US Macro Daily(Beta Mode)

Warsh Leads Fed as Oil Falls on Iran Hopes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,473.47 | +0.37% |

| Nasdaq 100 | 29,481.64 | +0.42% |

| Dow Jones | 50,579.70 | +0.58% |

| Russell 2000 | 2,869.23 | +0.91% |

| USD/JPY | 159.14 | +0.12% |

| EUR/USD | 1.16 | +0.03% |

| GBP/USD | 1.35 | +0.03% |

| Gold | 4,538.50 | +0.39% |

| WTI Crude | 91.92 | -4.84% |

| Bitcoin | 77,337.98 | +0.08% |

| US 2Y Treasury | 4.08% | +0.99% |

| US 10Y Treasury | 4.57% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

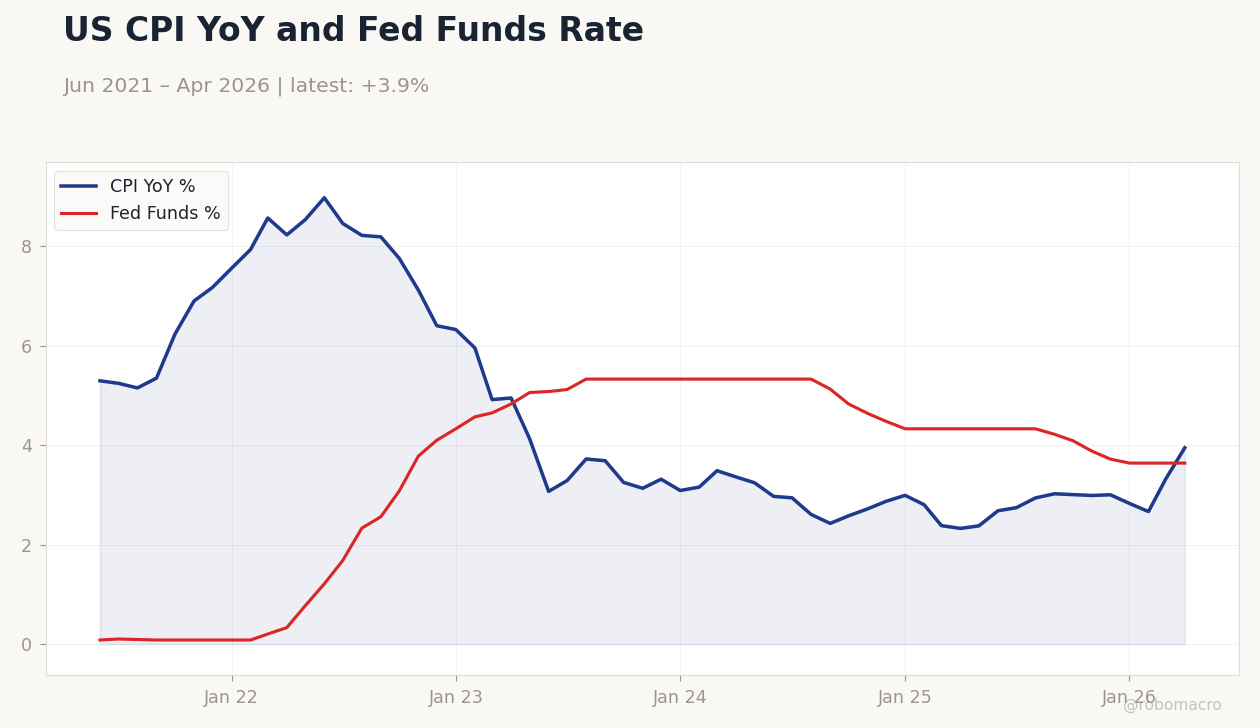

US CPI YoY and Fed Funds Rate | Type: macro_line | CPI YoY %: 3.947 (2026-04-01) | Range: 2.325–8.979 | Trend(6pt): 5.296,8.223,3.251,2.871,3.32,3.947 | Fed Funds %: 3.64 (2026-04-01) | Range: 0.08–5.33 | Trend(5pt): 0.08,2.33,5.33,4.48,3.64

US CPI YoY and Fed Funds Rate | Type: macro_line | CPI YoY %: 3.947 (2026-04-01) | Range: 2.325–8.979 | Trend(6pt): 5.296,8.223,3.251,2.871,3.32,3.947 | Fed Funds %: 3.64 (2026-04-01) | Range: 0.08–5.33 | Trend(5pt): 0.08,2.33,5.33,4.48,3.64

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Chicago Fed National Activity Index | -0.20 | - | 04:30 |

| S&P/Case-Shiller Home Price Year-over-Year | 0.90 | 1 | 05:00 |

| Cb Consumer Confidence | 92.80 | - | 06:00 |

| Dallas Fed Manufacturing Index | -2.30 | - | 06:30 |

| Wednesday (2026-05-27) | |||

| Speech by Fed's Logan | - | - | 00:00 |

| MBA 30-Year Mortgage Rate | 6.56 | - | 03:00 |

| ADP Employment Change Weekly | 42,250 | - | 04:15 |

| Fed Cook Speech | - | - | 11:55 |

| API Weekly Crude Oil Stocks | -9.1m | - | 12:30 |

- Equities advance with S&P 500 at 7,473.47 as oil drops 4.84% on easing Iran tensions

- New Fed Chair Warsh stresses AI-driven cost cuts while funds rate holds at 3.62%

- CPI at 2.31% and unemployment at 4.30% keep policy focus on gradual normalization

Yesterday's Recap

US equity indices posted gains with the Dow Jones rising 0.58% to 50,579.70 and Russell 2000 climbing 0.91%. Oil prices fell sharply after reports of US strikes in Iran and renewed peace talks that raised hopes for reopening the Strait of Hormuz. Treasury yields showed mixed moves as the 2-year note yield increased to 4.08% while the 10-year held steady at 4.57%.

The dollar strengthened modestly against the yen at 159.14. Gold advanced 0.39% to 4,538.50 amid geopolitical uncertainty. No major data releases occurred on May 25, leaving markets to react primarily to headlines on energy and central bank leadership.

Bitcoin edged higher by 0.08% to 77,337.98.

The Day Ahead

The Chicago Fed National Activity Index releases at 4:30 ET followed by S&P/Case-Shiller home prices and Conference Board consumer confidence. Dallas Fed manufacturing data arrives at 6:30 ET. Markets will monitor any follow-through from yesterday’s oil price drop and its impact on inflation expectations.

Fed Governor Cook is scheduled to speak at 11:55 ET tomorrow while ADP employment figures and mortgage rates also print. Traders await the second GDP estimate and core PCE release on Thursday for fresh growth and inflation signals.

Other Economic Notes

Housing price growth remains modest at a 0.9% year-over-year pace with consensus expecting a slight pickup to 1%. Consumer confidence at 92.8 signals ongoing caution among households despite stable labor market conditions. Manufacturing surveys from Dallas and Chicago will provide early reads on regional activity ahead of national data.

Broader themes center on whether AI productivity gains can sustain expansion without reigniting price pressures.

Global Macro News

US strikes in Iran checked optimism for a quick peace deal and kept energy markets volatile despite the sharp price decline. Petrodollar dynamics continue to shift as dollar-oil linkages weaken amid changing trade patterns with China. Nigerian naira held steady against the dollar while Saudi officials joined condemnation of actions in Gaza.

<i>↓ p.2</i>