US Macro Daily(Beta Mode)

Robust Jobs Data, ISM Lift Dow to Record

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,584.31 | +0.41% |

| Nasdaq 100 | 30,407.81 | -0.53% |

| Dow Jones | 51,561.93 | +1.73% |

| Russell 2000 | 2,935.33 | +1.45% |

| USD/JPY | 160.18 | +0.15% |

| EUR/USD | 1.15 | -0.70% |

| GBP/USD | 1.33 | -0.67% |

| Gold | 4,347.20 | -2.87% |

| WTI Crude | 90.20 | -3.05% |

| Bitcoin | 59,706.49 | -6.42% |

| US 2Y Treasury | - | - |

| US 10Y Treasury | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ISM Manufacturing PMI | 52.70 | 53 | 54 |

| ISM Manufacturing Employment | 46.40 | - | 48.60 |

| Speech by Fed's Kashkari | - | - | - |

| Fed Hammack Speech | - | - | - |

| JOLTs Job Openings | 6.9m | 6.9m | 7.6m |

| API Weekly Crude Oil Stocks | -2.8m | -3.6m | -6.8m |

| MBA 30-Year Mortgage Rate | 6.65 | - | 6.57 |

| ADP Employment Change | 105,000 | 117,000 | 122,000 |

| Speech by Fed's Barr | - | - | - |

| Services Sector PMI | 53.60 | 53.80 | 54.50 |

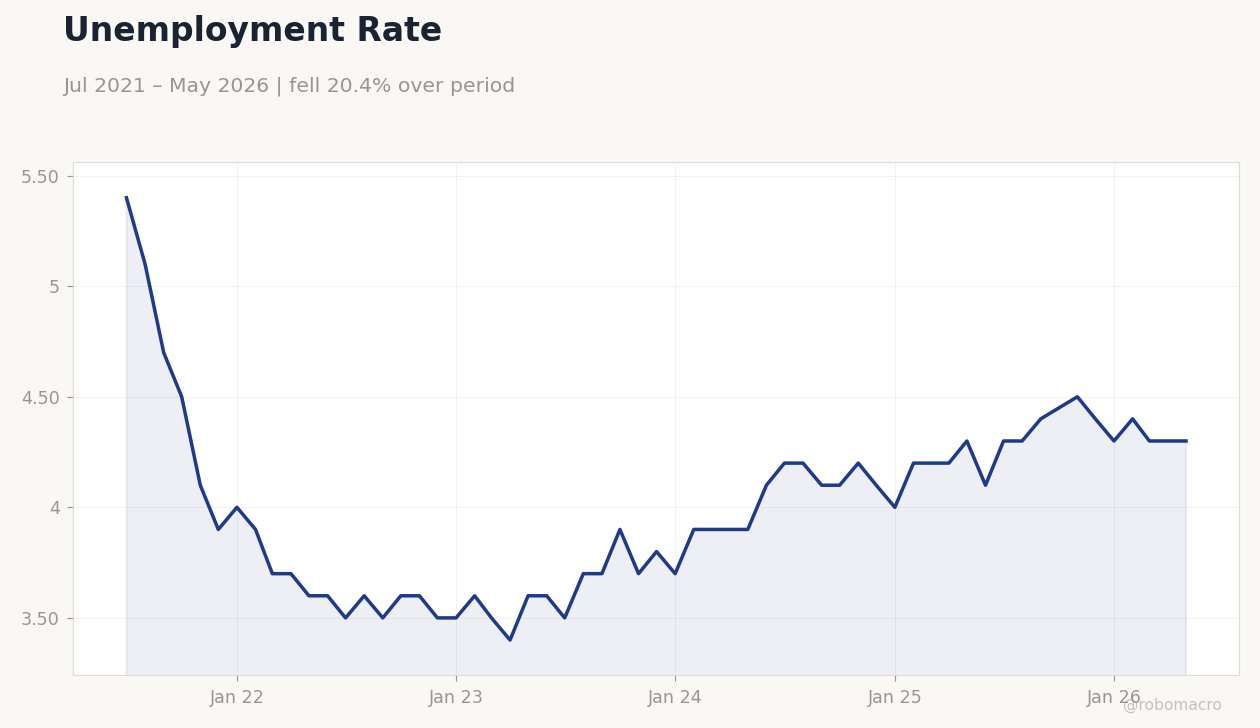

Unemployment Rate | Type: macro_line | Percent: 4.3 (2026-05-01) | Range: 3.4–5.4 | Trend(5pt): 5.4,3.5,3.7,4,4.3

