Yesterday's Recap

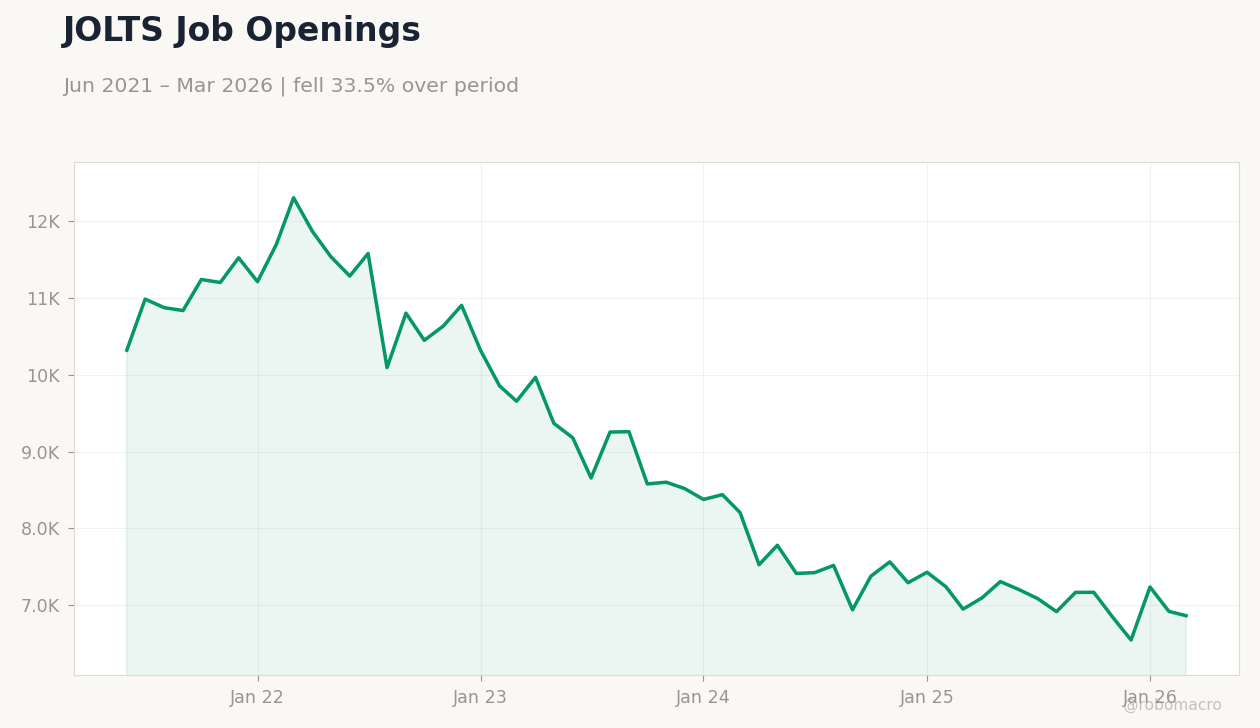

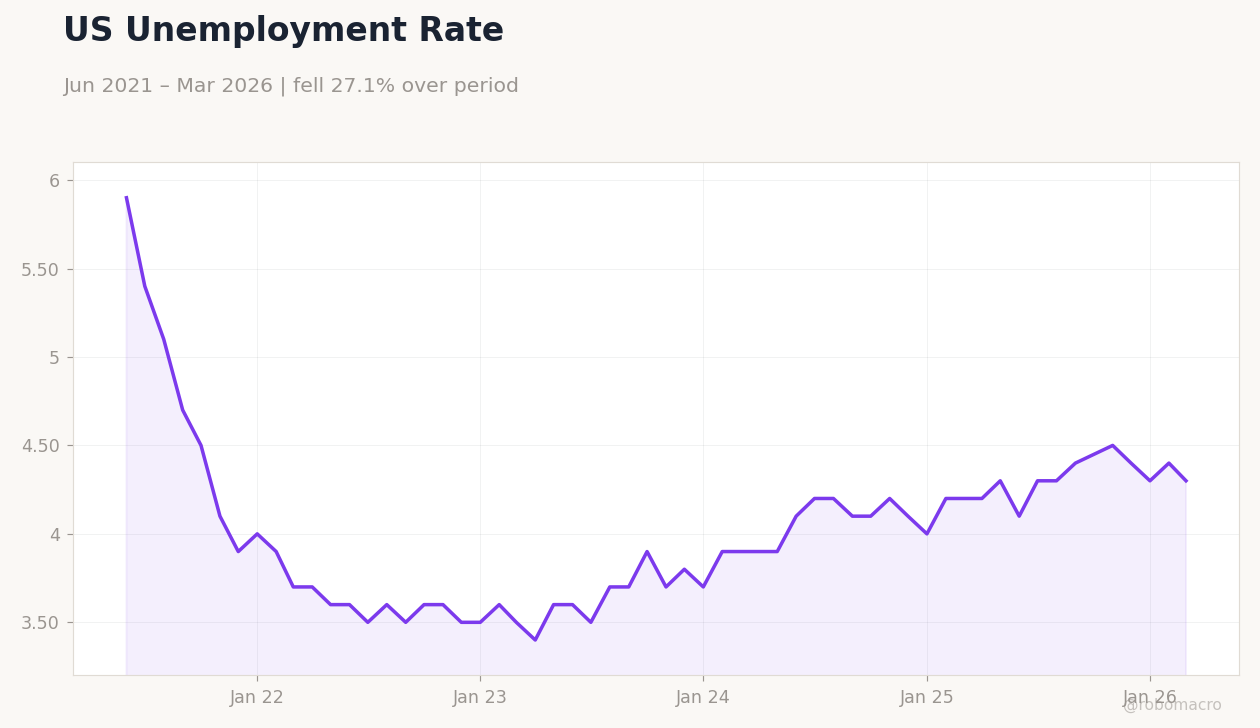

US factory orders rose 1.5% month-over-month on May 4, beating the 0.5% consensus and prior 0.3% gain, underscoring manufacturing vigor. The trade balance widened to -60.3 billion on May 5, worse than the prior -57.8 billion but better than the -60.9 billion forecast, with exports up to 320.9 billion and imports to 381.2 billion. JOLTs job openings fell to 6.866 million, beating the 6.84 million consensus but down from 6.922 million prior, reflecting labor market tightness alongside 4.30% unemployment.

Services PMI eased to 53.6, missing the 53.7 consensus and down from 54.0 previous, yet still in expansion. New home sales climbed to 682,000 units, exceeding the 650,000 consensus with 7.4% month-over-month growth, up from the prior 635,000 and reversing earlier weakness. Fed's Williams spoke on May 4, while Bowman and Barr addressed audiences on May 5, all maintaining a neutral tone.

Equities closed lower: S&P 500 -0.41% at 7,200.75, Nasdaq 100 -0.21% at 27,651.82, Dow Jones -1.13% at 48,941.90, and Russell 2000 -0.60% at 2,796.00, pressured by rising oil prices and Fed anticipation. USD/JPY rose 0.66% to 157.89, while EUR/USD fell 0.19% to 1.17 and GBP/USD -0.22% to 1.36. Gold gained 1.09% to 4,568.60, WTI crude dropped 4.01% to 102.15, and Bitcoin rose 2.18% to 81,571.83.

US 10-year Treasury yield fell 0.23% to 4.39%, with 2-year unchanged at 3.88%.

The Day Ahead

Focus shifts to API weekly crude oil stocks at 12:30 ET on May 5, with consensus for a -2.8 million barrel draw after the prior -1.79 million, amid WTI's recent decline and Middle East risks. On May 6, MBA 30-year mortgage rate releases at 3:00 ET, following 6.37% previous, offering housing insights in a high-rate context. ADP employment change follows at 4:15 ET, with last at 62,000, potentially previewing payrolls.

No Fed speeches today, leaving room for data digestion. Markets may react to oil inventory surprises, influencing inflation views and USD pairs, while eyeing Treasury dynamics for volatility cues.

US Industrial Production Index | Type: macro_line | Index 2017=100: 0.7417 (2026-03-01) | Range: -1.558–8.958 | Trend(6pt): 8.958,1.052,-0.7743,-0.2741,1.231,0.7417

US Industrial Production Index | Type: macro_line | Index 2017=100: 0.7417 (2026-03-01) | Range: -1.558–8.958 | Trend(6pt): 8.958,1.052,-0.7743,-0.2741,1.231,0.7417