US Macro Daily(Beta Mode)

Retail Sales Steady, Stocks Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,501.24 | +0.77% |

| Nasdaq 100 | 29,580.30 | +0.73% |

| Dow Jones | 50,063.46 | +0.75% |

| Russell 2000 | 2,863.09 | +0.67% |

| USD/JPY | 158.38 | +0.33% |

| EUR/USD | 1.17 | -0.54% |

| GBP/USD | 1.34 | -1.06% |

| Gold | 4,563.50 | -2.45% |

| WTI Crude | 99.39 | -1.76% |

| Bitcoin | 80,743.80 | -0.38% |

| US 2Y Treasury | 3.98% | -0.50% |

| US 10Y Treasury | 4.46% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Retail Sales Month-over-Month | 1.60 | 0.50 | 0.50 |

| Export Prices Month-over-Month | 1.50 | 1.10 | 3.30 |

| Import Prices Month-over-Month | 0.90 | 1 | 1.90 |

| Weekly Jobless Claims | 199,000 | 205,000 | 211,000 |

| Retail Sales Control Group Month-over-Month | 0.80 | 0.40 | 0.50 |

| Retail Sales Excluding Autos Month-over-Month | 1.90 | 0.60 | 0.70 |

| Business Inventories Month-over-Month | 0.40 | 0.80 | 0.90 |

| Speech by Fed's Schmid | - | - | - |

| Speech by Fed's Bowman | - | - | - |

| Fed Hammack Speech | - | - | - |

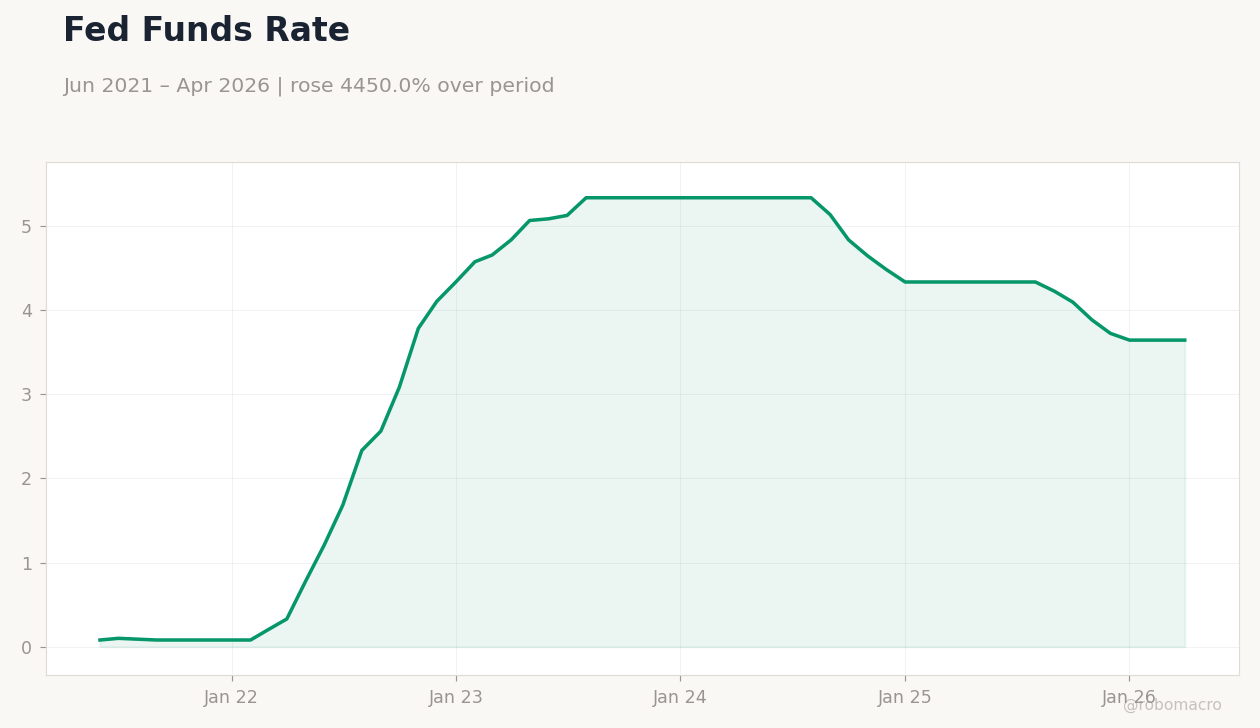

US 10Y Treasury Yield | Type: macro_line | Yield (%): 4.46 (2026-05-13) | Range: 1.19–4.98 | Trend(5pt): 1.64,2.79,4.63,4.52,4.46 | Fed Funds Rate: 3.64 (2026-04-01) | Range: 0.08–5.33 | Trend(5pt): 0.08,2.33,5.33,4.48,3.64

US 10Y Treasury Yield | Type: macro_line | Yield (%): 4.46 (2026-05-13) | Range: 1.19–4.98 | Trend(5pt): 1.64,2.79,4.63,4.52,4.46 | Fed Funds Rate: 3.64 (2026-04-01) | Range: 0.08–5.33 | Trend(5pt): 0.08,2.33,5.33,4.48,3.64

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NY Empire State Manufacturing Index | 11 | 7.50 | 08:30 |

| Industrial Production Month-over-Month | -0.50 | 0.30 | 09:15 |

| Monday (2026-05-18) | |||

| Fed Venable Speech | - | - | 08:30 |

| NAHB Housing Market Index | 34 | - | 10:00 |

| Net Long-term TIC Flows | 58,600m | - | 16:00 |

| Tuesday (2026-05-19) | |||

| ADP Employment Change Weekly | 33,000 | - | 08:15 |

| Pending Home Sales Month-over-Month | 1.50 | - | 10:00 |

| Pending Home Sales Year-over-Year | -1.10 | - | 10:00 |

- Retail sales met forecasts at +0.5% MoM amid resilient spending; ex-autos beat at +0.7%.