Unemployment Rate | Type: macro_line | Percent: 4.3 (2026-05-01) | Range: 3.4–5.4 | Trend(5pt): 5.4,3.5,3.7,4,4.3

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Saturday (2026-06-06) | |||

| Speech by Fed's Barr | - | - | 08:00 |

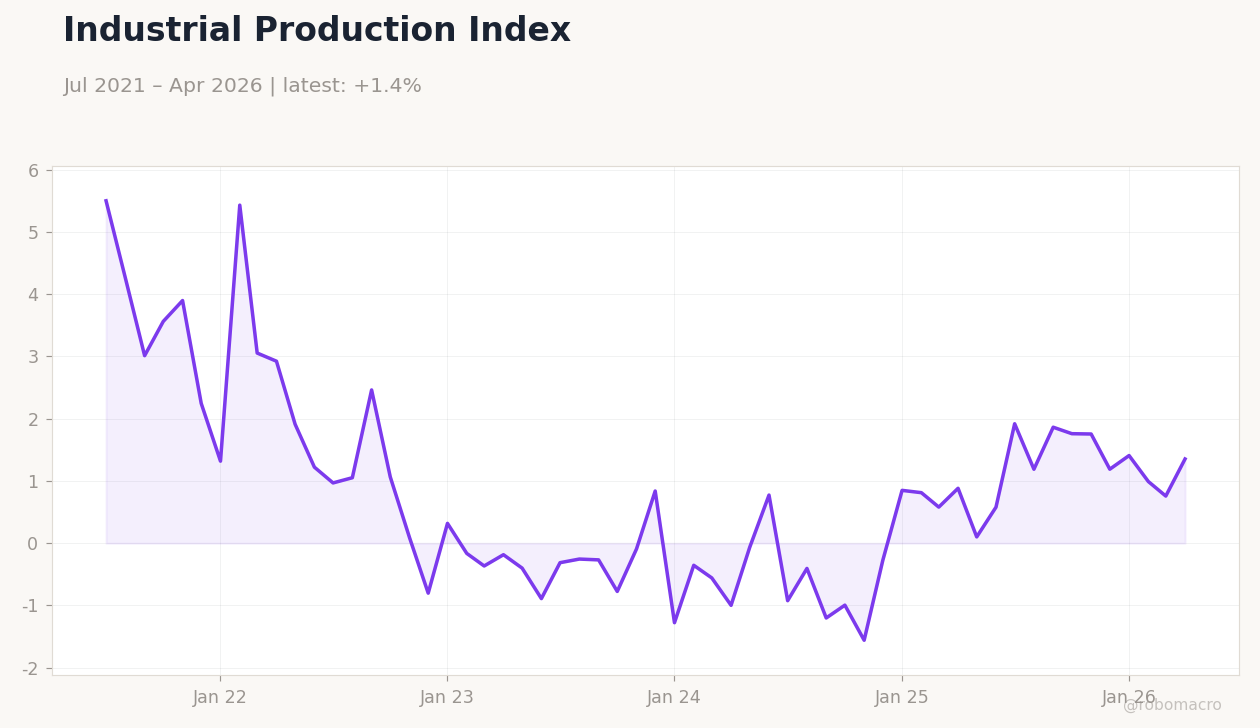

- ISM manufacturing PMI rose to 54.0 while services PMI reached 54.5, both exceeding forecasts

- JOLTs job openings surged to 7.618 million and ADP payrolls added 122,000

- Dow Jones climbed 1.73 percent to a fresh record high as S&P 500 gained 0.41 percent

Yesterday's Recap

ISM Manufacturing PMI printed at 54.0 against a 53.0 consensus, with the employment sub-index advancing to 48.6 from 46.4. JOLTs job openings jumped to 7.618 million, well above the 6.887 million prior reading. ADP private employment rose 122,000 versus 117,000 expected.

