US Macro Daily(Beta Mode)

ISM Beats as Oil Climbs on Iran Tensions

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,599.96 | +0.26% |

| Nasdaq 100 | 30,513.86 | +0.60% |

| Dow Jones | 51,078.88 | +0.09% |

| Russell 2000 | 2,905.76 | -0.47% |

| USD/JPY | 159.76 | +0.25% |

| EUR/USD | 1.17 | +0.06% |

| GBP/USD | 1.35 | +0.18% |

| Gold | 4,561.30 | +1.92% |

| WTI Crude | 90.91 | -1.36% |

| Bitcoin | 69,030.39 | -3.21% |

| US 2Y Treasury | 3.98% | -0.25% |

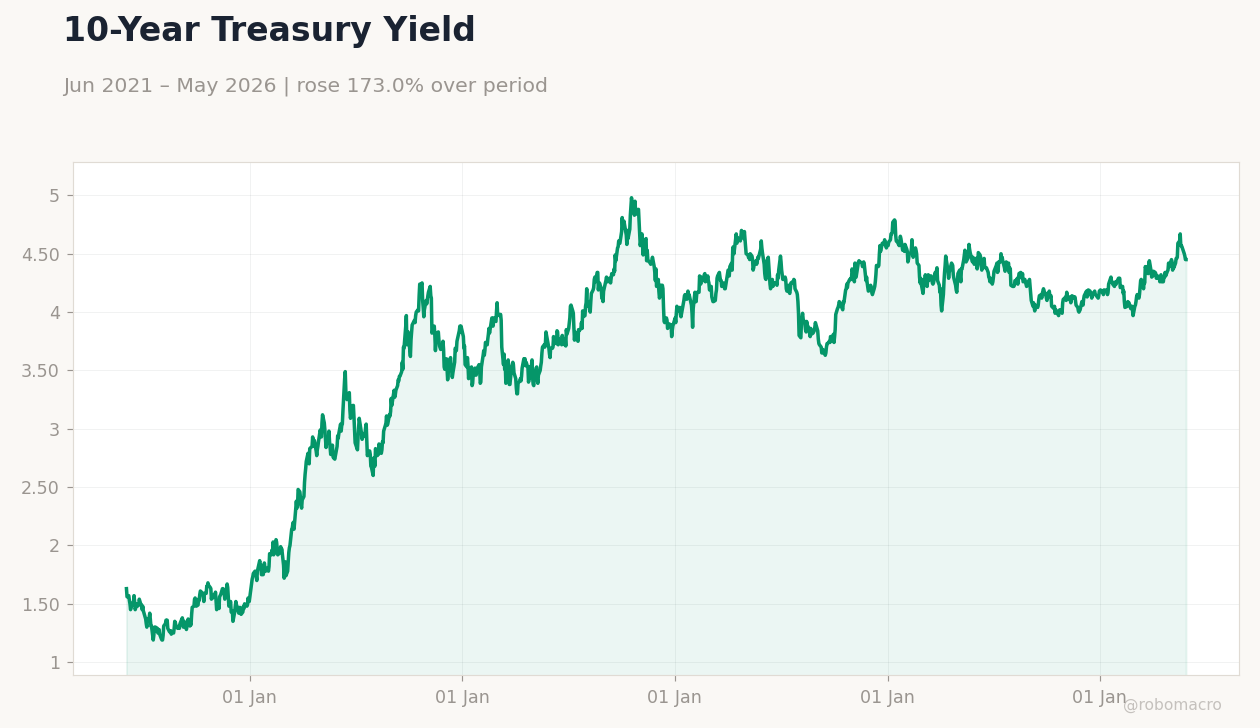

| US 10Y Treasury | 4.45% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ISM Manufacturing PMI | 52.70 | 53 | 54 |

| ISM Manufacturing Employment | 46.40 | - | 48.60 |

| Speech by Fed's Kashkari | - | - | - |

WTI Crude Oil Price | Type: macro_line | USD per Barrel: 97.63 (2026-05-26) | Range: 55.44–123.6 | Trend(6pt): 68.81,93.63,76.8,71.06,100.2,97.63

WTI Crude Oil Price | Type: macro_line | USD per Barrel: 97.63 (2026-05-26) | Range: 55.44–123.6 | Trend(6pt): 68.81,93.63,76.8,71.06,100.2,97.63

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Fed Hammack Speech | - | - | 04:30 |

| JOLTs Job Openings | 6.9m | 6.8m | 06:00 |

| API Weekly Crude Oil Stocks | -2.8m | - | 12:30 |

| Wednesday (2026-06-03) | |||

| MBA 30-Year Mortgage Rate | 6.65 | - | 03:00 |

| ADP Employment Change | 109,000 | 110,000 | 04:15 |

| Speech by Fed's Barr | - | - | 05:00 |

| Services Sector PMI | 53.60 | 53.70 | 06:00 |

| Factory Orders Month-over-Month | 1.50 | 4.60 | 06:00 |

| EIA Weekly Crude Oil Inventory | -3.3m | - | 06:30 |

- ISM manufacturing PMI rose to 54.0 in May, beating consensus of 53.0 and signaling stronger factory activity.

- Equity markets closed mixed with Nasdaq 100 up 0.60% while Russell 2000 fell 0.47% amid geopolitical concerns.

- Gold advanced 1.92% to $4,561.30 as central banks diversify reserves away from US Treasuries.

Yesterday's Recap

US data showed manufacturing momentum accelerating with the ISM PMI climbing to 54.0 from 52.7 and employment sub-index rising to 48.6. Equities finished narrowly higher as the S&P 500 gained 0.26% and the Dow added 0.09%, while the 10-year Treasury yield held steady at 4.45%. Oil prices climbed after reports of renewed US-Iran military exchanges and stalled peace talks.

Gold posted its strongest daily gain in weeks, reflecting safe-haven demand. Fed Governor Kashkari delivered remarks that markets interpreted as neutral on near-term policy. The dollar index edged higher against most major currencies.

Bitcoin declined 3.21% to $69,030.

The Day Ahead

Markets will focus on the 6:00 a.m. JOLTs job openings report, expected to show 6.82 million openings. Fed President Hammack speaks at 4:30 a.m.

ET on economic conditions. ADP private payrolls and the services PMI are due tomorrow, alongside factory orders. Oil inventory data from API and EIA will influence energy prices.

Treasury yields may react to any hawkish comments from Hammack on inflation persistence.

Other Economic Notes

US unemployment stands at 4.30% and CPI at 2.31% year-over-year, keeping the policy rate at 3.62%. Central banks continue shifting reserves toward gold, which now accounts for 27% of global holdings according to ECB data. Treasury market liquidity remains adequate despite the shift, but higher gold prices signal reduced appetite for dollar assets.

Manufacturing employment gains suggest labor demand in goods-producing sectors is stabilizing.

Global Macro News

US-Iran tensions lifted oil prices and pressured equities outside energy sectors. The US and Vietnam pledged to avoid currency manipulation and increase transparency in foreign exchange operations. <i>↓ p.2</i>