US Macro Daily(Beta Mode)

Tech Rally Offsets Oil Drop on Mixed Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,519.12 | +0.61% |

| Nasdaq 100 | 30,001.32 | +1.76% |

| Dow Jones | 50,461.68 | -0.23% |

| Russell 2000 | 2,920.54 | +1.79% |

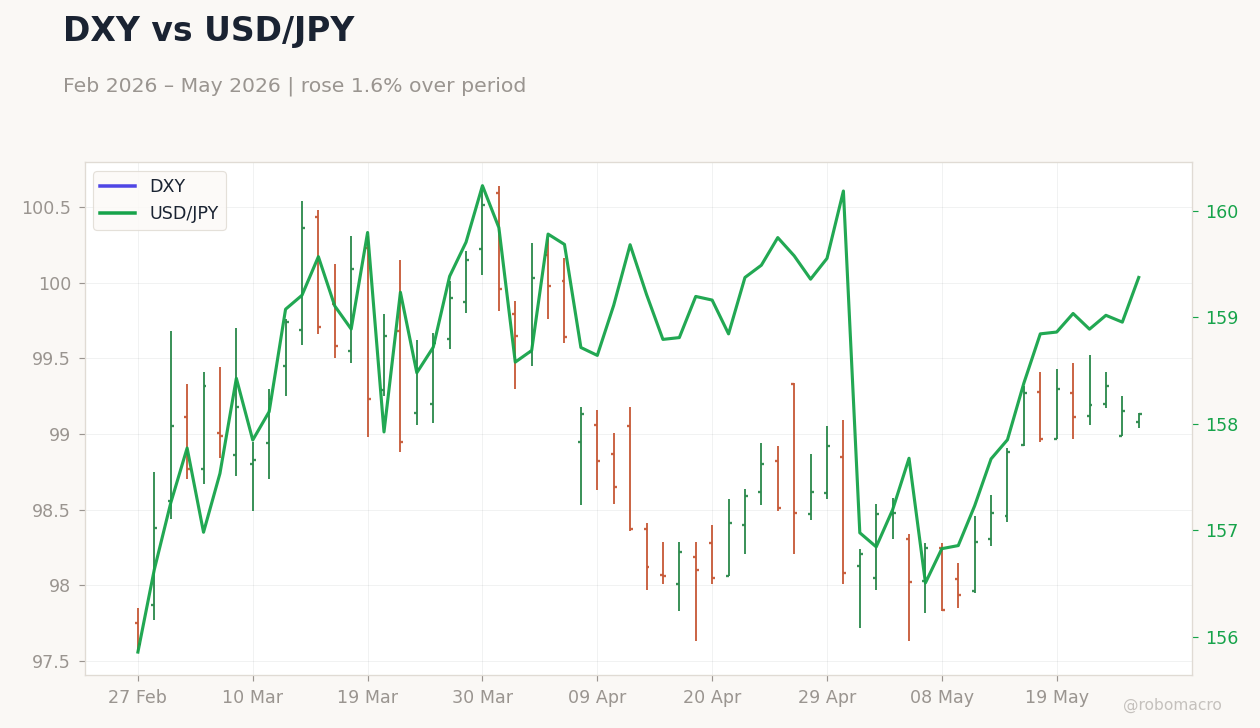

| USD/JPY | 159.38 | +0.27% |

| EUR/USD | 1.16 | +0.05% |

