US Macro Daily(Beta Mode)

Fed Holds Rates Amid Weak Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,431.46 | +0.50% |

| Nasdaq 100 | 29,635.95 | +0.64% |

| Dow Jones | 51,202.26 | +0.70% |

| Russell 2000 | 2,943.99 | +0.79% |

| USD/JPY | 160.38 | +0.27% |

| EUR/USD | 1.16 | +0.12% |

| GBP/USD | 1.34 | -0.10% |

| Gold | 4,351.30 | +0.54% |

| WTI Crude | 75.33 | -6.71% |

| Bitcoin | 65,837.81 | -0.68% |

| US 2Y Treasury | - | - |

| US 10Y Treasury | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NY Empire State Manufacturing Index | 19.60 | 14 | 5.70 |

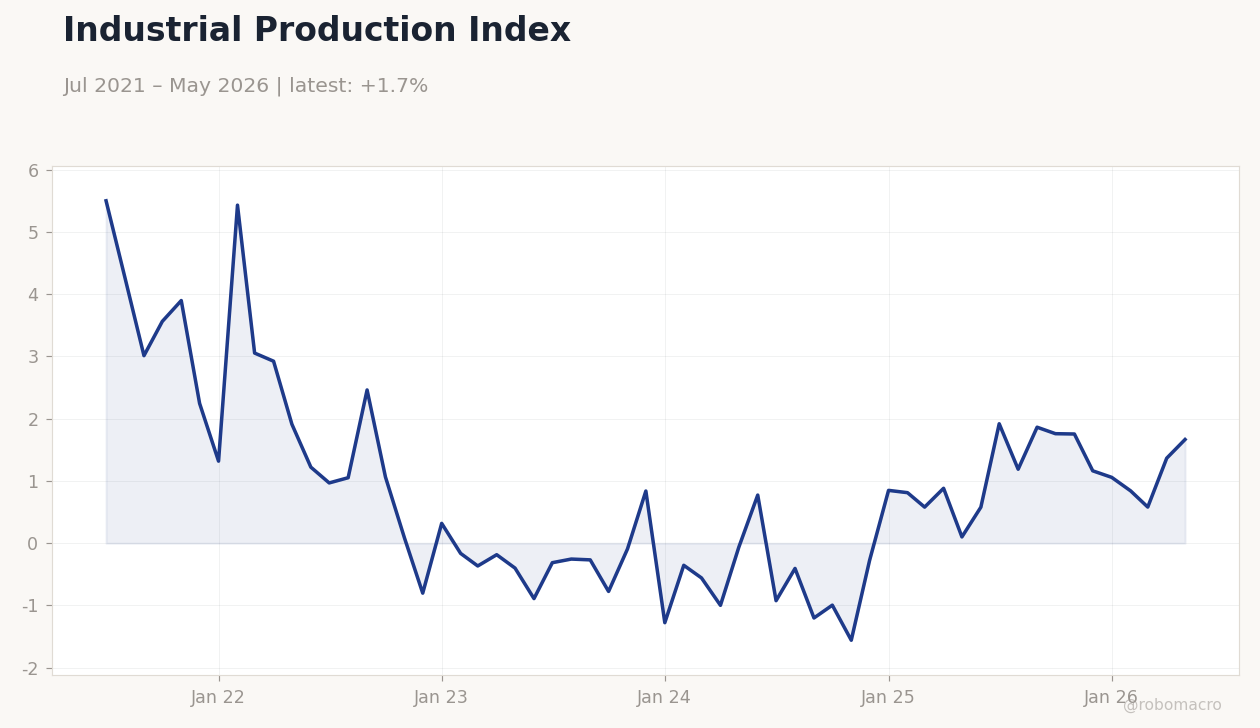

| Industrial Production Month-over-Month | 0.90 | 0.30 | 0.10 |

| NAHB Housing Market Index | 37 | 36 | 35 |

Industrial Production Index | Type: macro_line | Index (2017=100): 1.666 (2026-05-01) | Range: -1.558–5.5 | Trend(6pt): 5.5,2.462,-0.09044,0.849,0.5809,1.666

