US Macro Daily(Beta Mode)

CPI Hits 4.2% as Equities Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,333.88 | -0.71% |

| Nasdaq 100 | 28,812.24 | -0.94% |

| Dow Jones | 50,347.10 | -1.03% |

| Russell 2000 | 2,862.49 | -0.16% |

| USD/JPY | 160.49 | +0.06% |

| EUR/USD | 1.15 | -0.08% |

| GBP/USD | 1.33 | -0.23% |

| Gold | 4,105.60 | -0.06% |

| WTI Crude | 90.42 | +0.43% |

| Bitcoin | 62,639.86 | +1.94% |

| US 2Y Treasury | - | - |

| US 10Y Treasury | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 30,500 | - | 29,000 |

| Exports Level | 318,800m | - | 327,100m |

| Imports Level | 375,400m | - | 383,000m |

| Trade Balance | -56,600m | -56,100m | -55,900m |

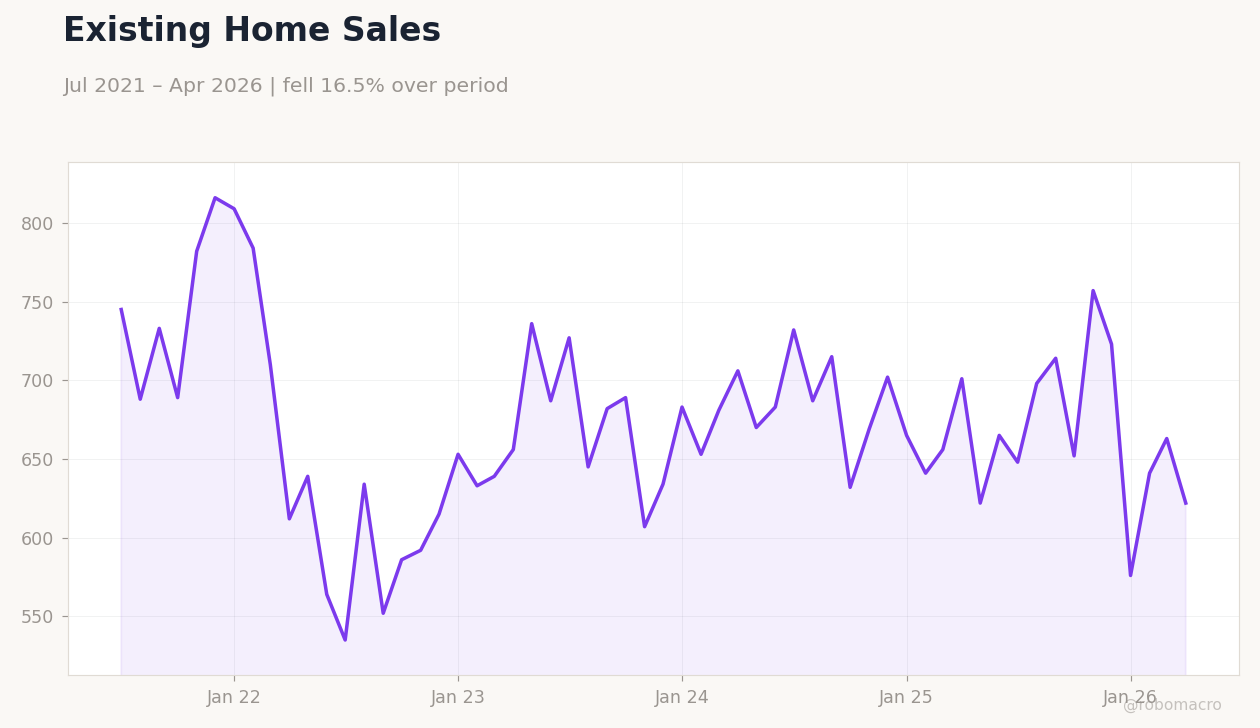

| Existing Home Sales | 4.0m | 4.1m | 4.2m |

| Existing Home Sales Month-over-Month | 0.70 | - | 3.20 |

| Eia Short-Term Energy Outlook | - | - | "" |

| MBA 30-Year Mortgage Rate | 6.57 | - | 6.60 |

| Core Inflation Rate Month-over-Month | 0.40 | 0.30 | 0.20 |

| Core Inflation Rate Year-over-Year | 2.80 | 2.90 | 2.90 |

US Core CPI YoY | Type: macro_line | YoY %: 2.957 (2026-05-01) | Range: 2.673–6.624 | Trend(6pt): 4.211,6.624,4.018,3.283,2.988,2.957

