US Macro Daily(Beta Mode)

Warsh Confirmed as Fed Chair, Yields Spike

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,408.50 | -1.24% |

| Nasdaq 100 | 29,125.20 | -1.54% |

| Dow Jones | 49,526.17 | -1.07% |

| Russell 2000 | 2,793.30 | -2.44% |

| USD/JPY | 158.92 | +0.34% |

| EUR/USD | 1.16 | -0.27% |

| GBP/USD | 1.33 | -0.32% |

| Gold | 4,545.60 | -0.22% |

| WTI Crude | 102.21 | -3.04% |

| Bitcoin | 76,685.73 | -0.96% |

| US 2Y Treasury | 4.00% | +0.50% |

| US 10Y Treasury | 4.47% | +0.22% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

10-Year Treasury Yield | Type: macro_line | Percent: 4.47 (2026-05-14) | Range: 1.19–4.98 | Trend(6pt): 1.68,2.82,4.63,4.62,4.46,4.47

10-Year Treasury Yield | Type: macro_line | Percent: 4.47 (2026-05-14) | Range: 1.19–4.98 | Trend(6pt): 1.68,2.82,4.63,4.62,4.46,4.47

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NAHB Housing Market Index | 34 | - | 06:00 |

| Net Long-term TIC Flows | 58,600m | - | 12:00 |

| Tuesday (2026-05-19) | |||

| ADP Employment Change Weekly | - | - | 04:15 |

| Pending Home Sales Month-over-Month | 1.50 | - | 06:00 |

| Pending Home Sales Year-over-Year | -1.10 | - | 06:00 |

| API Weekly Crude Oil Stocks | - | - | 12:30 |

| Wednesday (2026-05-20) | |||

| MBA 30-Year Mortgage Rate | - | - | 03:00 |

| EIA Weekly Crude Oil Inventory | - | - | 06:30 |

- Equities fell sharply with S&P 500 down 1.24% as Treasury yields rose to multi-month highs after Kevin Warsh’s Senate confirmation as next Fed chair.

