US Macro Daily(Beta Mode)

JOLTs Beat and ISM Strength Lift Equities

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,609.78 | +0.13% |

| Nasdaq 100 | 30,660.60 | +0.48% |

| Dow Jones | 51,307.79 | +0.45% |

| Russell 2000 | 2,931.96 | +0.90% |

| USD/JPY | 159.90 | +0.16% |

| EUR/USD | 1.16 | -0.25% |

| GBP/USD | 1.34 | -0.17% |

| Gold | 4,484.10 | -0.11% |

| WTI Crude | 96.23 | +2.63% |

| Bitcoin | 67,010.25 | +0.46% |

| US 2Y Treasury | - | - |

| US 10Y Treasury | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ISM Manufacturing PMI | 52.70 | 53 | 54 |

| ISM Manufacturing Employment | 46.40 | - | 48.60 |

| Speech by Fed's Kashkari | - | - | - |

| Fed Hammack Speech | - | - | - |

| JOLTs Job Openings | 6.9m | 6.9m | 7.6m |

| API Weekly Crude Oil Stocks | -2.8m | -3.6m | -6.8m |

| MBA 30-Year Mortgage Rate | 6.65 | - | - |

Nonfarm Payrolls (Employment) | Type: macro_line | Thousands of Persons: 1.587e+05 (2026-04-01) | Range: 1.468e+05–1.587e+05 | Trend(6pt): 1.468e+05,1.536e+05,1.567e+05,1.583e+05,1.586e+05,1.587e+05

Nonfarm Payrolls (Employment) | Type: macro_line | Thousands of Persons: 1.587e+05 (2026-04-01) | Range: 1.468e+05–1.587e+05 | Trend(6pt): 1.468e+05,1.536e+05,1.567e+05,1.583e+05,1.586e+05,1.587e+05

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change | 109,000 | 117,000 | 04:15 |

| Speech by Fed's Barr | - | - | 05:00 |

| Services Sector PMI | 53.60 | 53.80 | 06:00 |

| Factory Orders Month-over-Month | 1.50 | 4.60 | 06:00 |

| EIA Weekly Crude Oil Inventory | -3.3m | -2.9m | 06:30 |

| EIA Weekly Gasoline Inventory | -2.6m | - | 06:30 |

| Fed Goolsbee Speech | - | - | 07:00 |

| Speech by Fed's Logan | - | - | 12:00 |

- ISM Manufacturing PMI climbed to 54.0, exceeding the 53.0 consensus and marking the strongest reading since late 2025.

- JOLTs job openings jumped to 7.618 million, well above the 6.88 million consensus and prior 6.887 million.

- Equities posted modest gains with S&P 500 up 0.13 percent to 7,609.78 while WTI crude rose 2.63 percent to 96.23 on inventory draws.

Yesterday's Recap

US data releases surprised to the upside on June 2. ISM Manufacturing PMI printed at 54.0 while the employment sub-index rose to 48.6 from 46.4. JOLTs job openings reached 7.618 million, the largest beat in several months and consistent with gradual labor-market cooling rather than abrupt weakening.

Fed speakers Kashkari and Hammack delivered remarks that markets interpreted as neutral on near-term policy. Equities advanced across the board, led by Russell 2000 gains of 0.90 percent. WTI crude climbed sharply after API reported a 6.75 million barrel draw.

Treasury yields were little changed ahead of today’s data slate.

The Day Ahead

ADP private payrolls, ISM Services PMI, and Factory Orders headline the June 3 calendar. ADP is expected to show 117,000 jobs added while Services PMI is forecast at 53.8. Factory Orders are projected to rise 4.6 percent month-over-month.

EIA crude and gasoline inventory figures follow at 6:30 a.m. ET. Speeches from Fed Governors Barr, Goolsbee, and Logan will provide fresh guidance on the policy path.

Markets will focus on whether services strength offsets the earlier manufacturing beat.

Other Economic Notes

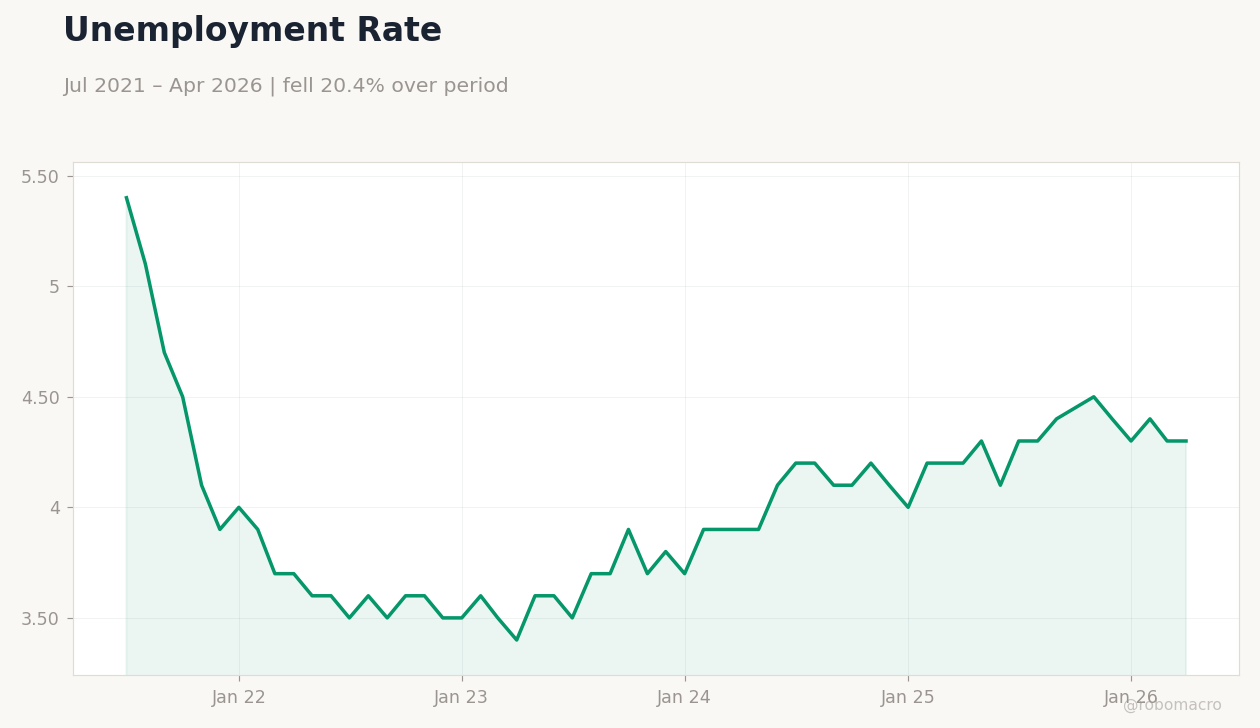

Stronger-than-expected labor demand data reinforce the view that the economy retains momentum despite the 4.30 percent unemployment rate. Oil inventory draws and rising WTI prices add to headline inflation risks even as core CPI sits at 2.31 percent. Equity markets continue to price resilient growth, with the S&P 500 holding above 7,600.

The combination of firm demand indicators and contained unemployment supports the current Fed Funds rate of 3.62 percent.

Global Macro News

The Trump administration proposed a 25 percent tariff on Brazilian imports despite a US trade surplus with the country. India and the United States are reported 99 percent complete on the first phase of a bilateral trade agreement. Iranian drone strikes on Kuwait’s airport and subsequent US-Iran exchanges lifted oil prices globally.

<i>↓ p.2</i>