US Macro Daily(Beta Mode)

Data Surprises Weigh on Stocks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,337.11 | -0.38% |

| Nasdaq 100 | 28,563.95 | -0.12% |

| Dow Jones | 49,596.97 | -0.63% |

| Russell 2000 | 2,839.63 | -1.63% |

| USD/JPY | 156.66 | +0.10% |

| EUR/USD | 1.18 | +0.27% |

| GBP/USD | 1.36 | +0.25% |

| Gold | 4,717.10 | +0.37% |

| WTI Crude | 95.71 | +0.95% |

| Bitcoin | 79,954.64 | -0.07% |

| US 2Y Treasury | 3.87% | -1.53% |

| US 10Y Treasury | 4.36% | -1.58% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Factory Orders Month-over-Month | 0.30 | 0.50 | 1.50 |

| Speech by Fed's Williams | - | - | - |

| Exports Level | 314,700m | - | 320,900m |

| Imports Level | 372,400m | - | 381,200m |

| Trade Balance | -57,800m | -60,900m | -60,300m |

| JOLTs Job Openings | 6.9m | 6.8m | 6.9m |

| Services Sector PMI | 54 | 53.70 | 53.60 |

| New Home Sales | 583,000 | - | 635,000 |

| New Home Sales | 635,000 | 650,000 | 682,000 |

| New Home Sales Month-over-Month | 8.90 | - | 7.40 |

US Industrial Production Index | Type: macro_line | Index 2017=100: 0.7417 (2026-03-01) | Range: -1.558–8.958 | Trend(6pt): 8.958,1.052,-0.7743,-0.2741,1.231,0.7417

US Industrial Production Index | Type: macro_line | Index 2017=100: 0.7417 (2026-03-01) | Range: -1.558–8.958 | Trend(6pt): 8.958,1.052,-0.7743,-0.2741,1.231,0.7417

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Fed Daly Speech | - | - | 15:30 |

| Fed Goolsbee Speech | - | - | 15:30 |

| Speech by Fed's Bowman | - | - | 15:30 |

| Speech by Fed's Waller | - | - | 15:30 |

- Factory orders jumped 1.5% MoM, beating estimates; JOLTs openings at 6.866M topped consensus but eased from prior.

- Services PMI slipped to 53.6, trade deficit narrowed to -$60.3B; new home sales rose 8.9% MoM to 682K.

- Equities fell with S&P 500 -0.38%, 10Y yield down 1.58% to 4.36%; API oil stocks drew 8.1M barrels.

Yesterday's Recap

Yesterday's US data highlighted economic strength mixed with softening signals. Factory orders rose 1.5% MoM in April, surpassing the 0.5% consensus and prior 0.3% gain, underscoring manufacturing vigor. JOLTs job openings for March reached 6.866 million, above the 6.84 million expected but below February's 6.922 million, pointing to persistent labor tightness.

Services PMI fell to 53.6 in April from 54.0, slightly missing the 53.7 forecast, indicating ongoing expansion at a slower pace. Trade data showed exports at $320.9 billion and imports at $381.2 billion, yielding a -$60.3 billion deficit, better than the -$60.9 billion consensus. New home sales annualized at 682,000 in March, up 8.9% MoM and beating expectations, offsetting earlier weakness.

API reported an 8.1 million barrel crude stock draw, exceeding the 2.8 million forecast, lifting WTI to $95.71 (+0.95%). Markets closed lower: S&P 500 -0.38% at 7,337.11, Nasdaq 100 -0.12% at 28,563.95, Dow -0.63% at 49,596.97, Russell 2000 -1.63% at 2,839.63. Treasuries gained, with 2Y yield at 3.87% (-1.53%) and 10Y at 4.36% (-1.58%).

Currencies shifted: USD/JPY +0.10% to 156.66, EUR/USD +0.27% to 1.18, GBP/USD +0.25% to 1.36. Gold +0.37% to 4,717.10, Bitcoin -0.07% to 79,954.64.

The Day Ahead

The calendar spotlights Fed's Daly speech at 15:30 ET, rated high impact, potentially addressing policy amid recent data. Markets await insights on rate paths, especially with inflation cooling. No other major US releases are confirmed, but attention turns to broader sentiment ahead of tomorrow's payrolls.

Global factors, including yen defense efforts, may influence currency moves.

Other Economic Notes

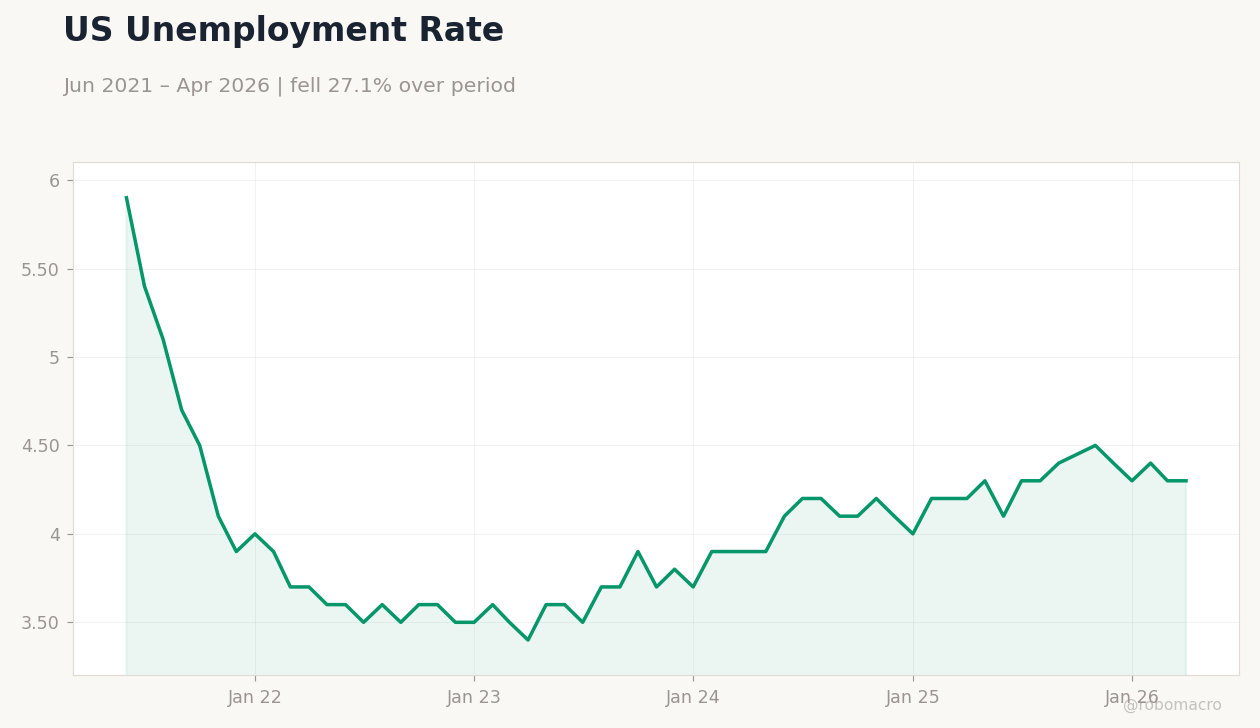

US economy demonstrates resilience, with unemployment at 4.30% as of April supporting spending despite headwinds. CPI YoY at 2.31% through April signals easing inflation toward the Fed's target, reducing rate hike fears. Housing shows momentum via new home sales gains, though MBA 30-year mortgage rates rose to 6.45%, challenging affordability.

<i>↓ p.2</i>