US Macro Daily(Beta Mode)

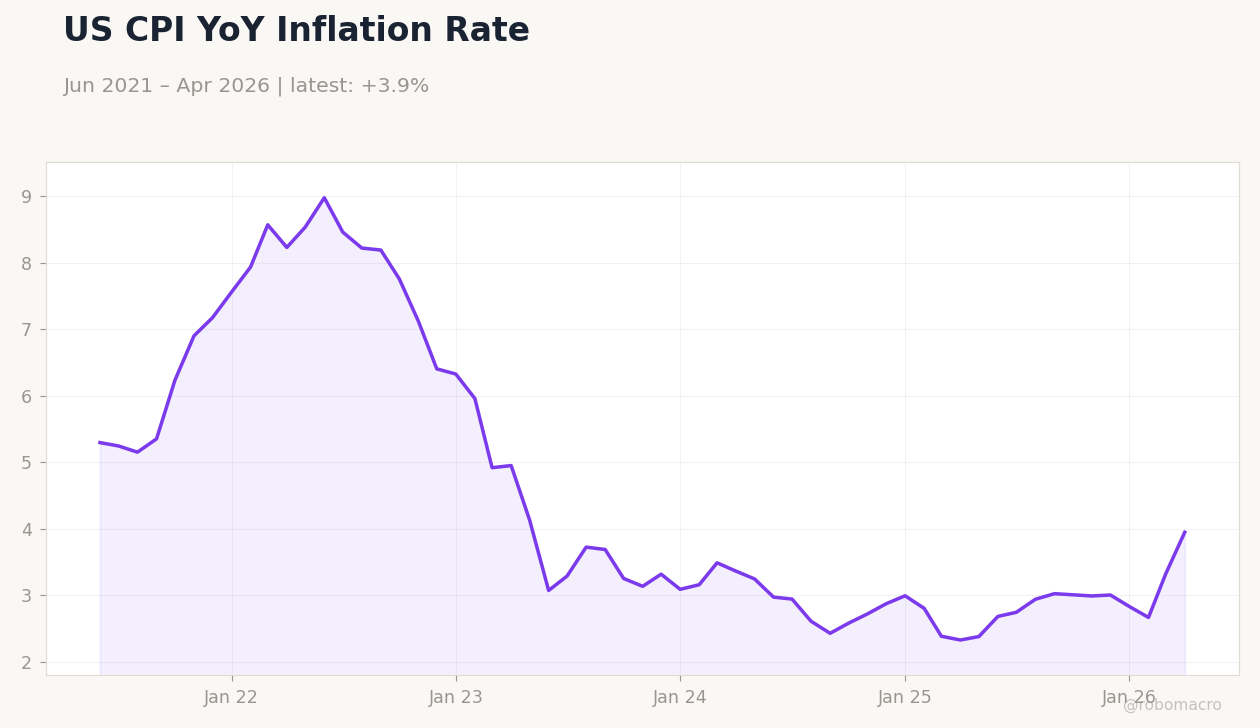

Inflation Surprises Higher

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,400.96 | -0.16% |

| Nasdaq 100 | 29,064.80 | -0.87% |

| Dow Jones | 49,760.56 | +0.11% |

| Russell 2000 | 2,842.83 | -0.97% |

| USD/JPY | 157.81 | +0.37% |

| EUR/USD | 1.17 | -0.54% |

| GBP/USD | 1.35 | -0.72% |

| Gold | 4,703.80 | +0.56% |

| WTI Crude | 102.11 | -0.07% |

| Bitcoin | 80,790.76 | +0.39% |

| US 2Y Treasury | 3.95% | +1.28% |

| US 10Y Treasury | 4.42% | +0.91% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Williams | - | - | - |

| ADP Employment Change Weekly | 30,250 | - | 33,000 |

| Core Inflation Rate Month-over-Month | 0.20 | 0.30 | 0.40 |

| Core Inflation Rate Year-over-Year | 2.60 | 2.70 | 2.80 |

| Inflation Rate Month-over-Month | 0.90 | 0.60 | 0.60 |

| Inflation Rate Year-over-Year | 3.30 | 3.70 | 3.80 |

| Consumer Price Index | 330.21 | - | 333.02 |

| Consumer Price Index SA | 330.29 | - | 332.41 |

| Fed Goolsbee Speech | - | - | - |

| Monthly Budget Statement | -164,000m | 220,000m | 215,000m |

US 10Y Treasury Yield | Type: macro_line | 10Y Yield: 4.42 (2026-05-11) | Range: 1.19–4.98 | Trend(6pt): 1.63,2.87,4.49,4.49,4.41,4.42 | 2Y Yield: 3.95 (2026-05-11) | Range: 0.13–5.19 | Trend(6pt): 0.16,3.23,4.93,4.29,3.92,3.95

