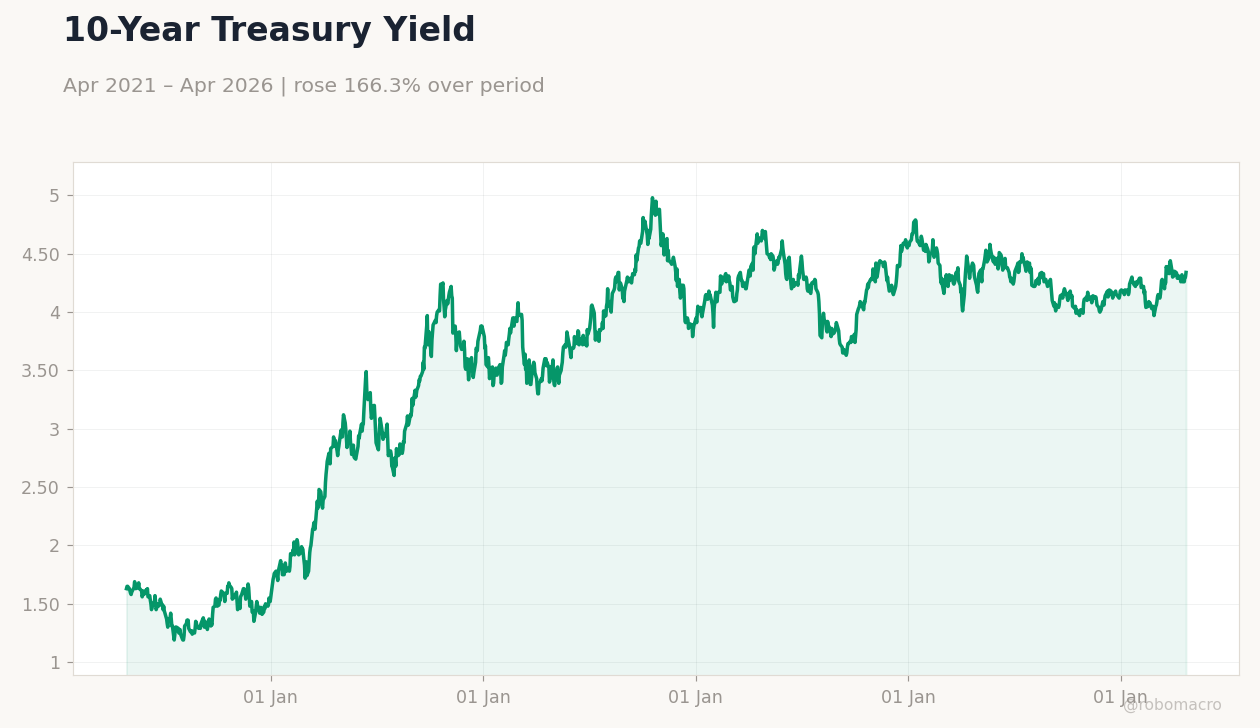

| US 2Y Treasury | 3.83% | +1.06% |

| US 10Y Treasury | 4.34% | +0.93% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

US Industrial Production | Type: macro_line | Industrial Production Index: 0.7417 (2026-03-01) | Range: -1.558–15.67 | Trend(6pt): 15.67,0.9687,-0.2672,-1.558,1.53,0.7417

US Industrial Production | Type: macro_line | Industrial Production Index: 0.7417 (2026-03-01) | Range: -1.558–15.67 | Trend(6pt): 15.67,0.9687,-0.2672,-1.558,1.53,0.7417

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Dallas Fed Manufacturing Index | -0.20 | - | 06:30 |

| Tuesday (2026-04-28) | |||

| ADP Employment Change Weekly | 54,750 | - | 04:15 |

| S&P/Case-Shiller Home Price Year-over-Year | 1.20 | 1 | 05:00 |

| Cb Consumer Confidence | 91.80 | - | 06:00 |

| API Weekly Crude Oil Stocks | -4.4m | - | 12:30 |

| Wednesday (2026-04-29) | |||

| MBA 30-Year Mortgage Rate | 6.35 | - | 03:00 |

| Building Permits Prel | 1.4m | - | 04:30 |

| Building Permits Prel | - | 1.4m | 04:30 |

- US equities advanced amid hopes for US-Iran peace talks, with Nasdaq leading gains on tech strength.

- Treasury yields rose as markets priced in steady Fed policy, reflecting resilient economic data.

- Oil prices edged higher, while the dollar weakened against major peers.

Yesterday's Recap

US markets closed mixed yesterday, with the S&P 500 rising 0.80% to 7,165.08, driven by optimism over potential US-Iran peace talks that boosted investor sentiment. The Nasdaq 100 surged 1.95% to 27,303.67, fueled by gains in technology stocks, while the Dow Jones dipped 0.16% to 49,230.71 amid sector rotation away from industrials. Russell 2000 added 0.43% to 2,787.00, supported by small-cap resilience.

Treasury yields climbed, with the 2-year at 3.83% (change +1.06%) and the 10-year at 4.34% (change +0.93%), as investors digested hawkish economic undertones. Oil prices increased 0.97% to $95.32 per barrel for WTI, reflecting supply dynamics, while gold held steady with a 0.04% gain to $4,724.10. Currency markets saw USD/JPY fall 0.37% to 159.15, EUR/USD rise 0.56% to 1.17, and GBP/USD advance 0.71% to 1.36, amid a softer dollar tone.

No major US data releases occurred yesterday, allowing geopolitical news to dominate trading flows.

The Day Ahead

Today's Dallas Fed Manufacturing Index at 06:30 ET (prior -0.2) could signal regional factory trends. Tuesday brings ADP Employment Change at 04:15 ET (prior 54,750), S&P/Case-Shiller Home Price YoY at 05:00 ET (consensus 1%, prior 1.2%), CB Consumer Confidence at 06:00 ET (prior 91.8), and API Crude Oil Stocks at 12:30 ET (prior -4.4 million barrels). Wednesday features Building Permits Prel at 04:30 ET (consensus 1.39 million, prior 1.386 million), Durable Goods Orders MoM at 04:30 ET (consensus 0.5%, prior -1.4%), Housing Starts at 04:30 ET (consensus 1.4 million, prior 1.487 million), and MBA 30-Year Mortgage Rate at 03:00 ET (prior 6.35%).

These releases could influence Fed expectations and market volatility.

Other Economic Notes

US CPI YoY stands at 2.31%, indicating moderated inflation that supports stable policy, while unemployment at 4.30% reflects labor market resilience. Upcoming housing data on permits and starts may highlight sector challenges from high rates. Tariff risks and geopolitical tensions could amplify volatility in trade-sensitive areas.