Industrial Production Index | Type: macro_line | Index (2017=100): 1.666 (2026-05-01) | Range: -1.558–5.5 | Trend(6pt): 5.5,2.462,-0.09044,0.849,0.5809,1.666

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change Weekly | 29,000 | - | 04:15 |

| Building Permits Prel | 1.4m | 1.4m | 04:30 |

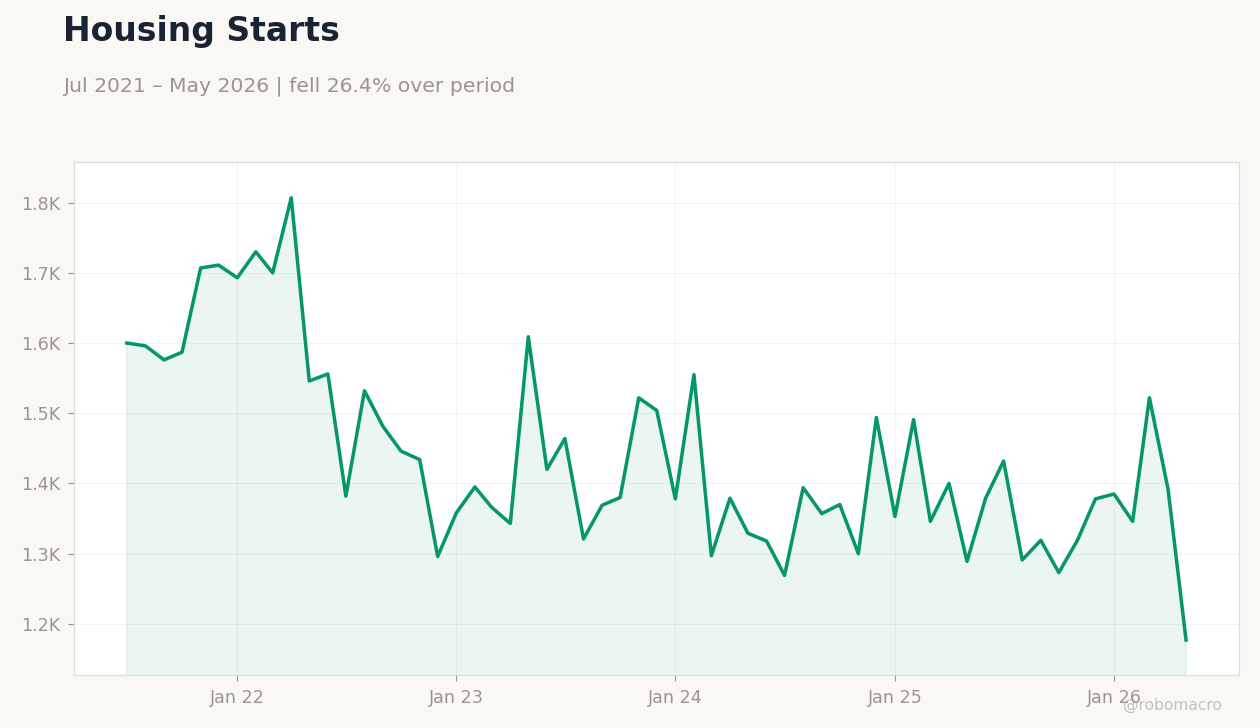

| Housing Starts Level | 1.5m | 1.4m | 04:30 |

| Building Permits Month-over-Month Prel | 4.40 | - | 04:30 |

| Export Prices Month-over-Month | 3.30 | 1.20 | 04:30 |

| Housing Starts Month-over-Month | -2.80 | - | 04:30 |

| Import Prices Month-over-Month | 1.90 | 1 | 04:30 |

| API Weekly Crude Oil Stocks | -9.1m | -4.5m | 12:30 |

- NY Empire State Manufacturing plunged to 5.7 from 19.6, missing consensus of 14

- Industrial Production rose just 0.1% MoM while NAHB Housing Index fell to 35

- Equities advanced with Dow up 0.70% as WTI Crude dropped 6.71% on easing supply concerns

Yesterday's Recap

US data releases showed clear softening in manufacturing and housing. The NY Empire State Manufacturing Index collapsed to 5.70, well below the 14 consensus and prior 19.60 reading. Industrial Production expanded only 0.1% month-over-month against expectations of 0.3%.

