US Macro Daily(Beta Mode)

Warsh Takes Fed Helm as Yields Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,403.05 | -0.07% |

| Nasdaq 100 | 28,994.37 | -0.45% |

| Dow Jones | 49,686.12 | +0.32% |

| Russell 2000 | 2,775.10 | -0.65% |

| USD/JPY | 159.08 | +0.15% |

| EUR/USD | 1.16 | +0.09% |

| GBP/USD | 1.34 | +0.74% |

| Gold | 4,537.40 | -0.33% |

| WTI Crude | 103.48 | -4.77% |

| Bitcoin | 76,964.54 | +0.01% |

| US 2Y Treasury | 4.09% | +2.25% |

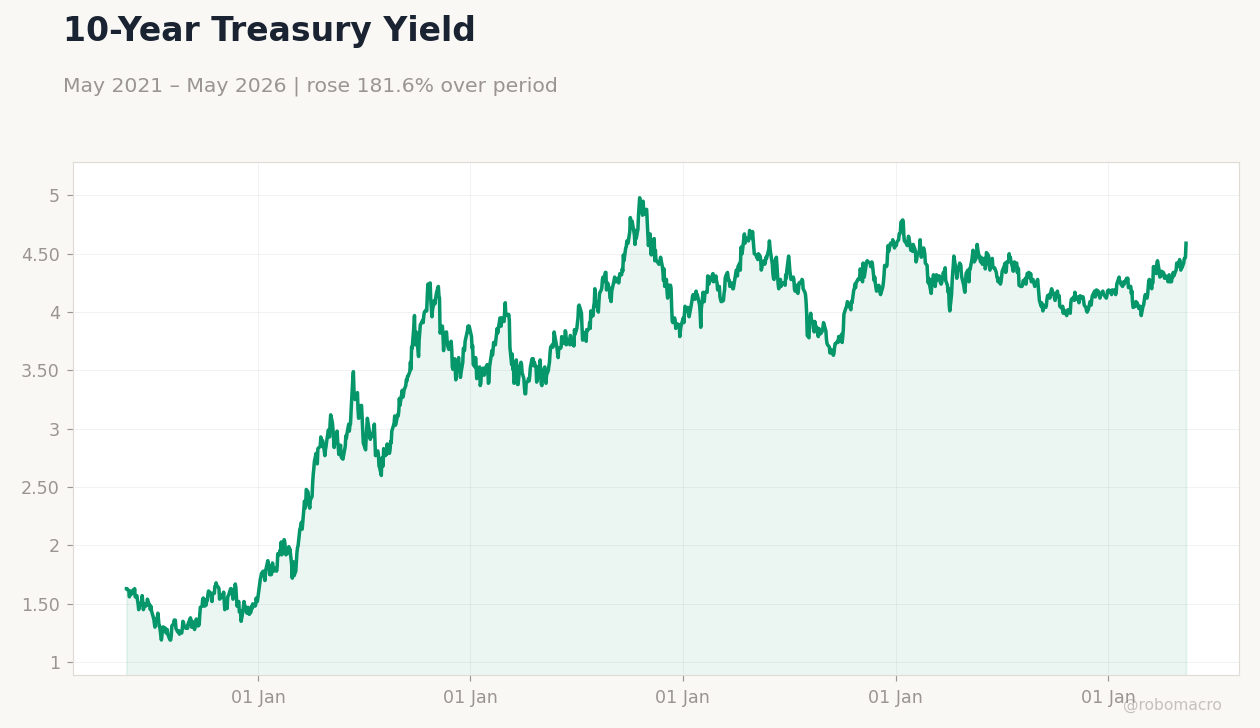

| US 10Y Treasury | 4.59% | +2.68% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Fed Venable Speech | - | - | - |