| GBP/USD | 1.34 | -0.41% |

| Gold | 4,478.80 | -0.48% |

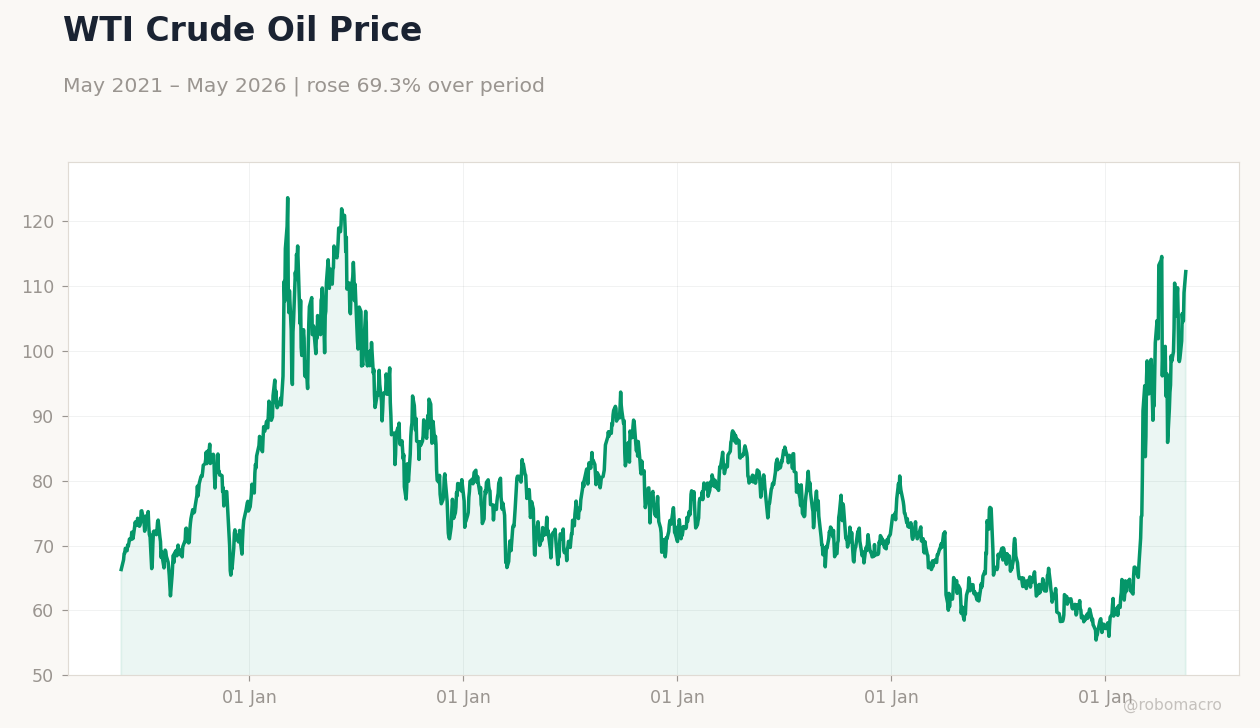

| WTI Crude | 90.30 | -3.82% |

| Bitcoin | 75,789.04 | -0.05% |

| US 2Y Treasury | 4.13% | +1.23% |

| US 10Y Treasury | 4.56% | -0.22% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Chicago Fed National Activity Index | -0.15 | - | 0.14 |

