US Macro Daily(Beta Mode)

Core CPI Softens, Equities Rally on Housing Beat

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,394.30 | +1.75% |

| Nasdaq 100 | 29,446.18 | +3.29% |

| Dow Jones | 50,848.75 | +1.86% |

| Russell 2000 | 2,921.03 | +3.02% |

| USD/JPY | 160.19 | -0.21% |

| EUR/USD | 1.16 | +0.44% |

| GBP/USD | 1.34 | +0.44% |

| Gold | 4,236.50 | +3.57% |

| WTI Crude | 84.37 | -3.81% |

| Bitcoin | 64,074.34 | +0.81% |

| US 2Y Treasury | - | - |

| US 10Y Treasury | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 30,500 | - | 29,000 |

| Exports Level | 318,800m | - | 327,100m |

| Imports Level | 375,400m | - | 383,000m |

| Trade Balance | -56,600m | -56,100m | -55,900m |

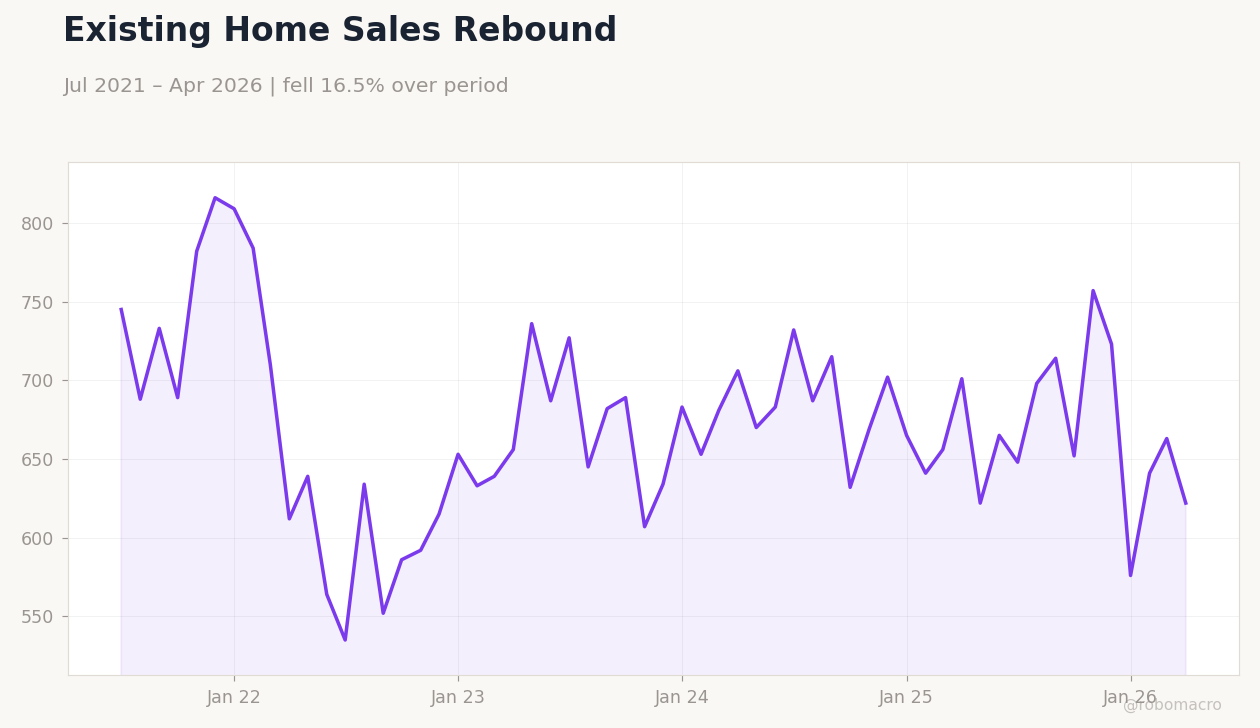

| Existing Home Sales | 4.0m | 4.1m | 4.2m |

| Existing Home Sales Month-over-Month | 0.70 | - | 3.20 |

| Eia Short-Term Energy Outlook | - | - | "" |

| MBA 30-Year Mortgage Rate | 6.57 | - | 6.60 |

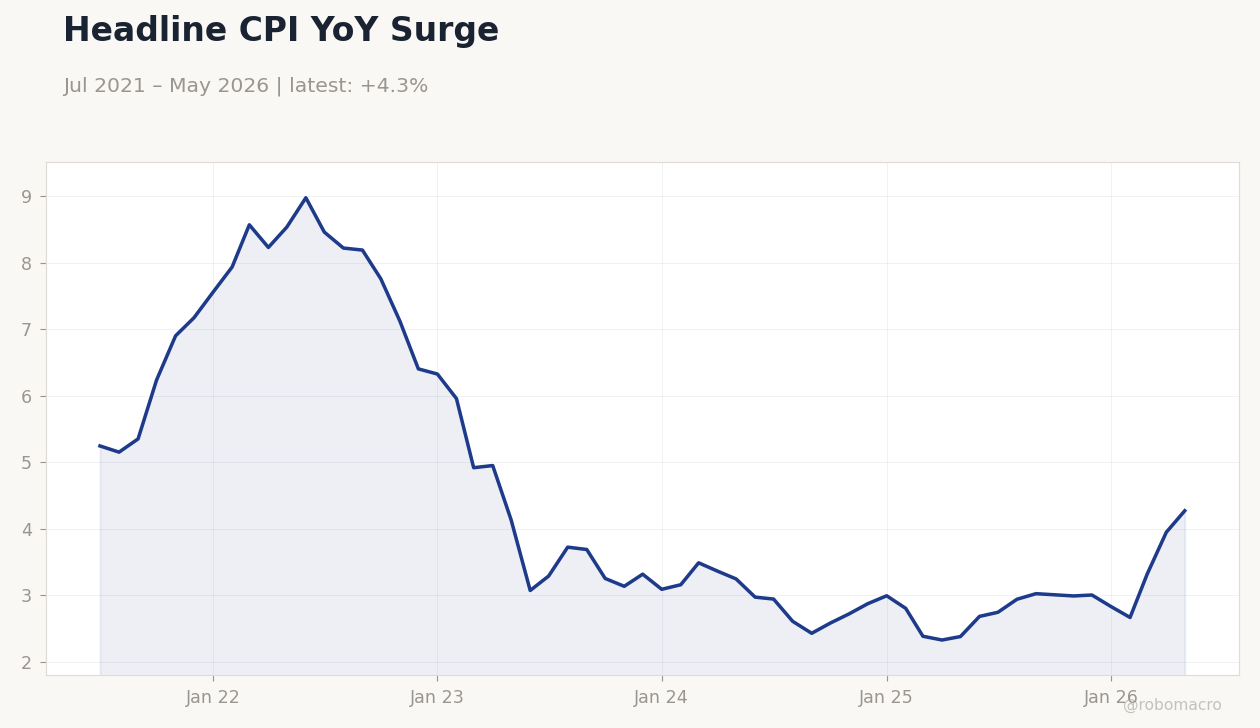

| Core Inflation Rate Month-over-Month | 0.40 | 0.30 | 0.20 |

| Core Inflation Rate Year-over-Year | 2.80 | 2.90 | 2.90 |

Headline CPI YoY Surge | Type: macro_line | CPI YoY %: 4.27 (2026-05-01) | Range: 2.325–8.979 | Trend(6pt): 5.245,8.192,3.133,2.991,3.947,4.27

Headline CPI YoY Surge | Type: macro_line | CPI YoY %: 4.27 (2026-05-01) | Range: 2.325–8.979 | Trend(6pt): 5.245,8.192,3.133,2.991,3.947,4.27

