US Macro Daily(Beta Mode)

Retail Sales Beat as Fed Holds Rates

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,420.10 | -1.21% |

| Nasdaq 100 | 29,670.95 | -0.99% |

| Dow Jones | 51,492.55 | -0.98% |

| Russell 2000 | 2,917.98 | -0.72% |

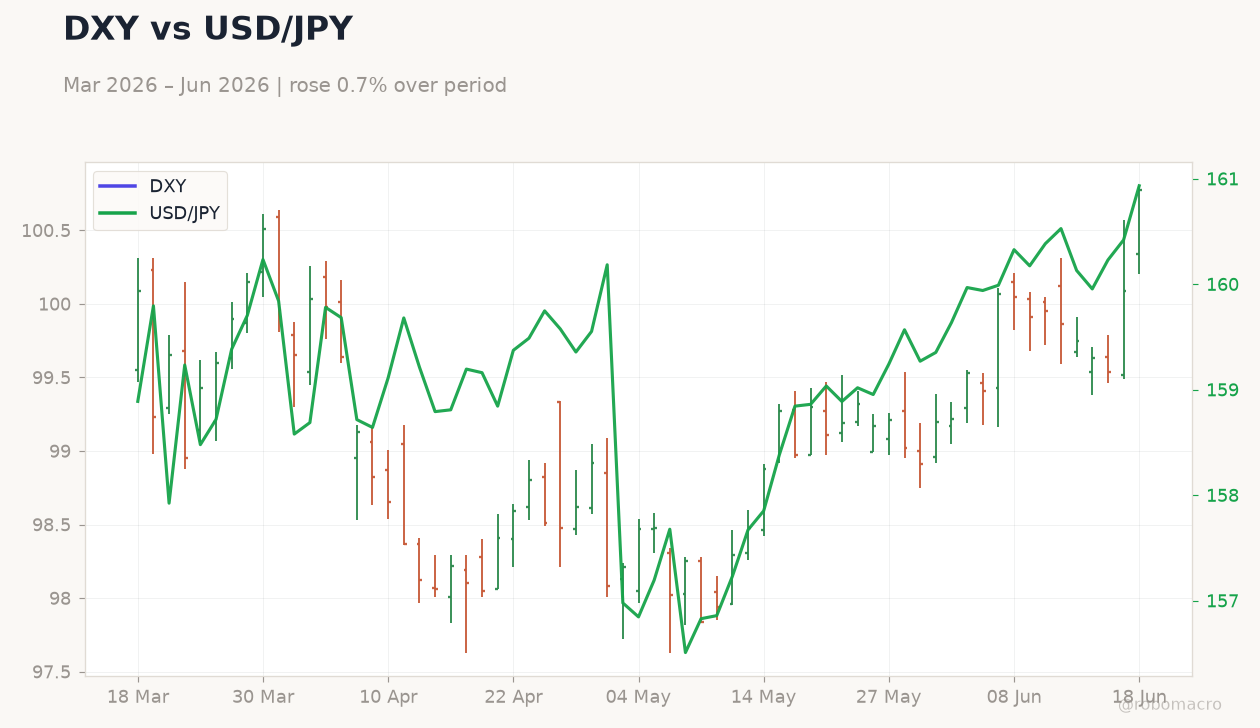

| USD/JPY | 160.94 | +0.32% |

| EUR/USD | 1.15 | -1.28% |

| GBP/USD | 1.32 | -1.60% |

| Gold | 4,260.30 | -2.26% |

| WTI Crude | 74.59 | -2.86% |

| Bitcoin | 63,927.04 | -2.55% |

| US 2Y Treasury | 4.05% | -0.49% |

| US 10Y Treasury | 4.43% | -0.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NY Empire State Manufacturing Index | 19.60 | 14 | 5.70 |