| S&P/Case-Shiller Home Price Year-over-Year | 0.90 | 1 | 0.80 |

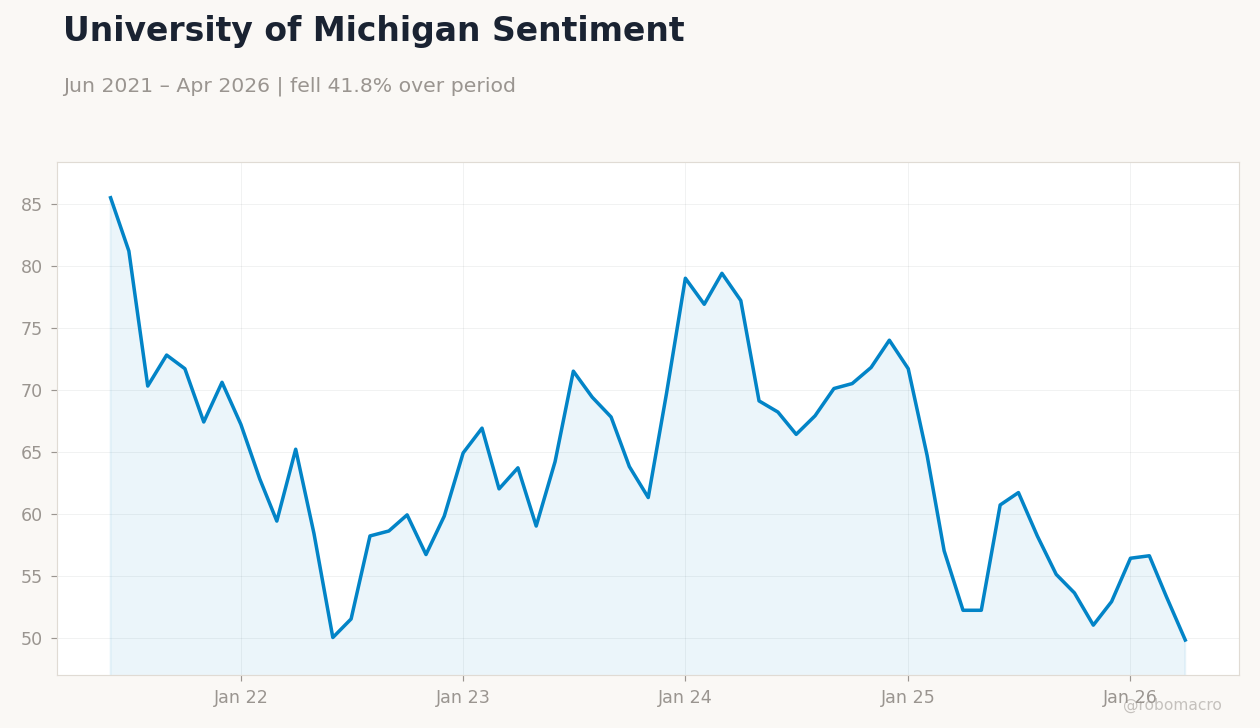

| Cb Consumer Confidence | 93.80 | - | 93.10 |

| Dallas Fed Manufacturing Index | -2.30 | - | 0.40 |

| Speech by Fed's Logan | - | - | - |

| MBA 30-Year Mortgage Rate | 6.56 | - | - |

10Y Treasury Yield | Type: macro_line | Percent: 4.56 (2026-05-22) | Range: 1.19–4.98 | Trend(6pt): 1.58,3.03,4.42,4.4,4.57,4.56 | 2Y Yield: 4.13 (2026-05-22) | Range: 0.13–5.19 | Trend(6pt): 0.14,3.35,4.89,4.13,4.08,4.13

10Y Treasury Yield | Type: macro_line | Percent: 4.56 (2026-05-22) | Range: 1.19–4.98 | Trend(6pt): 1.58,3.03,4.42,4.4,4.57,4.56 | 2Y Yield: 4.13 (2026-05-22) | Range: 0.13–5.19 | Trend(6pt): 0.14,3.35,4.89,4.13,4.08,4.13

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change Weekly | 42,250 | - | 04:15 |

| Fed Cook Speech | - | - | 11:55 |

| API Weekly Crude Oil Stocks | -9.1m | - | 12:30 |

| Speech by Fed's Jefferson | - | - | 16:00 |

| Thursday (2026-05-28) | |||

| Core PCE Price Index Month-over-Month | 0.30 | 0.30 | 04:30 |

| Durable Goods Orders Month-over-Month | 0.80 | 3.50 | 04:30 |

| GDP Growth Quarter-over-Quarter Second Estimate | 0.50 | 2 | 04:30 |

| Personal Income Month-over-Month | 0.60 | 0.40 | 04:30 |

| Personal Spending Month-over-Month | 0.90 | 0.50 | 04:30 |

- US data mixed as Chicago Fed index rose to 0.14 while Case-Shiller home prices slowed to 0.8% YoY and consumer confidence fell to 93.1.

- Equities closed higher with Nasdaq 100 up 1.76% and S&P 500 gaining 0.61%, while WTI crude fell 3.82% to 90.30 amid Iran developments.

