US Macro Daily(Beta Mode)

Warsh Sworn In as Fed Chair Amid Soft Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,473.47 | +0.37% |

| Nasdaq 100 | 29,481.64 | +0.42% |

| Dow Jones | 50,579.70 | +0.58% |

| Russell 2000 | 2,869.23 | +0.91% |

| USD/JPY | 158.93 | -0.05% |

| EUR/USD | 1.16 | +0.21% |

| GBP/USD | 1.35 | +0.43% |

| Gold | 4,523.20 | +0.05% |

| WTI Crude | 96.60 | +0.00% |

| Bitcoin | 77,369.38 | +0.50% |

| US 2Y Treasury | 4.08% | +0.99% |

| US 10Y Treasury | 4.57% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Consumer Confidence Index | Type: macro_line | Confidence Index: 49.8 (2026-04-01) | Range: 49.8–85.5 | Trend(6pt): 85.5,58.2,63.8,74,56.6,49.8

Consumer Confidence Index | Type: macro_line | Confidence Index: 49.8 (2026-04-01) | Range: 49.8–85.5 | Trend(6pt): 85.5,58.2,63.8,74,56.6,49.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-05-26) | |||

| Chicago Fed National Activity Index | -0.20 | - | 04:30 |

| S&P/Case-Shiller Home Price Year-over-Year | 0.90 | 1 | 05:00 |

| Cb Consumer Confidence | 92.80 | - | 06:00 |

| Dallas Fed Manufacturing Index | -2.30 | - | 06:30 |

| Wednesday (2026-05-27) | |||

| Speech by Fed's Logan | - | - | 00:00 |

| MBA 30-Year Mortgage Rate | 6.56 | - | 03:00 |

| ADP Employment Change Weekly | 42,250 | - | 04:15 |

| Fed Cook Speech | - | - | 11:55 |

- Equities advanced with S&P 500 rising 0.37% to 7,473.47 as AI demand lifted sentiment.

- Treasury yields held steady with 2-year at 4.08% and 10-year at 4.57% after modest moves.

- Markets await Core PCE and GDP revisions while pricing limited near-term policy shifts.

Yesterday's Recap

US equity indices closed higher on May 24 with the Dow Jones gaining 0.58% to 50,579.70 and Nasdaq 100 up 0.42% to 29,481.64. Small caps outperformed as Russell 2000 rose 0.91%. Treasury yields edged up with the 2-year increasing 0.99% to 4.08% while the 10-year stayed at 4.57%.

USD/JPY eased 0.05% to 158.93 and EUR/USD gained 0.21% to 1.16. Gold held near 4,523.20 with minimal change. No major data releases occurred, leaving price action driven by ongoing AI enthusiasm and positioning ahead of inflation prints.

Bitcoin added 0.50% to 77,369.38.

The Day Ahead

Chicago Fed National Activity Index releases at 4:30 ET on May 26 alongside Case-Shiller home prices and consumer confidence. Dallas Fed manufacturing survey follows at 6:30 ET. On May 27, Fed's Cook speaks at 11:55 ET and Jefferson at 16:00 ET.

Core PCE month-over-month, durable goods orders, and second-estimate GDP growth arrive at 4:30 ET on May 28. These releases will shape views on consumer strength and price pressures. Markets will monitor speeches for signals from the new leadership.