US Core CPI YoY | Type: macro_line | YoY %: 2.957 (2026-05-01) | Range: 2.673–6.624 | Trend(6pt): 4.211,6.624,4.018,3.283,2.988,2.957

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

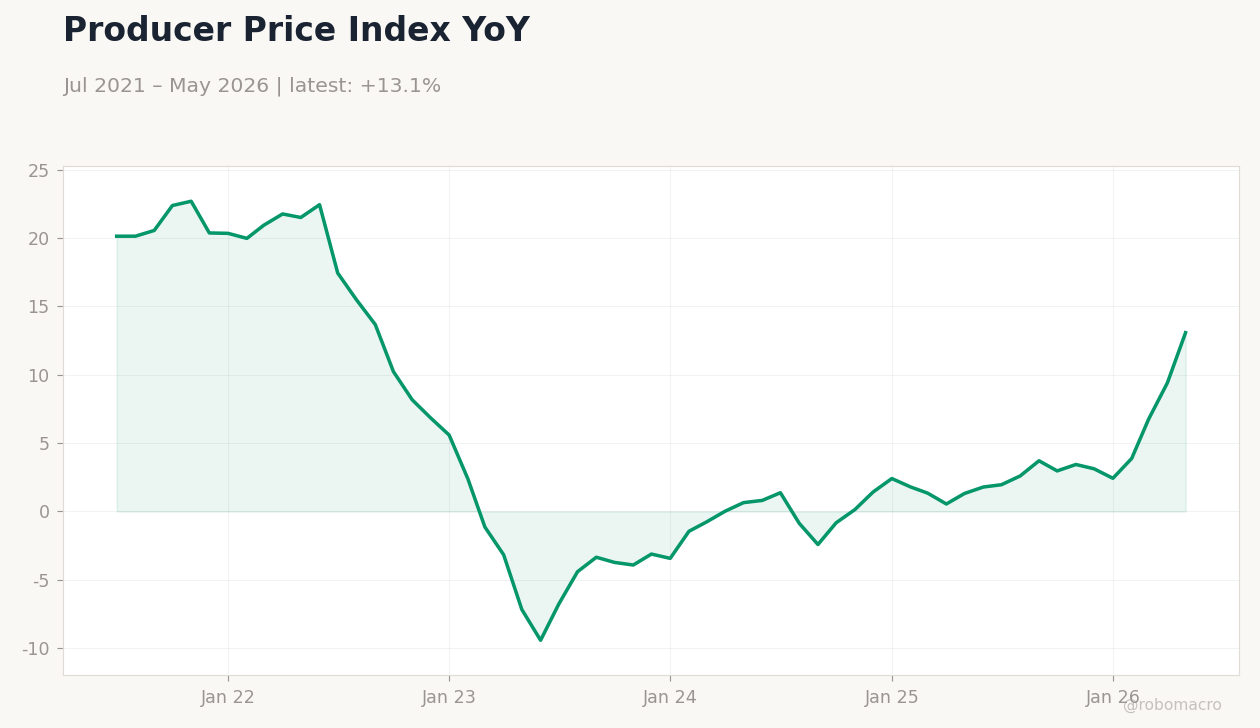

| Producer Price Index Month-over-Month | 1.40 | 0.70 | 04:30 |

| Core Producer Price Index Month-over-Month | 1 | 0.50 | 04:30 |

| Weekly Jobless Claims | 225,000 | 219,000 | 04:30 |

| Friday (2026-06-12) | |||

| Michigan Consumer Sentiment Prel | 44.80 | 46 | 06:00 |

- US CPI rose to 4.2% YoY in May, led by energy prices, while core held at 2.9%.

- Existing home sales jumped 3.2% MoM to 4.17 million, beating forecasts.

- Equities fell with S&P 500 down 0.71% amid higher-for-longer rate signals.

Yesterday's Recap

US data showed mixed inflation signals with headline CPI at 4.2% YoY and core at 2.9% YoY, both aligning with or slightly below consensus. Existing home sales surged to 4.17 million units, a 3.2% MoM gain that exceeded expectations and signaled housing resilience. Trade balance narrowed to -$55.9 billion as exports rose to $327.1 billion.