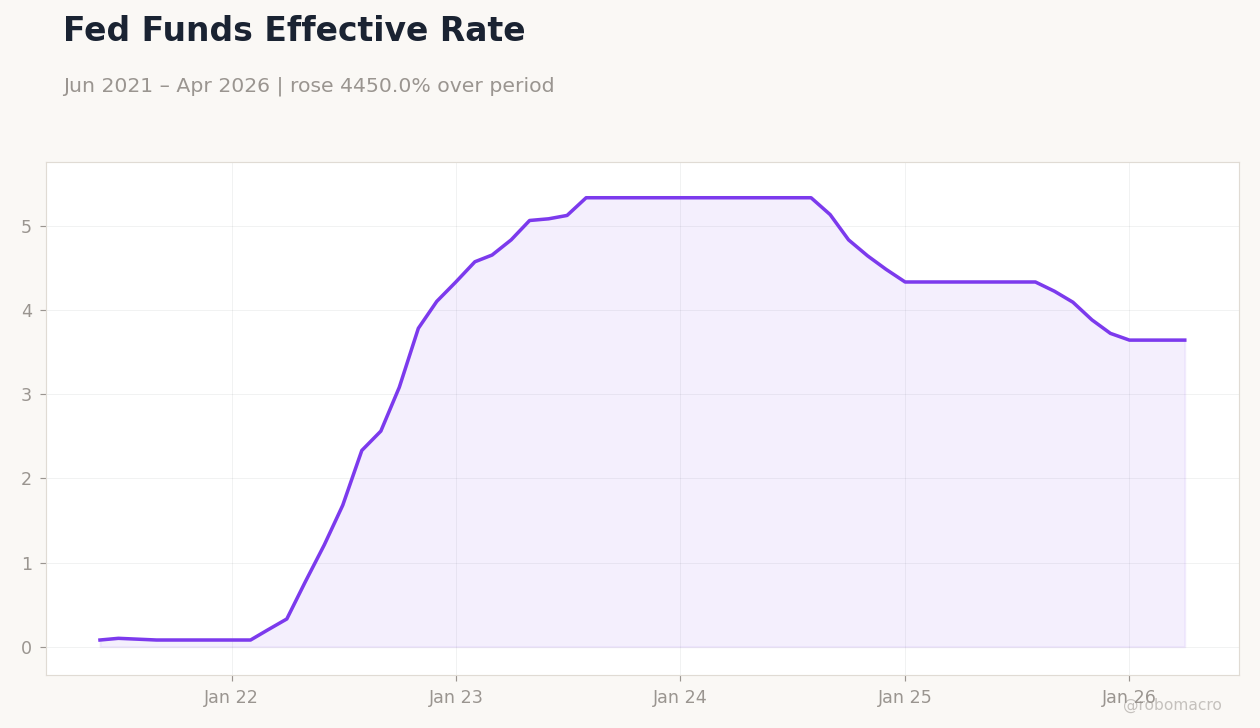

- Treasury yields showed divergence as 2-year rose to 4.13% and 10-year eased to 4.56%, with Fed Funds steady at 3.62%.

Yesterday's Recap

US data releases showed resilience in activity measures but softening in housing and sentiment. The Chicago Fed National Activity Index climbed to 0.14 from -0.15, while the Dallas Fed Manufacturing Index turned positive at 0.4. Case-Shiller home prices rose 0.8% YoY, below the 1.0% consensus, and consumer confidence slipped to 93.1.

Markets responded with broad equity gains led by technology stocks, as the Nasdaq 100 surged 1.76% to 30,001.32 and the S&P 500 added 0.61% to 7,519.12. WTI crude dropped sharply by 3.82% to 90.30 on reports of US strikes in Iran. The 2-year Treasury yield climbed 1.23% to 4.13%, while the 10-year eased 0.22% to 4.56%.

USD/JPY advanced 0.27% to 159.38.

The Day Ahead

Attention turns to ADP employment data and speeches from Fed officials Cook and Jefferson. API crude oil inventory figures will also be released later today. Tomorrow brings high-impact releases including core PCE, durable goods orders, the second GDP estimate, and personal income.

Markets will scrutinize the GDP revision for signs of stronger growth that could influence rate expectations. Fed speakers are expected to address monetary policy and financial imbalances. No major FOMC decisions are scheduled.

Other Economic Notes

Unemployment stands at 4.30% and CPI YoY at 2.31%, pointing to a labor market that remains balanced amid gradual disinflation. Equity markets continue to price a soft-landing scenario supported by AI-driven earnings momentum. Treasury market signals remain mixed, with shorter yields reflecting tighter policy expectations.

Broader fiscal developments, including recent spending legislation, have reduced near-term uncertainty for growth forecasts.

Global Macro News

US strikes in Iran have clouded prospects for a quick resolution and reopening of the Strait of Hormuz, pushing oil prices lower despite earlier optimism. A potential Hormuz blockade could severely disrupt global supply chains and energy markets, according to Fed warnings. <i>↓ p.2</i>