The NAHB Housing Market Index slipped to 35 from 37, signaling further cooling in homebuilder sentiment. Equity markets posted solid gains, with the S&P 500 rising 0.50%, Nasdaq 100 up 0.64%, and Dow Jones advancing 0.70%. Oil prices fell sharply, with WTI Crude declining 6.71% to 75.33 amid reports of improved geopolitical supply flows.

Gold climbed 0.54% to 4,351.30 while the dollar remained stable against major crosses.

The Day Ahead

Markets will focus on housing and labor indicators due this morning. Building Permits Prel and Housing Starts Level are both slated for release at 4:30 a.m. ET with consensus expectations of 1.42 million and 1.43 million respectively.

Export and Import Prices Month-over-Month prints will provide fresh inflation signals. ADP Employment Change Weekly follows at 4:15 a.m. ET.

API Weekly Crude Oil Stocks at 12:30 p.m. ET will set the tone ahead of tomorrow’s retail sales report.

Other Economic Notes

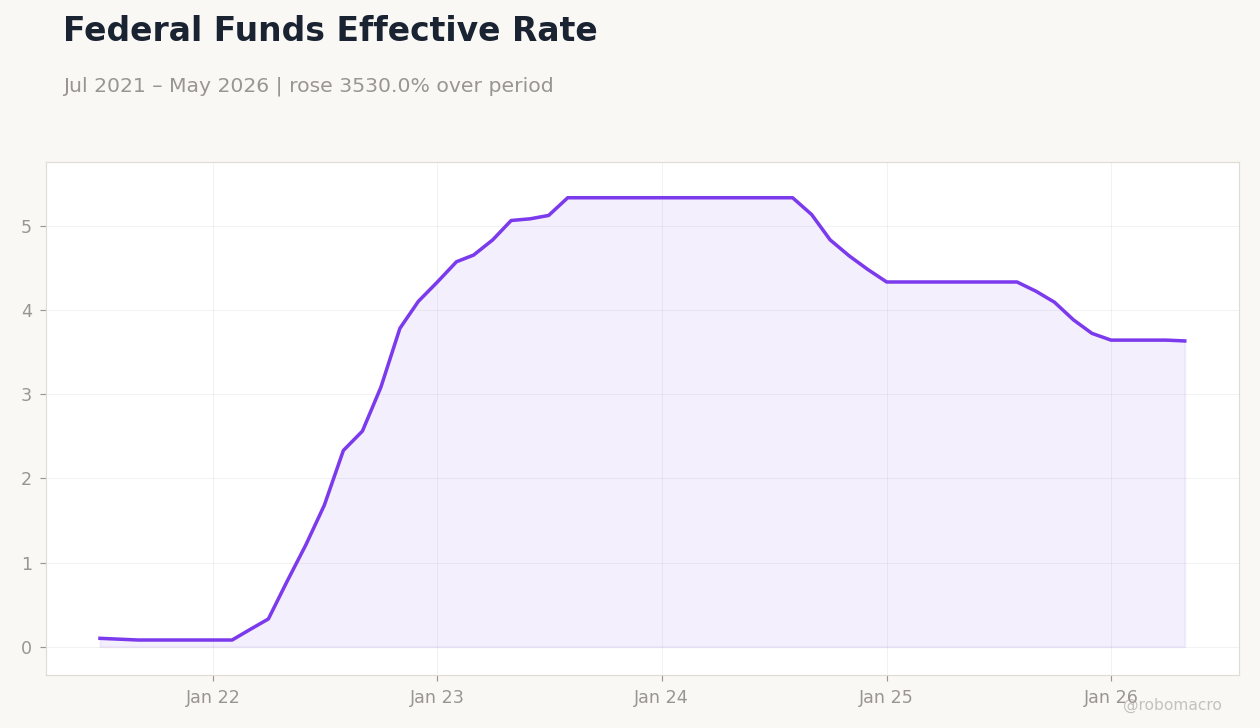

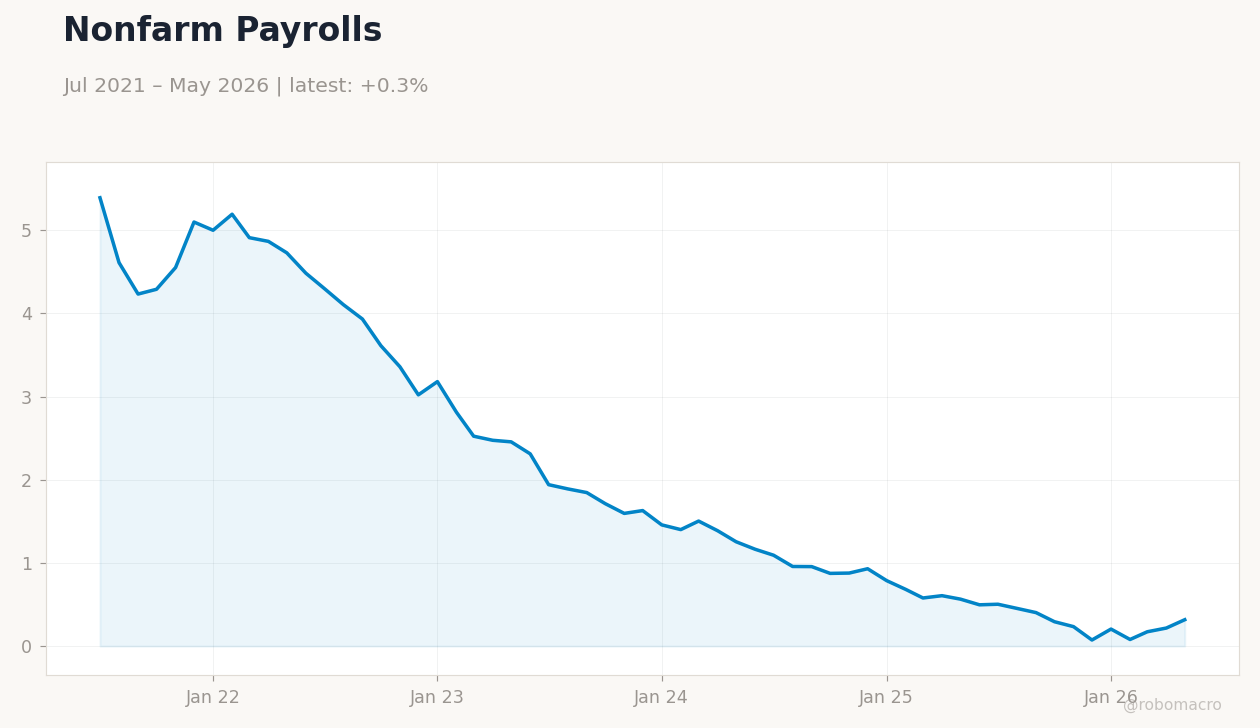

Broader indicators point to a gradual cooling. US CPI YoY stands at 2.31% while unemployment holds at 4.30%. The Fed Funds Rate remains at 3.62%.

Housing and manufacturing softness may reinforce expectations for steady policy through the summer. Equity breadth remains constructive despite the mixed data flow.

Global Macro News

Global developments continue to influence US asset prices. The new US-Iran framework has eased energy supply concerns, driving the sharp decline in WTI. European equity markets rose on the back of the same geopolitical relief.

<i>↓ p.2</i>