| NAHB Housing Market Index | 34 | 35 | 37 |

| Net Long-term TIC Flows | 57,000m | - | 81,300m |

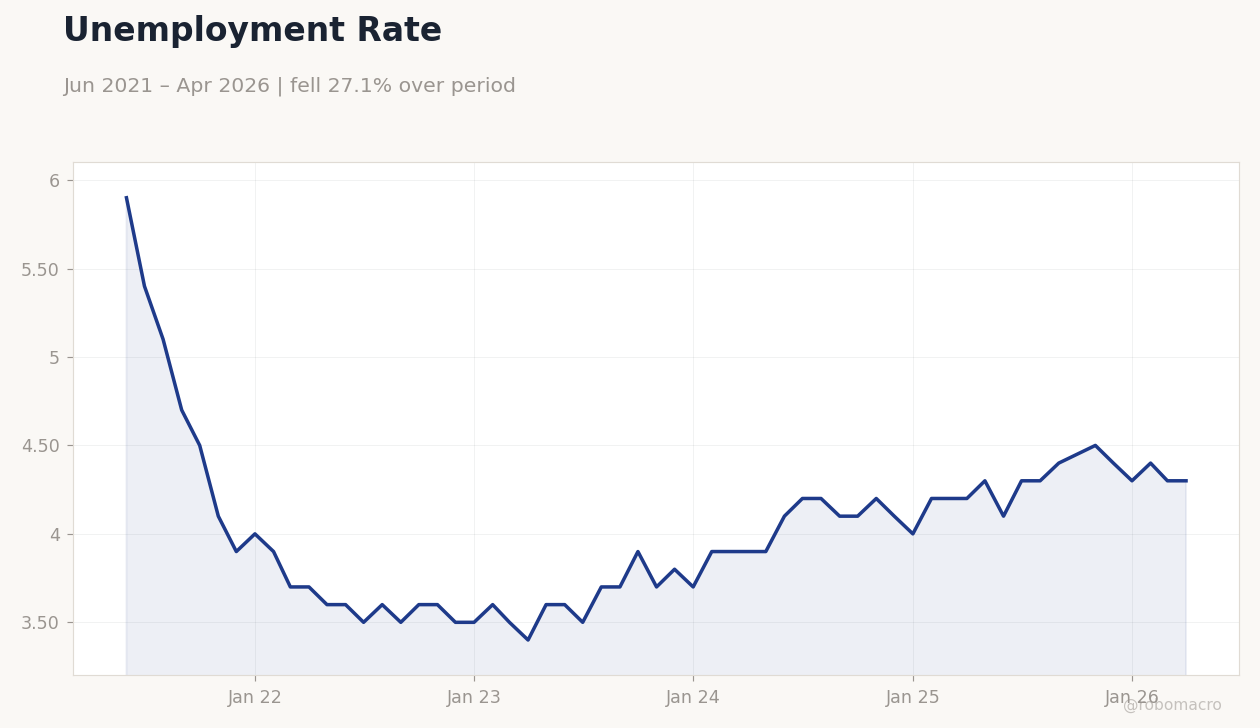

Unemployment Rate | Type: macro_line | Percent: 4.3 (2026-04-01) | Range: 3.4–5.9 | Trend(5pt): 5.9,3.6,3.9,4.1,4.3

Unemployment Rate | Type: macro_line | Percent: 4.3 (2026-04-01) | Range: 3.4–5.9 | Trend(5pt): 5.9,3.6,3.9,4.1,4.3

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change Weekly | 33,000 | - | 04:15 |

