US Macro Daily(Beta Mode)

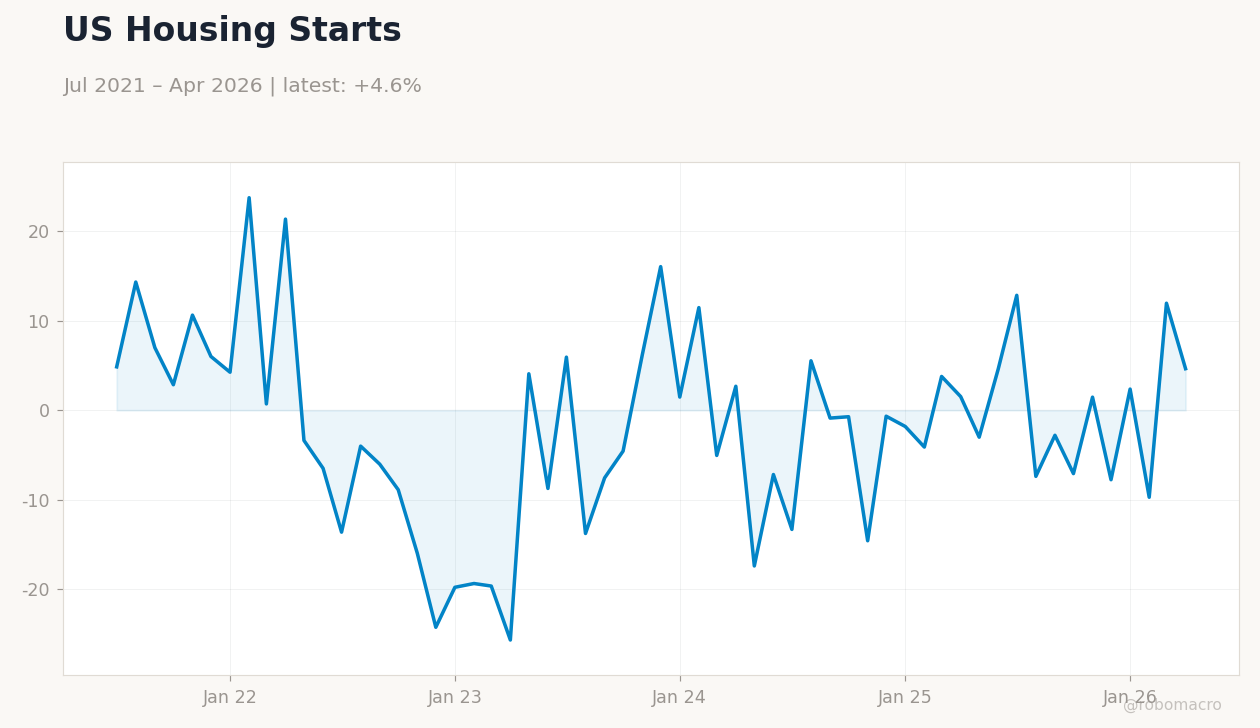

Empire State, IP Data Set Tone for Housing Week

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,431.46 | +0.50% |

| Nasdaq 100 | 29,635.95 | +0.64% |

| Dow Jones | 51,202.26 | +0.70% |

| Russell 2000 | 2,943.99 | +0.79% |

| USD/JPY | 160.13 | -0.25% |

| EUR/USD | 1.16 | +0.32% |

| GBP/USD | 1.34 | +0.15% |

| Gold | 4,384.50 | +4.02% |

| WTI Crude | 80.27 | -5.43% |

| Bitcoin | 66,433.02 | +1.10% |

| US 2Y Treasury | - | - |

| US 10Y Treasury | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

US Unemployment Rate | Type: macro_line | Percent: 4.3 (2026-05-01) | Range: 3.4–5.4 | Trend(5pt): 5.4,3.5,3.7,4,4.3

US Unemployment Rate | Type: macro_line | Percent: 4.3 (2026-05-01) | Range: 3.4–5.4 | Trend(5pt): 5.4,3.5,3.7,4,4.3

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NY Empire State Manufacturing Index | 19.60 | - | 04:30 |

| Industrial Production Month-over-Month | 0.70 | 0.20 | 05:15 |

| NAHB Housing Market Index | 37 | - | 06:00 |

| Tuesday (2026-06-16) | |||

| ADP Employment Change Weekly | 29,000 | - | 04:15 |

| Building Permits Prel | 1.4m | 1.4m | 04:30 |

| Housing Starts Level | 1.5m | 1.4m | 04:30 |

| Building Permits Month-over-Month Prel | 4.40 | - | 04:30 |

| Export Prices Month-over-Month | 3.30 | - | 04:30 |

| Housing Starts Month-over-Month | -2.80 | - | 04:30 |

- Equities advanced with S&P 500 up 0.50% to 7,431.46 as risk appetite improved ahead of industrial and housing prints.