- Claims rose to 211k, missing estimates; import/export prices surged.

- Equities gained 0.7%; 2Y yield dropped 50bps to 3.98% as Warsh named Fed chair.

Yesterday's Recap

US retail sales rose 0.5% MoM in April, matching consensus but down sharply from March's 1.6% gain, with ex-autos at +0.7% beating 0.6% estimates and control group at +0.5% topping 0.4%. Weekly jobless claims increased to 211k, above 205k consensus and up from 199k prior. Export prices jumped 3.3% MoM versus 1.1% expected, while import prices hit 1.9% against 1.0% forecasts.

Business inventories expanded 0.9% MoM, edging past 0.8% consensus. Fed speakers included Schmid, Bowman, Hammack (high impact), Williams, and Barr, offering no major policy shifts. Equities rallied with S&P 500 +0.77% to 7,501, Nasdaq 100 +0.73% to 29,580, Dow +0.75% to 50,063, and Russell +0.67%.

Treasuries mixed: 2Y yield fell 50bps to 3.98%, 10Y steady at 4.46%; USD strengthened versus EUR (-0.54% to 1.17) and GBP (-1.06% to 1.34), USD/JPY +0.33% to 158.38; gold -2.45% to 4,564, WTI -1.76% to 99.39.

The Day Ahead

NY Empire State Manufacturing Index arrives at 8:30 ET, forecast at 7.5 versus prior 11.0. Industrial Production MoM follows at 9:15 ET, expected +0.3% after April's -0.5%. No Fed speeches today; Venable speaks Monday at 8:30 ET (high impact).

Markets eye data for manufacturing rebound signals amid Fed transition. Consensus points to modest industrial gains, potentially supporting soft-landing narrative.

Other Economic Notes

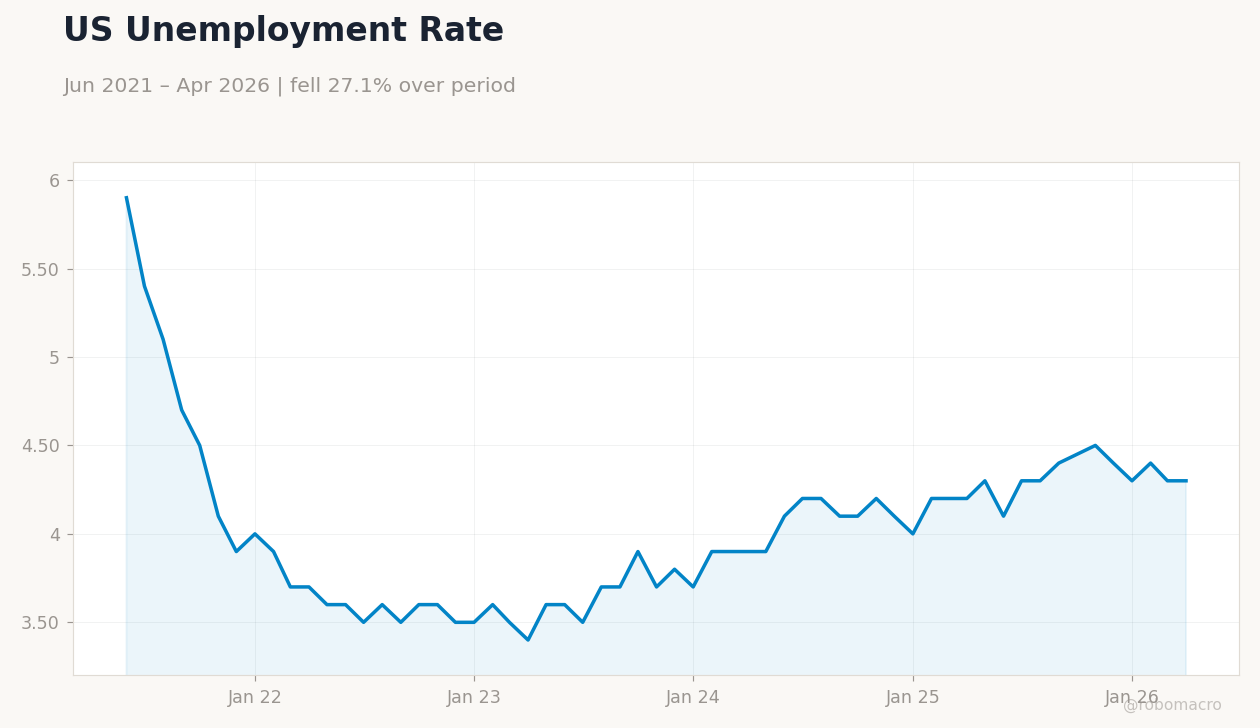

Unemployment holds at 4.30% per latest FRED data, signaling labor market stability. CPI YoY at 2.31% reflects cooling pressures, though supercore rose to 3.3% YoY per recent reports, hinting at sticky services inflation. Fed funds rate steady at 3.63%, with resilient retail underscoring consumer strength despite higher yields.

Global Macro News

Bank of Canada announces rates at 9:45 ET alongside Monetary Policy Report and Business Outlook Survey at 11:30 ET, potentially influencing CAD crosses. Asian stocks climbed on US-China trade talk optimism, with Sensex +789 points to 23,689 amid Trump-Xi summit focus on tariffs and AI. US futures edged higher pre-open, tracking tech rebound despite fading AI hype.

European PMIs beat earlier, bolstering EUR amid mixed Asian session. <i>↓ p.2</i>