| Speech by Fed's Waller | - | - | 05:00 |

| Pending Home Sales Month-over-Month | 1.50 | 1.30 | 06:00 |

| Pending Home Sales Year-over-Year | -1.10 | - | 06:00 |

| API Weekly Crude Oil Stocks | -2.2m | - | 12:30 |

| Speech by Fed's Paulson | - | - | 15:00 |

| Fed Venable Speech | - | - | 15:30 |

- NAHB housing index beat to 37 as TIC flows surged to $81.3bn

- Equities mixed with S&P 500 at 7,403 while 10-year yields rose to 4.59%

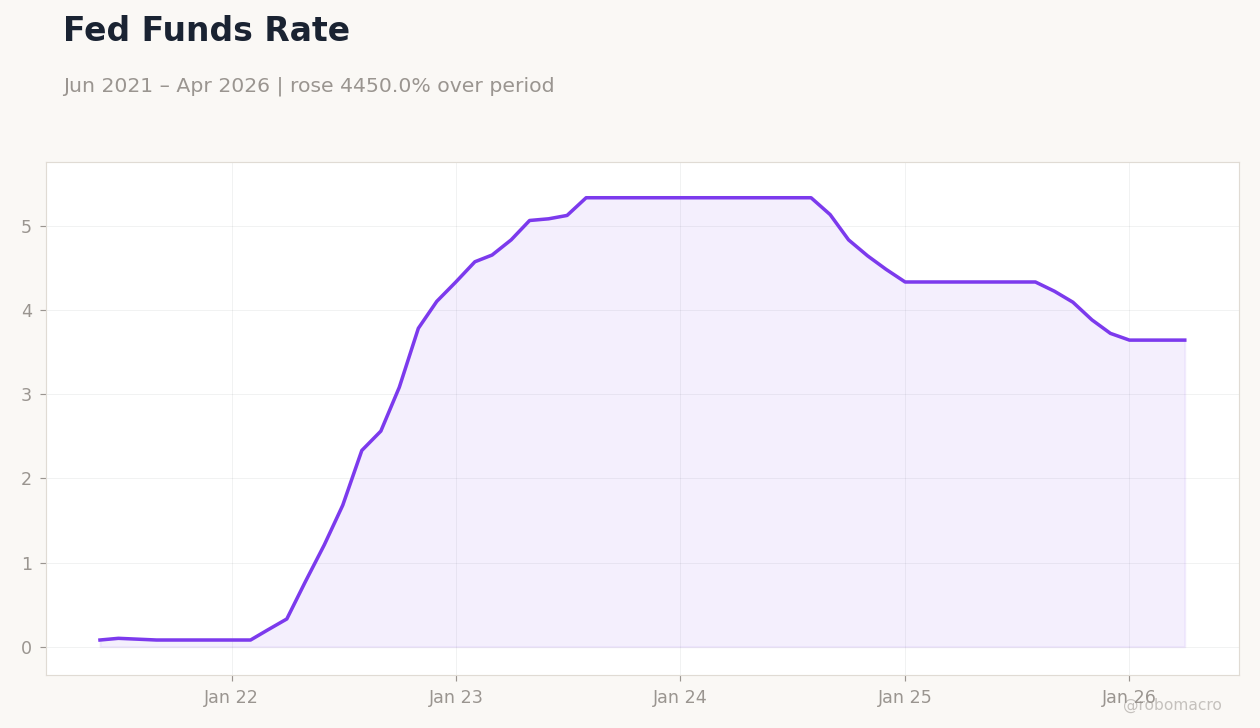

- Kevin Warsh sworn in as Fed chair with focus on inflation at 2.31%

Yesterday's Recap

NAHB Housing Market Index rose to 37, beating consensus of 35 and signaling modest improvement in builder sentiment. Net long-term TIC flows printed a strong $81.3 billion, well above the prior $57 billion reading and pointing to sustained foreign demand for US assets. Equity markets closed mixed as the S&P 500 slipped 0.07% to 7,403.05 while the Dow Jones gained 0.32% to 49,686.12.

The Nasdaq 100 fell 0.45% amid tech pressure. Treasury yields climbed sharply with the 2-year reaching 4.09% and the 10-year hitting 4.59%. WTI crude dropped 4.77% to $103.48 as API inventory data loomed.

USD/JPY edged higher to 159.08 while gold eased 0.33% to $4,537.40.

The Day Ahead

ADP Employment Change is due at 4:15 a.m. ET followed by Pending Home Sales at 6:00 a.m. Speeches from Fed officials Waller at 5:00 a.m., Paulson at 3:00 p.m.

and Venable at 3:30 p.m. will draw attention. API Weekly Crude Oil Stocks release at 12:30 p.m.

could influence energy prices. Markets will parse any fresh signals on policy direction from the new leadership. Housing data are expected to show continued softness consistent with elevated mortgage rates.

Other Economic Notes

US CPI stands at 2.31% year-over-year with unemployment at 4.30%, keeping the policy backdrop data-dependent. Housing metrics remain below pre-pandemic norms despite the NAHB beat, reflecting affordability constraints from higher yields. Strong TIC inflows underscore external appetite for US fixed income amid global uncertainty.

Broader growth signals point to resilience but with limited upside surprises in recent prints.

Global Macro News

UAE exit from OPEC adds supply uncertainty that could support elevated oil prices near $103. Iran acknowledged export difficulties due to US naval actions, tightening global energy balances. Trump cited Gulf state requests in pausing planned Iran action, easing near-term geopolitical risk.

<i>↓ p.2</i>