Other Economic Notes

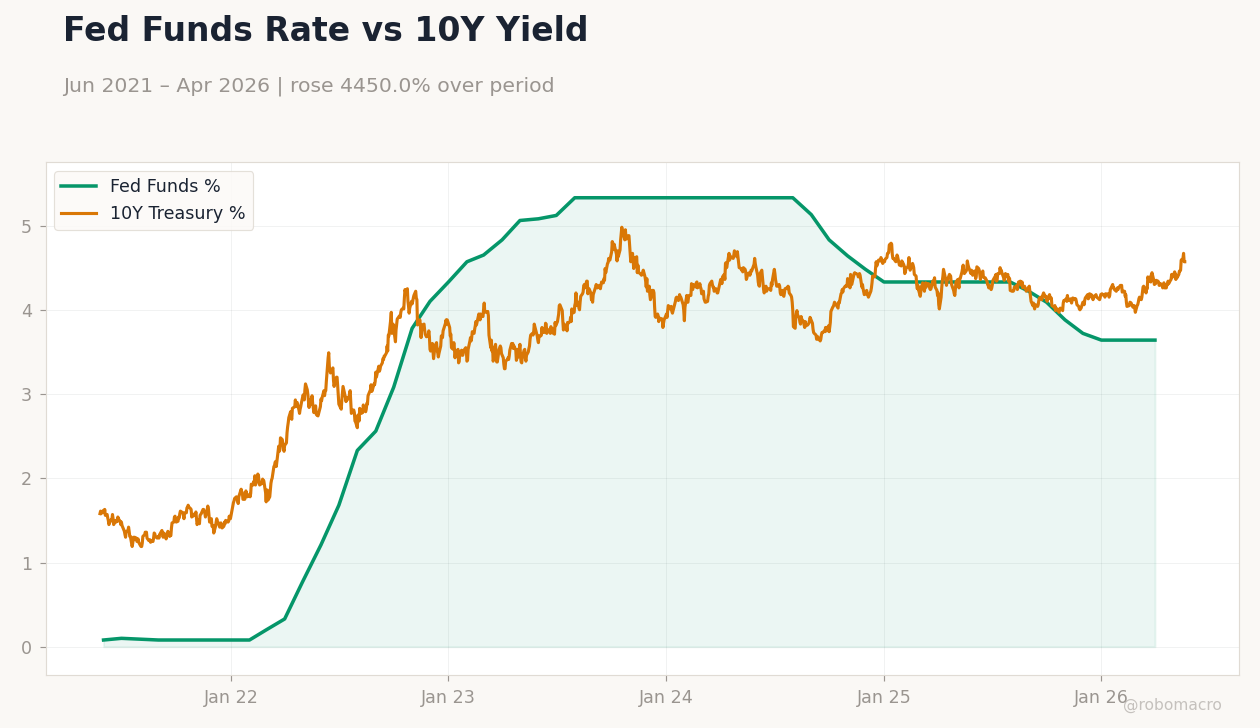

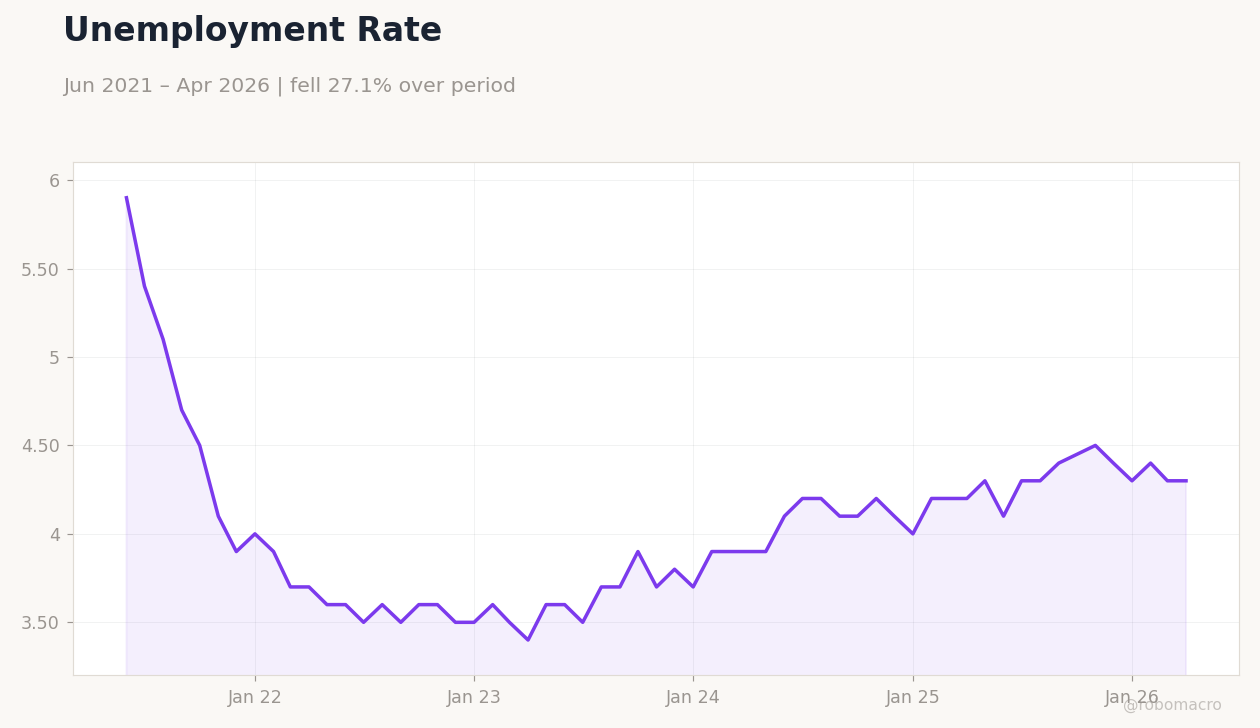

US CPI stood at 2.31% year-over-year and unemployment at 4.30% in recent readings, consistent with gradual cooling. The Fed funds rate remains at 3.62%. Strong corporate earnings growth supports equity valuations despite elevated yields.

Housing data due this week will test whether higher rates continue to constrain activity. Broader sentiment stays anchored to AI-driven productivity gains rather than traditional cyclical indicators.

Global Macro News

Treasury yields reacted little to Middle East developments as traders focused on domestic inflation paths. European and Asian markets rose in tandem with US tech gains. Oil held near 96.60 with limited reaction to supply signals.

Cross-border capital flows favored US assets given relative growth differentials. <i>↓ p.2</i>