US Macro Daily(Beta Mode)

Warsh Sworn In as Oil Prices Drop 6%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,353.61 | -0.67% |

| Nasdaq 100 | 28,818.84 | -0.61% |

| Dow Jones | 49,363.88 | -0.65% |

| Russell 2000 | 2,747.07 | -1.01% |

| USD/JPY | 159.00 | +0.09% |

| EUR/USD | 1.16 | -0.44% |

| GBP/USD | 1.34 | -0.26% |

| Gold | 4,494.00 | -0.27% |

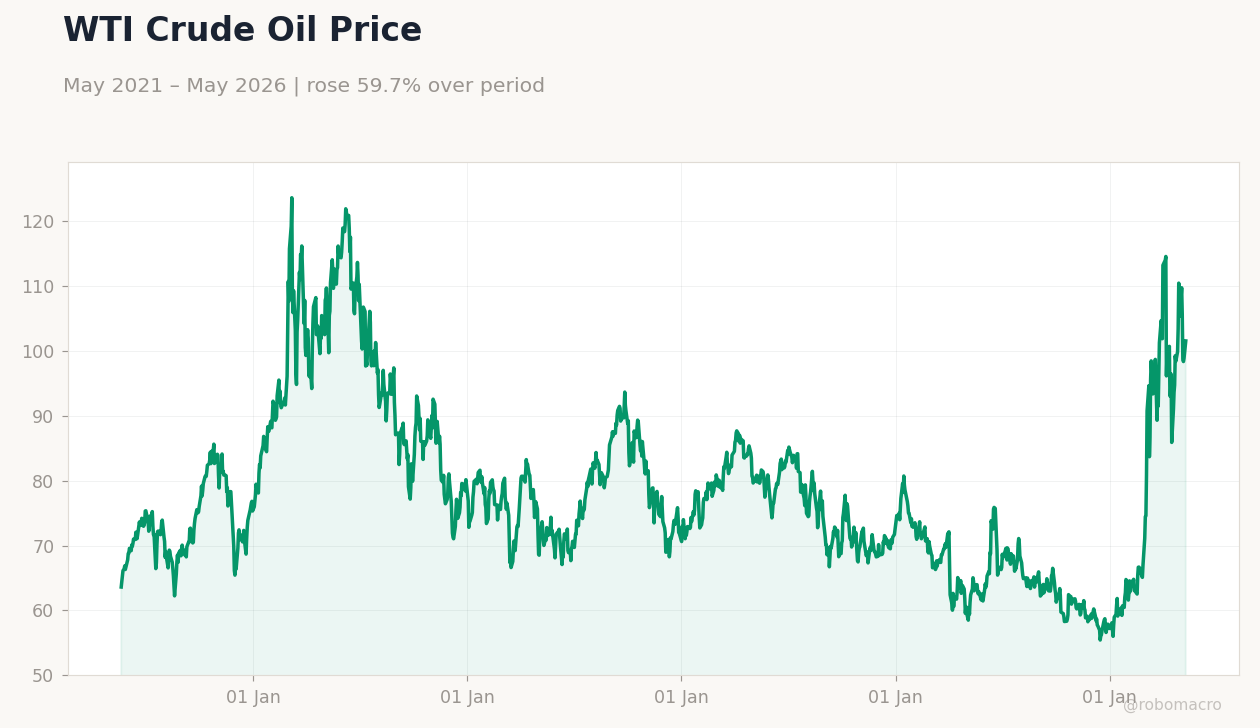

| WTI Crude | 101.22 | -6.08% |

| Bitcoin | 77,432.64 | +0.89% |

| US 2Y Treasury | 4.07% | -0.49% |

| US 10Y Treasury | 4.61% | +0.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Fed Venable Speech | - | - | - |

| NAHB Housing Market Index | 34 | 35 | 37 |

| Net Long-term TIC Flows | 57,000m | - | 81,300m |

| ADP Employment Change Weekly | 33,000 | - | 42,250 |

| Speech by Fed's Waller | - | - | - |

| Pending Home Sales Month-over-Month | 1.70 | 1 | 1.40 |

| Pending Home Sales Year-over-Year | -1.10 | - | 3.20 |

| API Weekly Crude Oil Stocks | -2.2m | -3.4m | -9.1m |

| API Weekly Crude Oil Stocks | -2.2m | -3.4m | -9.1m |

| Speech by Fed's Paulson | - | - | - |

10-Year Treasury Yield | Type: macro_line | Yield (%): 4.61 (2026-05-18) | Range: 1.19–4.98 | Trend(6pt): 1.63,2.88,4.53,4.47,4.47,4.61

10-Year Treasury Yield | Type: macro_line | Yield (%): 4.61 (2026-05-18) | Range: 1.19–4.98 | Trend(6pt): 1.63,2.88,4.53,4.47,4.47,4.61

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Speech by Fed's Paulson | - | - | 04:00 |

| Speech by Fed's Barr | - | - | 06:15 |

| EIA Weekly Crude Oil Inventory | -4.3m | -2.5m | 06:30 |

| EIA Weekly Gasoline Inventory | -4.1m | - | 06:30 |

| FOMC Meeting Minutes | - | - | 10:00 |

- NAHB Housing Index beat to 37, signaling resilient builder sentiment despite elevated rates.

- API crude stocks drew 9.1 million barrels, yet WTI fell 6.08% to $101.22 on demand concerns.

- Equities declined 0.6-1.0% while 10-year Treasury yields rose 4 bp to 4.61%.

Yesterday's Recap

US housing data surprised to the upside as the NAHB index climbed to 37 from 34, exceeding the 35 consensus and pointing to firmer demand for new homes. Pending home sales rose 1.4% month-over-month and 3.2% year-over-year, confirming a modest recovery in contract activity. API reported a larger-than-expected 9.1 million barrel crude draw, tightening near-term supply balances.

Equity indices fell across the board with the S&P 500 down 0.67% to 7,353.61 and the Russell 2000 off 1.01%. Treasury yields diverged as the 2-year eased 2 bp to 4.07% while the 10-year climbed 4 bp to 4.61%. The dollar held steady against the yen at 159.00.

Fed speakers Venable and Waller reiterated data-dependent patience ahead of the policy transition.

The Day Ahead

Markets will focus on the EIA weekly crude inventory release at 6:30 a.m. ET, with analysts expecting a 2.5 million barrel draw. Fed Governor Barr and former Governor Paulson are scheduled to speak on monetary policy options.

MBA 30-year mortgage rates will be monitored for any further rise above 6.46%. Housing and energy data will set the tone before Friday’s transition at the Federal Reserve. No major consumer or labor releases are due.

Other Economic Notes

Elevated energy prices continue to pressure household budgets, with gasoline above $4 per gallon in all 50 states. Thirty-year Treasury borrowing costs have reached levels unseen since 2007, weighing on corporate hiring plans and consumer spending. The incoming administration’s fiscal projections show a modestly narrower 2026 deficit, providing limited relief to Treasury supply concerns.

Labor market data remain consistent with the 4.30% unemployment rate recorded in April.

Global Macro News

The G7 communiqué highlighted risks from Middle East conflict to global growth and energy markets. UK CPI cooled to 2.8% year-over-year, widening the transatlantic rate differential. <i>↓ p.2</i>