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

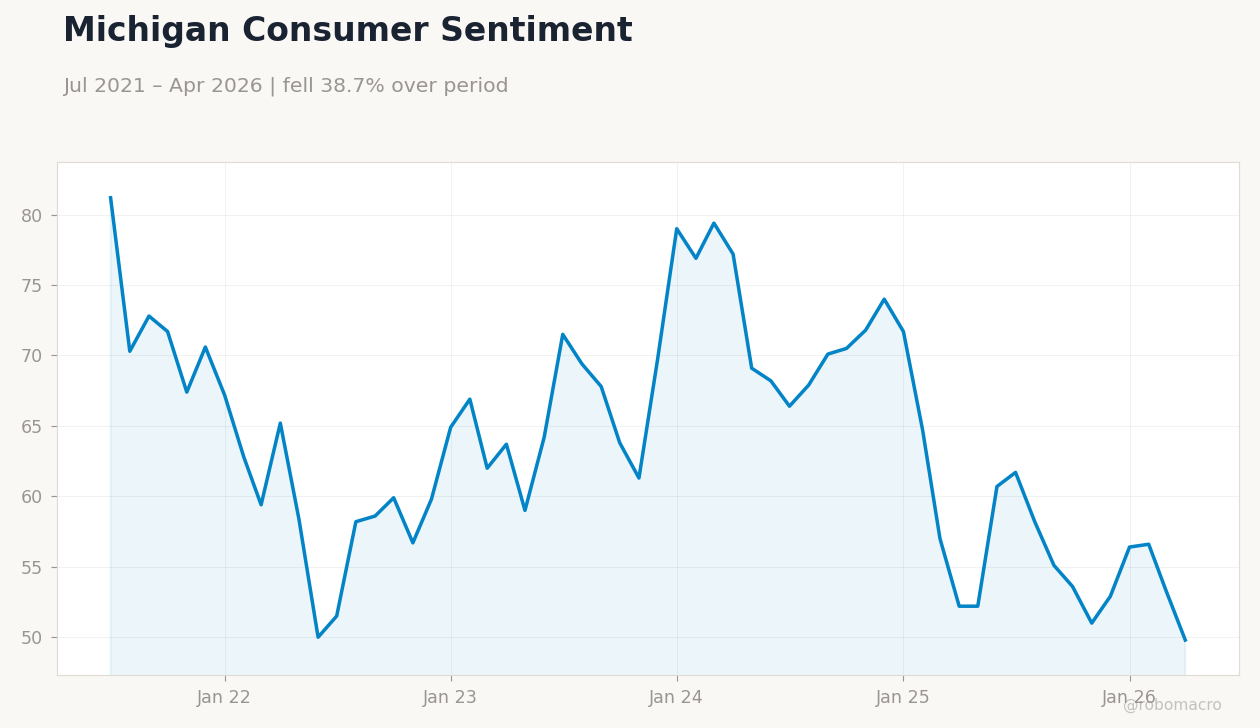

| Michigan Consumer Sentiment Prel | 44.80 | 46 | 06:00 |

- Core CPI rose just 0.2% m/m in May, below 0.3% consensus, while headline CPI held at 4.2% y/y.

- Existing home sales jumped 3.2% m/m to 4.17 million, beating forecasts and signaling housing resilience.

- Equities surged with S&P 500 up 1.75% and Nasdaq 100 gaining 3.29% as softer core inflation lifted risk appetite.

Yesterday's Recap

May CPI data released on June 10 showed core inflation moderating to 0.2% month-over-month against a 0.3% consensus, while the year-over-year rate matched expectations at 2.9%. Headline CPI printed 4.2% year-over-year with the index reaching 335.12. Existing home sales rose sharply to 4.17 million units, a 3.2% monthly gain that exceeded forecasts.

The trade balance narrowed to -$55.9 billion as exports climbed to $327.1 billion. Equity markets responded positively, with the S&P 500 advancing 1.75% to 7,394.30, the Nasdaq 100 surging 3.29%, and the Russell 2000 climbing 3.02%. Gold rose 3.57% to $4,236.50 while WTI crude fell 3.81% to $84.37 amid shifting supply signals.

Mortgage rates edged up to 6.6%.