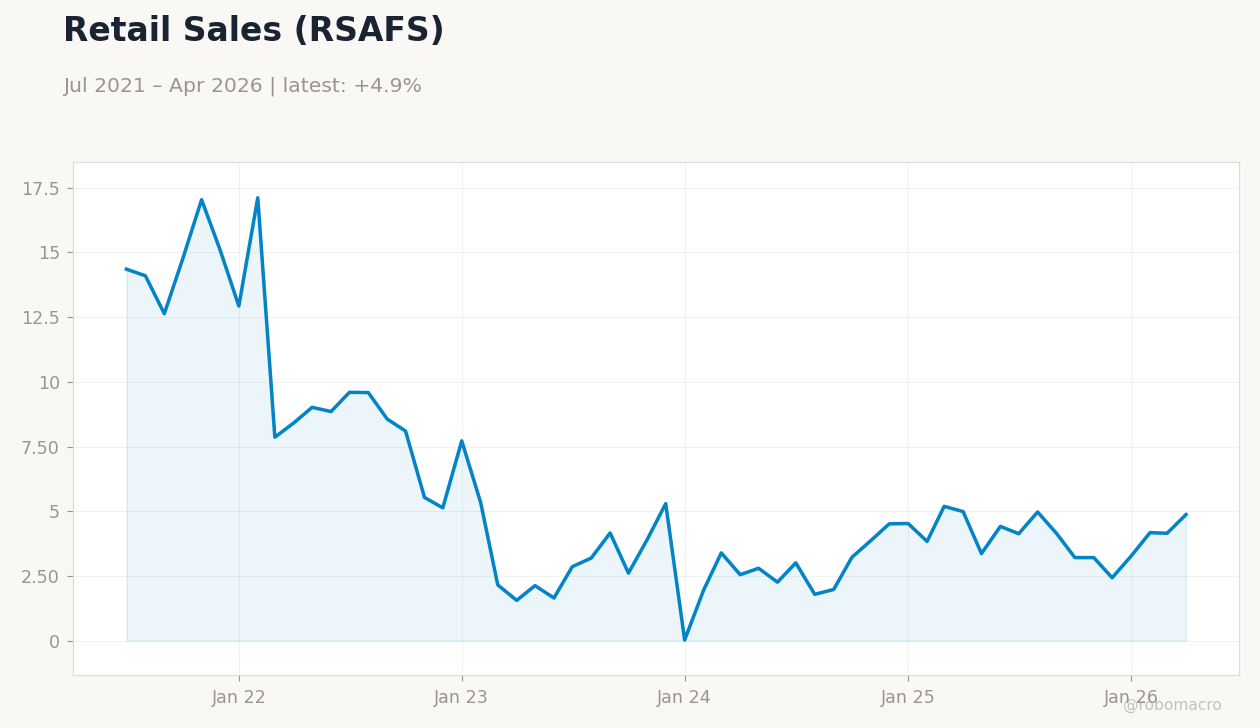

Services Sector PMI climbed to 54.5 from 53.6, and factory orders increased 4.8 percent month-over-month. The Dow Jones closed at 51,561.93 after a 1.73 percent gain, while the S&P 500 finished at 7,584.31, up 0.41 percent; the Nasdaq 100 slipped 0.53 percent. WTI crude fell 3.05 percent to 90.20 and gold dropped 2.87 percent to 4,347.20 amid the equity advance.

The Day Ahead

No major US data releases are scheduled for Friday, June 5. Markets will digest the prior day’s strong labor and PMI prints ahead of the weekend. Fed speakers including Goolsbee and Logan delivered remarks on Wednesday with no new policy signals.