ADP employment change printed at 29,000, slightly below the prior 30,500. Markets reacted with broad equity declines: S&P 500 fell 0.71% to 7,333.88, Nasdaq 100 dropped 0.94%, and Dow Jones lost 1.03%. WTI crude climbed 0.43% to $90.42 on geopolitical supply concerns.

Bitcoin gained 1.94% to $62,639.86 while USD/JPY held near 160.49.

The Day Ahead

Markets will monitor any follow-up housing or energy data releases. Treasury yields remain in focus given the inflation print and upcoming Fed communications. Oil inventory draws of 7.228 million barrels may support energy prices.

Mortgage rates edged to 6.60%, potentially weighing on future housing activity. Equity volatility could persist ahead of any Fed speakers. USD crosses will track global risk sentiment tied to Middle East developments.

Other Economic Notes

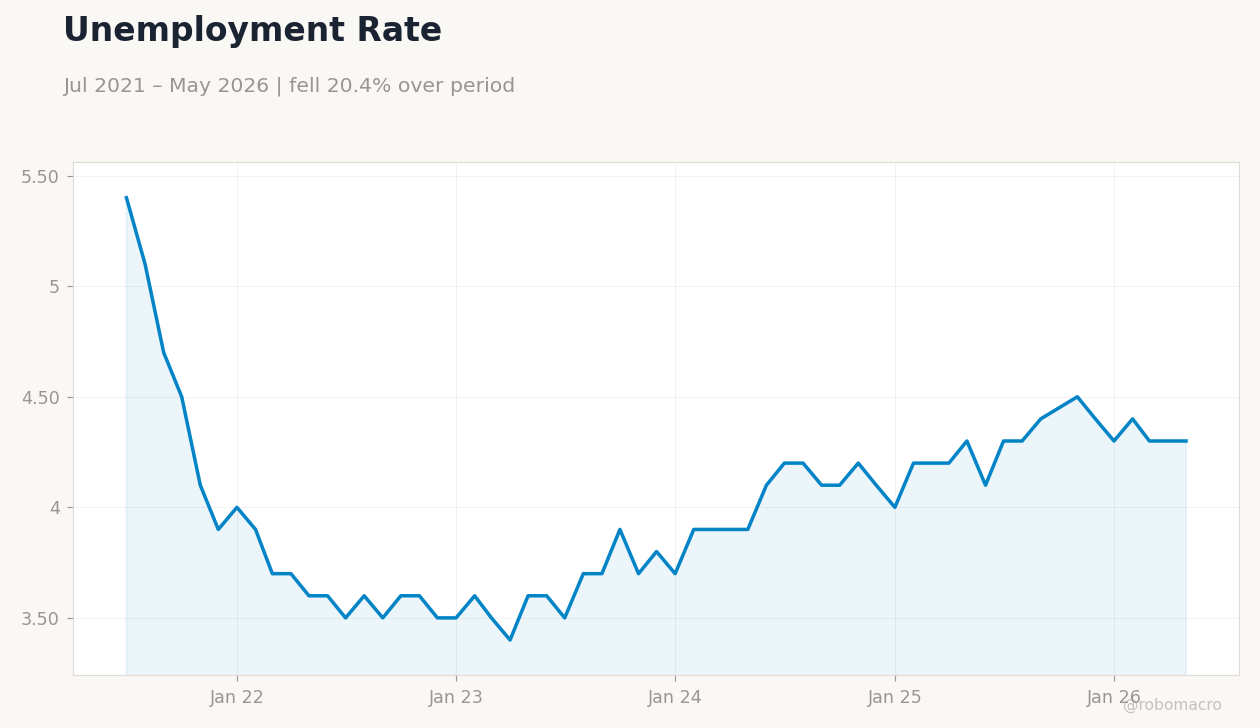

Inflation at 4.2% YoY marks the highest level in three years, fueled by gasoline and energy components. Unemployment stands at 4.3%, providing some labor-market slack that may temper wage pressures. The Fed funds rate at 3.62% anchors policy expectations.

Housing market rebound offers a counterweight to softening growth signals elsewhere. Broader price pressures remain concentrated in goods rather than services.

Global Macro News

President Trump signaled potential US action against Iranian oil infrastructure on Kharg Island, raising supply disruption risks. Gulf states condemned Iranian strikes on Bahrain, Kuwait, and Jordan, heightening regional tensions. Bank of Canada held its policy rate at 2.25% as economic growth flatlined.

<i>↓ p.2</i>