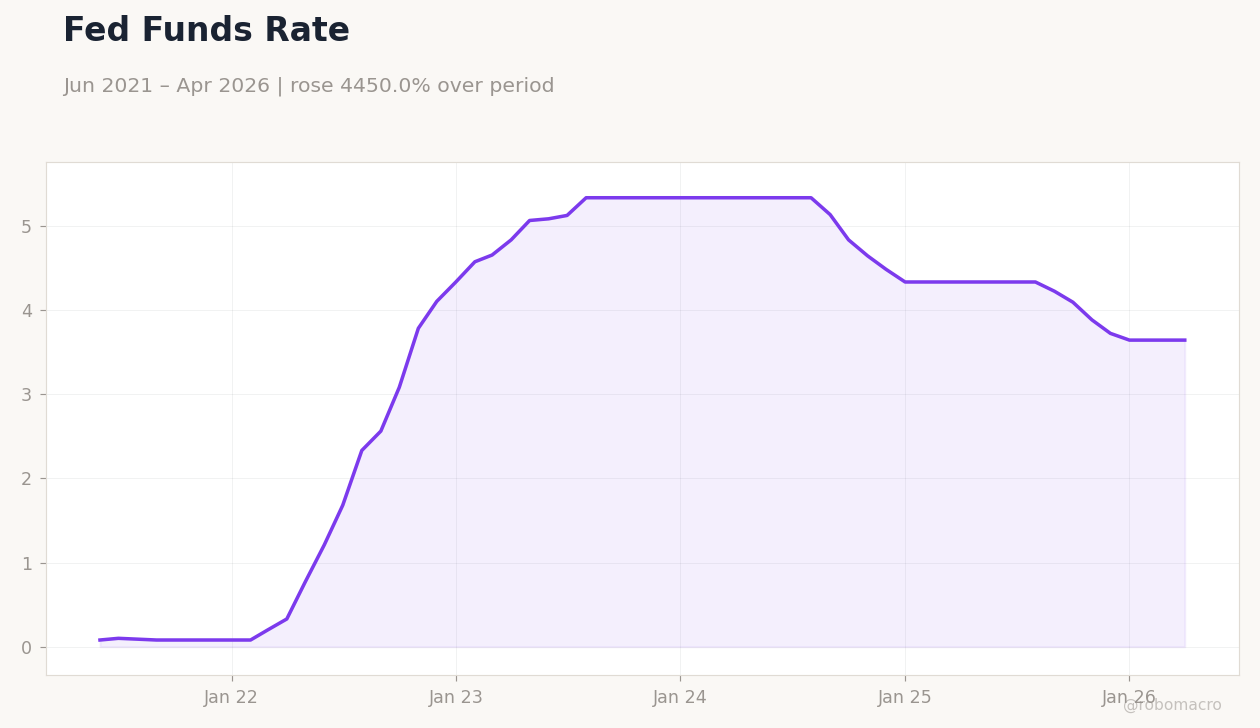

- Housing data and FOMC minutes this week will test whether the new leadership alters the path of policy easing from the current 3.63% Fed funds rate.