- Gold surged 4.02% to $4,384.50 while WTI crude fell 5.43% to $80.27 on progress toward Hormuz reopening.

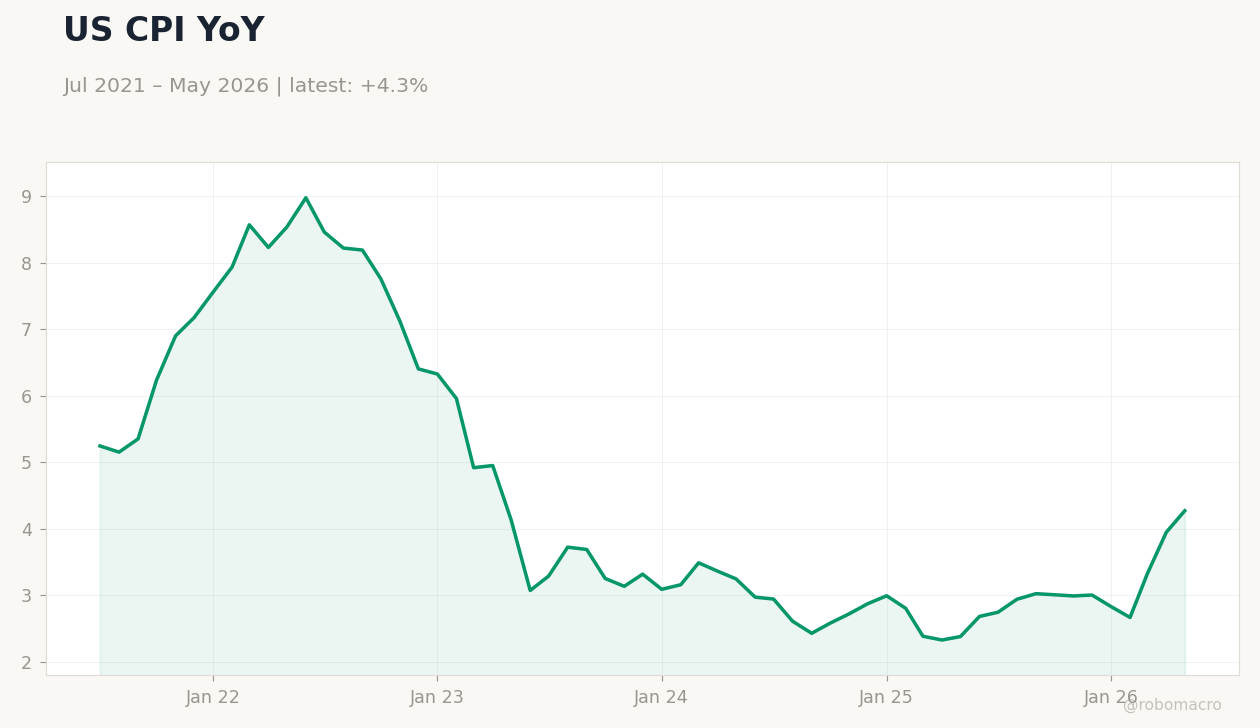

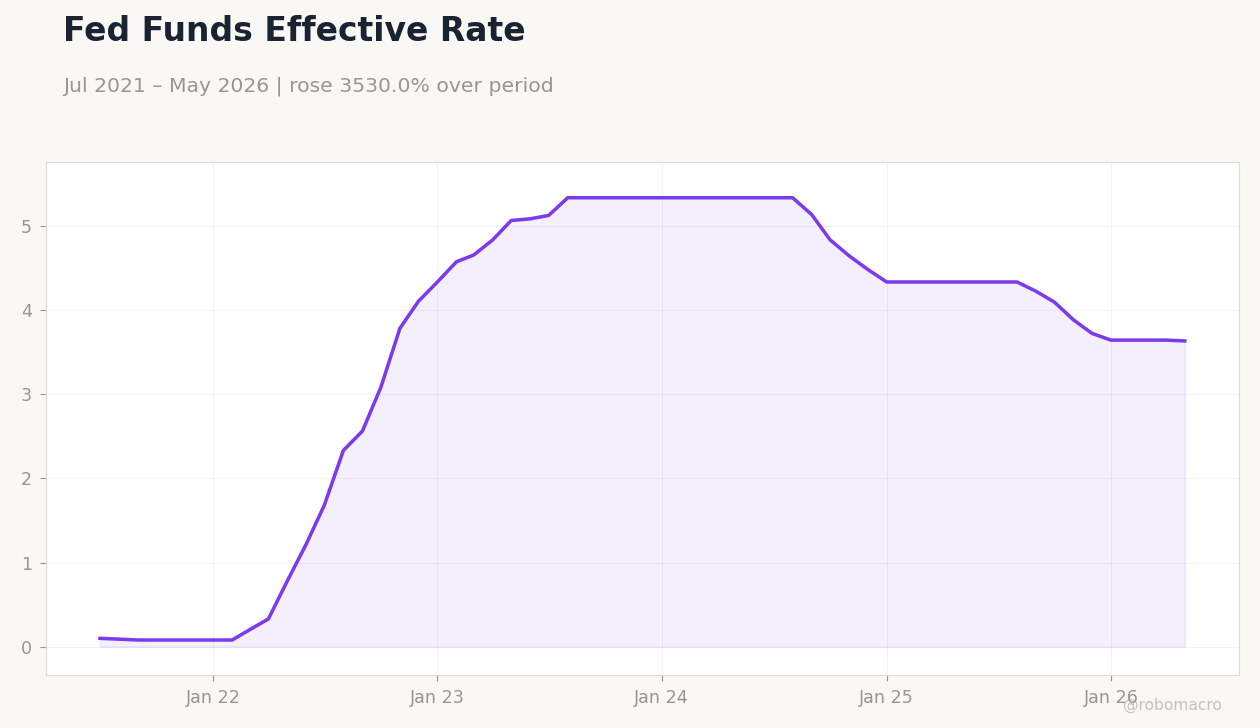

- Fed funds rate holds at 3.62% with CPI at 2.31% y/y and unemployment at 4.30%, keeping policy expectations anchored.

Yesterday's Recap

US markets posted solid gains on June 14 with no major data releases. The S&P 500 rose 0.50%, Nasdaq 100 gained 0.64%, Dow Jones advanced 0.70%, and Russell 2000 climbed 0.79%. USD/JPY eased 0.25% to 160.13 while EUR/USD rose 0.32% to 1.16.

Gold posted its strongest daily move in weeks, lifting 4.02%, as energy prices corrected sharply lower with WTI dropping 5.43%. Treasury yields were little changed in quiet trading ahead of this week's manufacturing and housing reports. Bitcoin added 1.10% to close at 66,433.02.

The Day Ahead

Focus shifts to the NY Empire State Manufacturing Index at 4:30 a.m. ET, followed by Industrial Production at 5:15 a.m. and the NAHB Housing Market Index at 6:00 a.m.

Tomorrow brings Building Permits and Housing Starts at 4:30 a.m., plus ADP employment figures. Retail Sales on Wednesday will provide the first read on consumer spending momentum. Markets will also monitor any updates from the G7 summit and Hormuz-related energy diplomacy.

Other Economic Notes

US industrial output faces mixed signals after last month's 0.7% gain, with consensus pointing to a 0.2% rise in May. Housing data remain central given persistent affordability constraints and elevated mortgage rates near 6.6%. Broader activity continues to reflect a labor market at 4.3% unemployment and contained inflation at 2.31% y/y, supporting a gradual policy path.

Energy price relief could further ease headline inflation readings in coming months.

Global Macro News

A deal to reopen the Strait of Hormuz has reduced near-term energy supply risks and contributed to today's sharp decline in WTI. European travel and tourism figures reached €30 billion, providing a modest positive impulse to euro-area services data. UK growth continues to diverge regionally, with Northern Ireland benefiting from its post-Brexit customs arrangements.

French authorities signaled readiness to support the Hormuz mission ahead of the G7. Broader global risk sentiment improved on the energy de-escalation, supporting USD crosses and equity flows into US assets.