US 10Y Treasury Yield | Type: macro_line | 10Y Yield: 4.42 (2026-05-11) | Range: 1.19–4.98 | Trend(6pt): 1.63,2.87,4.49,4.49,4.41,4.42 | 2Y Yield: 3.95 (2026-05-11) | Range: 0.13–5.19 | Trend(6pt): 0.16,3.23,4.93,4.29,3.92,3.95

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| MBA 30-Year Mortgage Rate | 6.45 | - | 07:00 |

| Producer Price Index Month-over-Month | 0.50 | 0.50 | 08:30 |

| Core Producer Price Index Month-over-Month | 0.10 | 0.30 | 08:30 |

| EIA Weekly Crude Oil Inventory | -2.3m | -2m | 10:30 |

| EIA Weekly Gasoline Inventory | -2.5m | -2.5m | 10:30 |

| Speech by Fed's Collins | - | - | 11:30 |

| Speech by Fed's Kashkari | - | - | 13:15 |

| Speech by Fed's Logan | - | - | 19:00 |

- US CPI data beat forecasts, with YoY headline at 3.8% vs. 3.7% expected, core at 2.8% vs. 2.7%.

- Equities mixed: S&P 500 -0.16%, Nasdaq 100 -0.87%, Dow +0.11%; yields rose, dollar strengthened.

- Fed speeches stressed inflation vigilance; oil inventories drew more than anticipated.

Yesterday's Recap

Yesterday's US inflation data exceeded expectations, with headline CPI MoM at 0.6% matching consensus but YoY at 3.8% vs. 3.7% forecast. Core CPI MoM hit 0.4% vs.

0.3% expected, and YoY 2.8% vs. 2.7%. ADP weekly employment rose 33,000, up from prior 30,250, indicating solid job gains.

The monthly budget statement showed a $215 billion surplus, below $220 billion consensus but better than the previous -$164 billion deficit. API crude stocks fell 2.188 million barrels, exceeding the 1.65 million draw expected, aiding oil price stability. Markets responded cautiously: S&P 500 dipped 0.16% to 7,400.96, Nasdaq 100 fell 0.87% to 29,064.80, Dow rose 0.11% to 49,760.56.

Russell 2000 dropped 0.97% to 2,842.83. Treasury yields increased, with 2-year at 3.95% (+1.28%) and 10-year at 4.42% (+0.91%). USD/JPY gained 0.37% to 157.81, EUR/USD fell 0.54% to 1.17, GBP/USD declined 0.72% to 1.35.

Gold rose 0.56% to 4,703.80, WTI slipped 0.07% to 102.11, Bitcoin edged up 0.39% to 80,790.76. Fed's Williams and Goolsbee spoke on price stability.

The Day Ahead

Focus today on Producer Price Index MoM at 08:30 ET, consensus 0.5% after prior 0.5%, which could signal persistent inflation if it tops estimates. Core PPI MoM expected at 0.3% vs. previous 0.1%, highlighting producer costs.

MBA 30-year mortgage rate at 07:00 ET follows last week's 6.45%, influencing housing amid high rates. EIA crude inventory at 10:30 ET, consensus -2 million barrels after prior -2.314 million, may confirm API's draw and affect energy prices. No Fed speakers scheduled; data could shift easing expectations from recent CPI upside.

Other Economic Notes

US economy shows resilience with unemployment at 4.30% as of April 2026, bolstering spending despite inflation. Budget surplus missed slightly, fueling debt debates in a high-rate environment. Energy sector stable, with WTI near $102 amid draws, though global demand worries persist.

<i>↓ p.2</i>