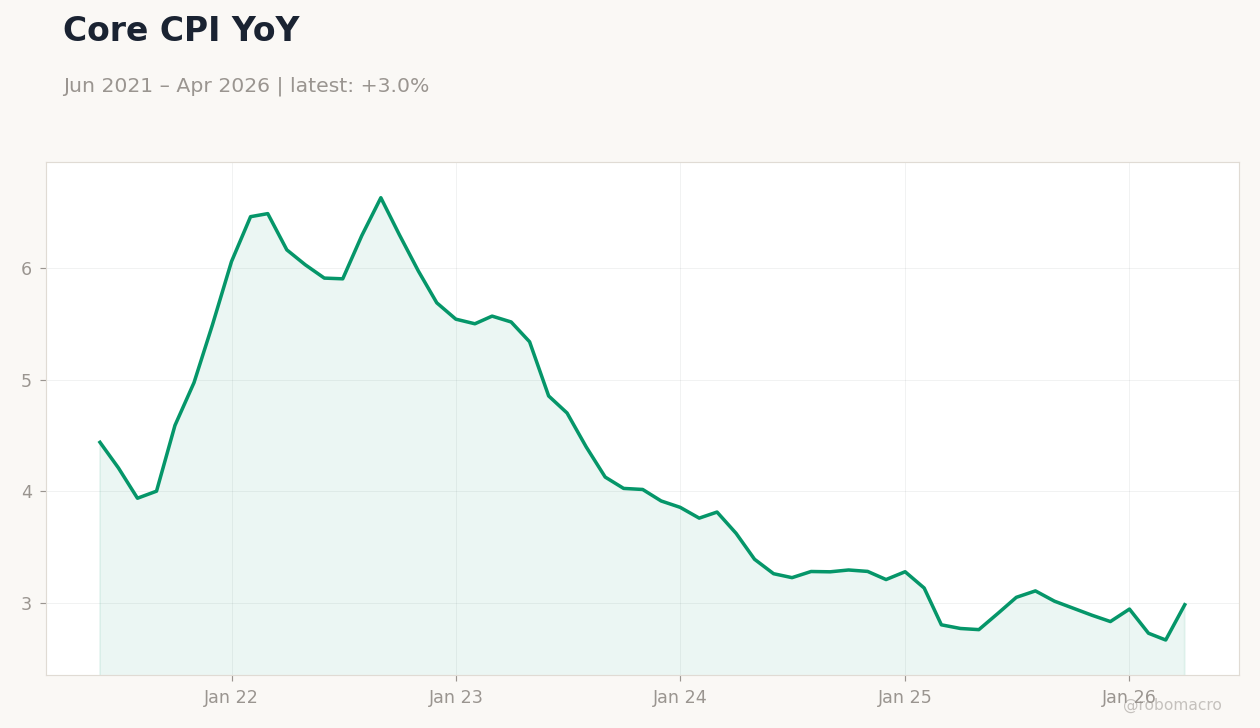

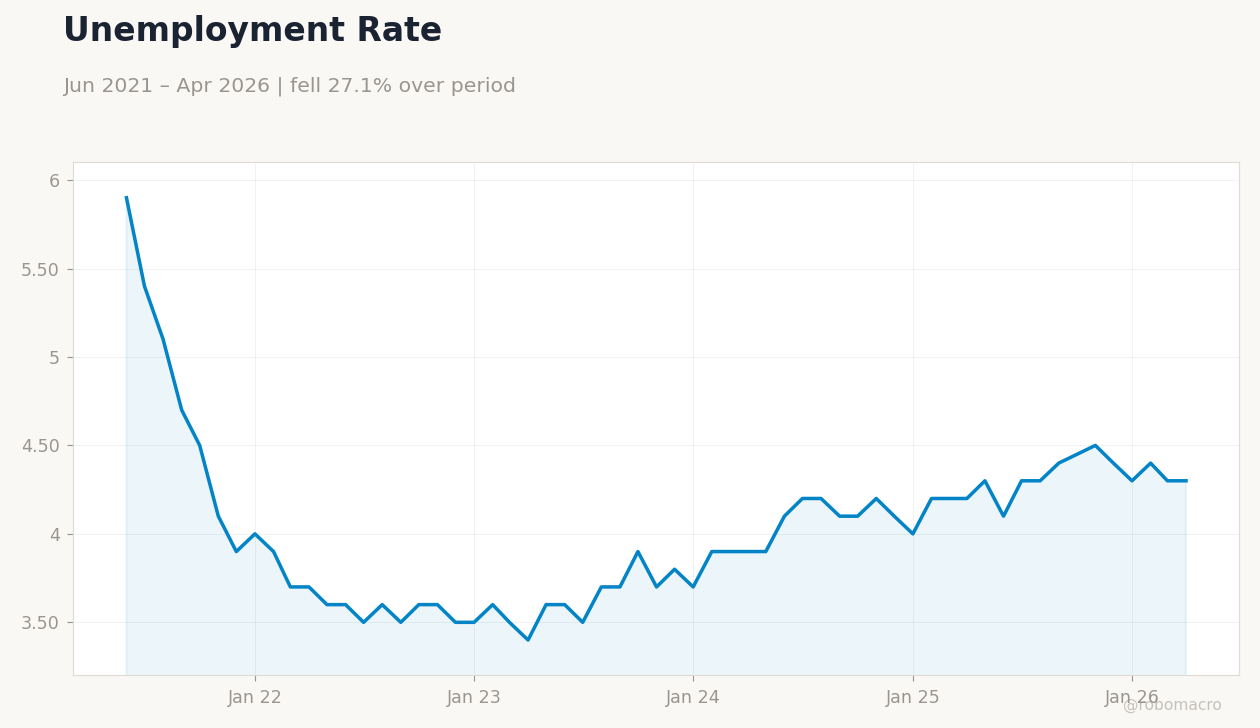

- Core inflation at 2.31% and unemployment at 4.30% keep the Fed’s baseline intact despite the leadership transition.

Yesterday's Recap

US equity indices declined across the board on Monday with the S&P 500 falling 1.24% to 7,408.50, Nasdaq 100 dropping 1.54%, and Russell 2000 sliding 2.44%. Treasury yields climbed, lifting the 2-year note to 4.00% and the 10-year to 4.47%. The dollar strengthened modestly against the yen while EUR/USD eased to 1.16.

Gold slipped 0.22% to $4,545.60 and WTI crude fell 3.04% to $102.21. No major data releases occurred on May 17, leaving the market reaction driven by the Warsh confirmation vote and higher-for-longer rate expectations priced into the curve.

The Day Ahead

The NAHB Housing Market Index at 6:00 a.m. ET will provide the first read on builder sentiment after the recent yield surge. Net long-term TIC flows at noon will show foreign appetite for US assets.

Tomorrow brings ADP employment figures, pending home sales, and API crude inventories. Wednesday’s FOMC minutes at 10:00 a.m. will be the week’s highest-impact release, offering the last detailed view under the prior leadership before housing starts and building permits on Thursday.

Other Economic Notes

The 4.30% unemployment rate continues to signal a resilient labor market that supports the Fed’s patient approach. Elevated 10-year yields near 4.47% are beginning to pressure housing affordability and may weigh on upcoming starts data. Oil prices above $102 reflect both geopolitical supply risks and strong global demand, adding a persistent inflation tailwind that the incoming chair will have to monitor closely.

Global Macro News

The UAE’s exit from OPEC introduces fresh uncertainty into global oil supply dynamics and could keep upward pressure on US energy prices. The UK’s advancing trade talks with Gulf states may indirectly support dollar demand through stronger sterling. China’s softer industrial output adds to concerns about global growth spillovers that could influence Fed easing decisions.

<i>↓ p.2</i>