The Day Ahead

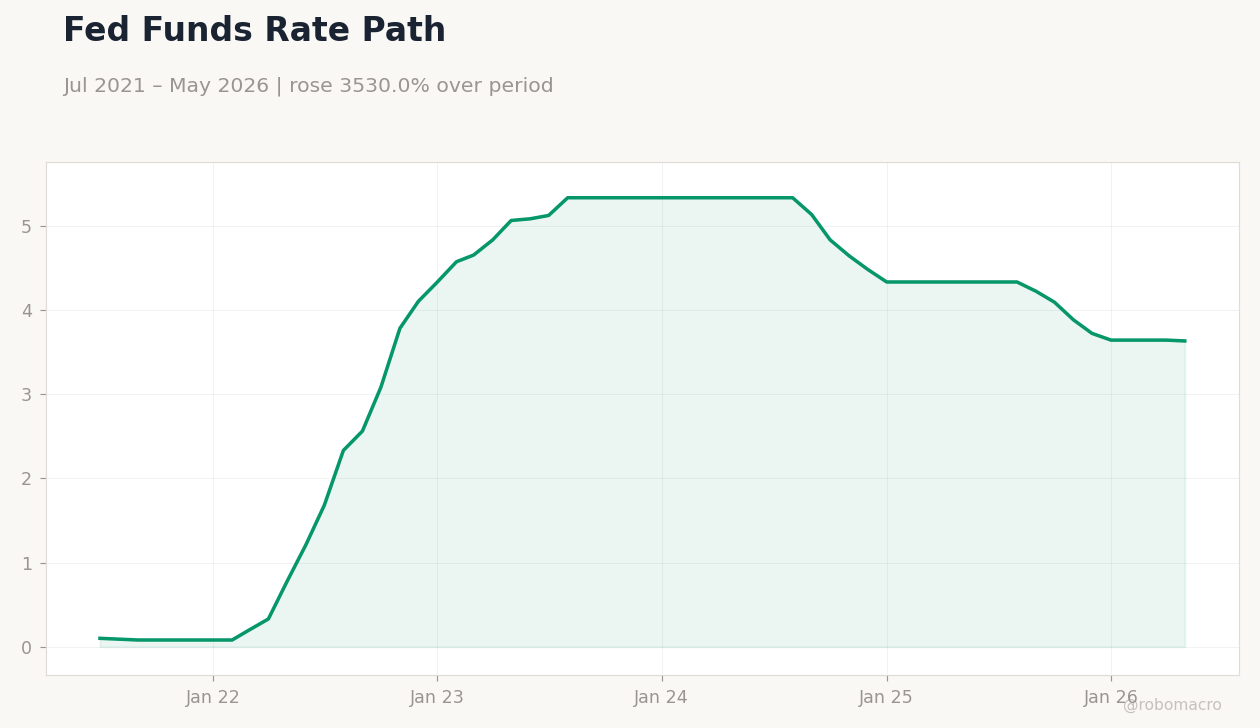

Attention turns to next week’s FOMC meeting under new Chair Kevin Warsh, where markets will parse any shift in forward guidance. Retail sales and initial jobless claims later this week could further shape rate expectations. Treasury yields remain in focus as participants assess whether the recent CPI moderation alters the path for the 3.62% fed funds rate.

Oil market volatility tied to Iran tensions may influence broader risk sentiment. Speakers from regional Fed banks are also scheduled and could offer early clues on the committee’s reaction function.

Other Economic Notes

The unemployment rate stands at 4.3%, providing the Fed with room to monitor labor-market cooling without immediate alarm. Housing data suggest demand remains firm despite elevated mortgage rates near 6.6%. Energy inventories drew down more than expected, supporting price stability even as geopolitical risks linger.

Broader price pressures appear contained on the core measure, consistent with a gradual return toward target.

Global Macro News

The ECB raised rates 25 basis points, tightening policy ahead of the FOMC and supporting the euro against the dollar. Trump’s renewed warnings on Iran pressured oil markets before partial de-escalation eased WTI prices. <i>↓ p.2</i>