Attention will turn to next week’s inflation and retail sales figures. Treasury futures are likely to remain range-bound until fresh catalysts emerge.

Other Economic Notes

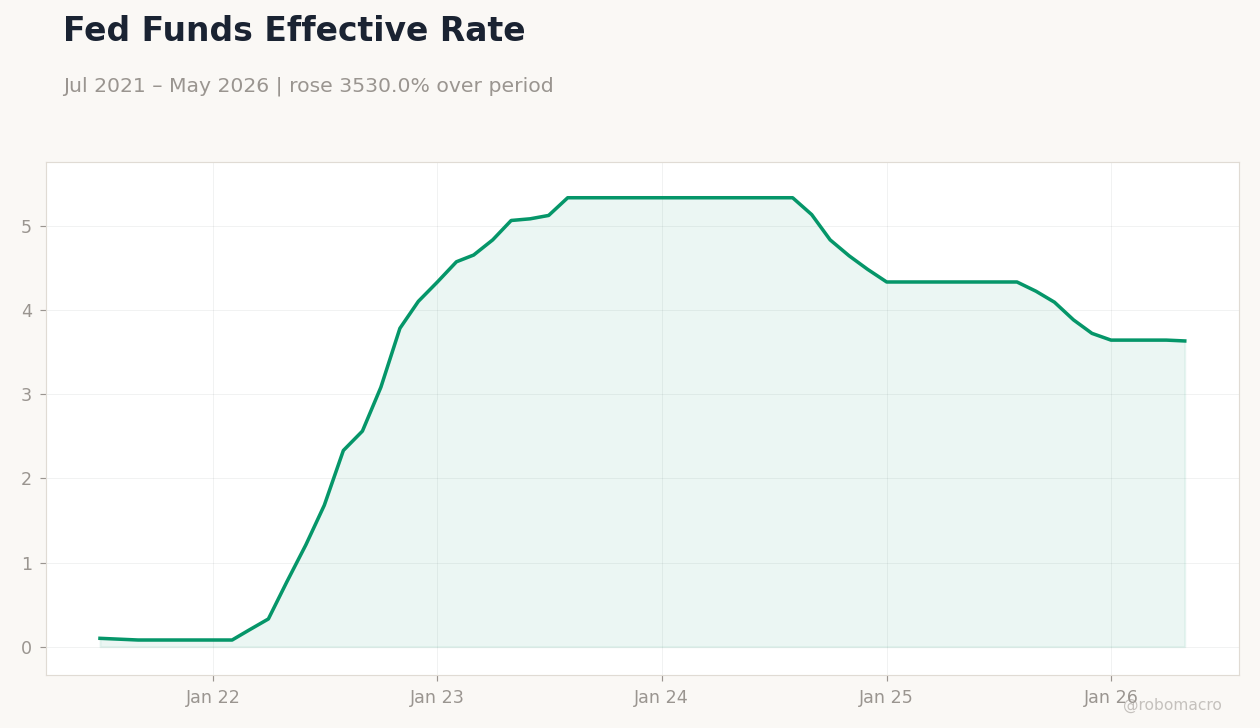

The US unemployment rate stands at 4.30 percent, supporting a resilient labor market narrative. CPI inflation registered 2.31 percent year-over-year in the latest available reading. An average 65-plus couple now requires roughly 1.16 million dollars in savings for comfortable retirement, according to fresh analysis.

USMCA renewal talks missed the July 1 target, raising the prospect of prolonged trade uncertainty with Mexico and Canada.

Global Macro News

The euro-zone economy contracted in the first quarter after Ireland’s sharp revision pulled the aggregate lower. Australian shares fell as iron-ore prices weakened and Middle East tensions flared. The Nigerian naira held steady against the dollar in both official and parallel markets.

US, Mexico and Canada face extended USMCA renegotiation, adding tariff risk. Western Forest Products workers in Canada joined the United Steelworkers union. <i>↓ p.2</i>