| Industrial Production Month-over-Month | 0.90 | 0.30 | 0.10 |

| NAHB Housing Market Index | 37 | 36 | 35 |

| ADP Employment Change Weekly | 29,000 | - | 25,500 |

| Building Permits Prel | 1.4m | 1.4m | 1.4m |

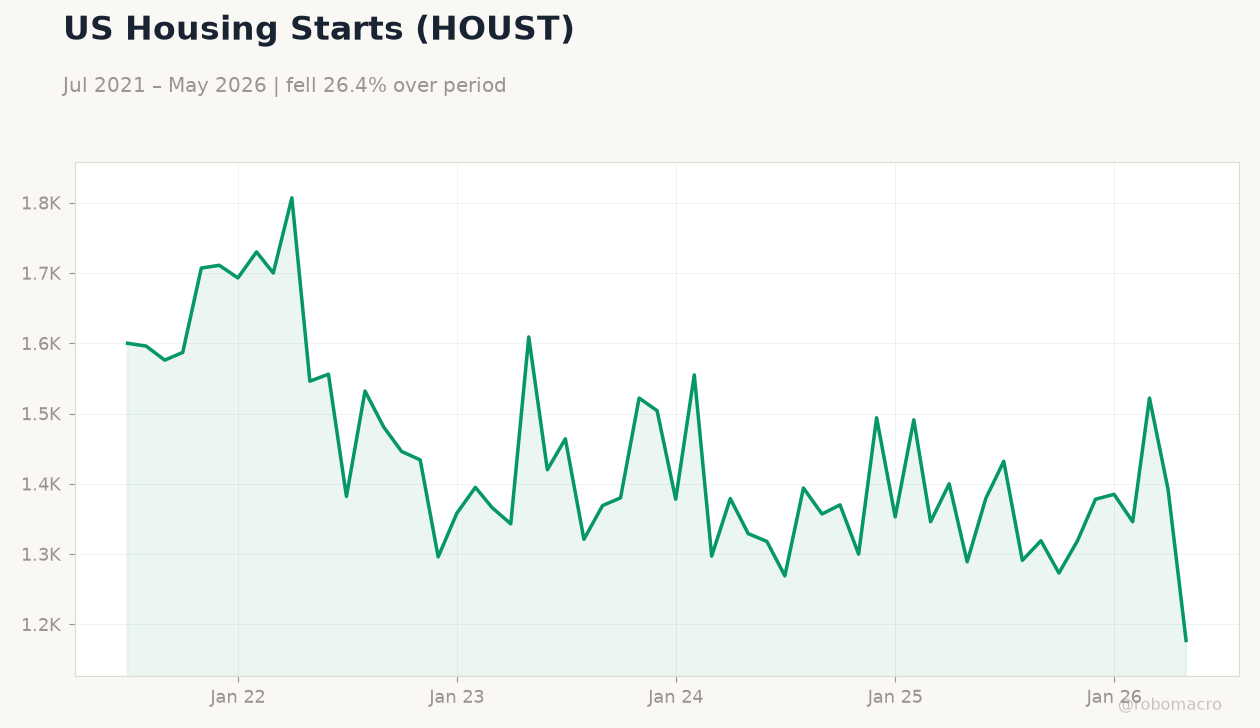

| Housing Starts Level | 1.4m | 1.4m | 1.2m |

| Building Permits Month-over-Month Prel | 4.40 | - | -0.70 |

| Export Prices Month-over-Month | 3.50 | 1.20 | 1.30 |

| Housing Starts Month-over-Month | -8.50 | - | -15.40 |

| Import Prices Month-over-Month | 2 | 1 | 1.90 |

US 10-Year Treasury Yield | Type: macro_line | Percent: 4.43 (2026-06-16) | Range: 1.19–4.98 | Trend(6pt): 1.5,3.45,3.92,4.31,4.48,4.43

US 10-Year Treasury Yield | Type: macro_line | Percent: 4.43 (2026-06-16) | Range: 1.19–4.98 | Trend(6pt): 1.5,3.45,3.92,4.31,4.48,4.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Philadelphia Fed Manufacturing Index | -0.40 | 10 | 04:30 |

| Weekly Jobless Claims | 229,000 | 225,000 | 04:30 |

| Net Long-term TIC Flows | 81,300m | 75,000m | 12:00 |

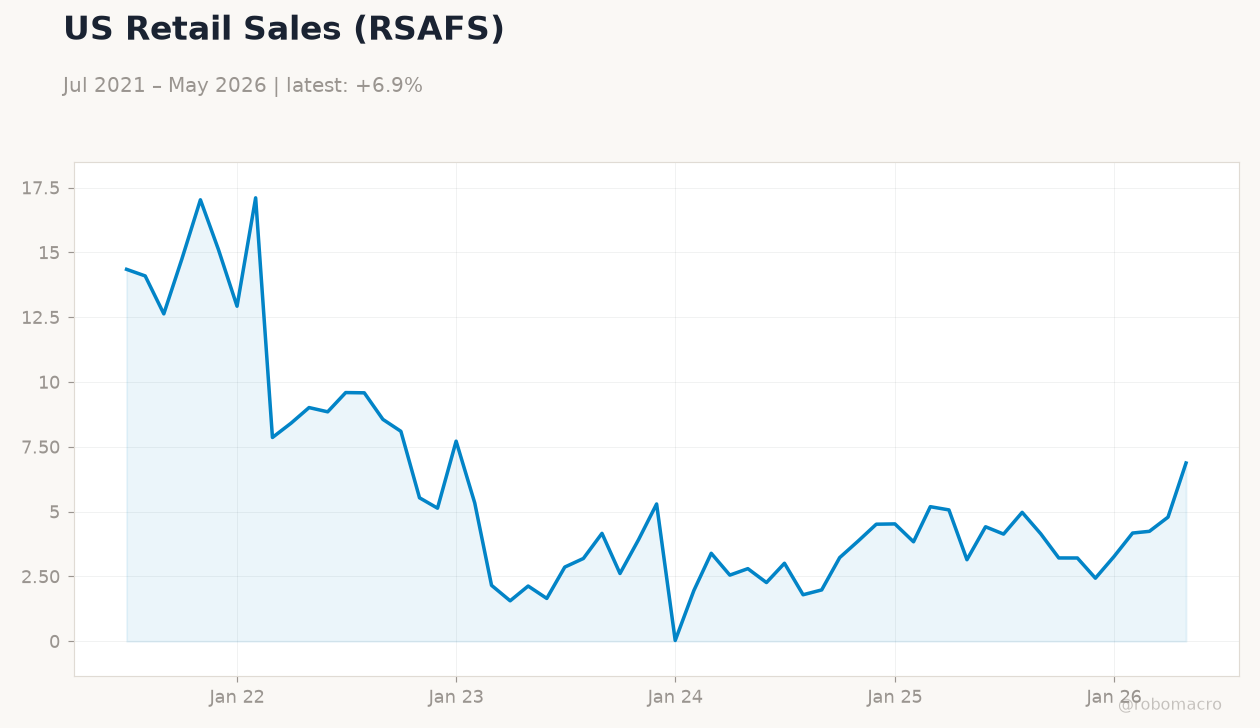

- US retail sales rose 0.9% m/m in May, beating the 0.5% consensus and signaling resilient consumer demand.

- Housing starts plunged 15.4% m/m to 1.177 million, far below expectations, highlighting sector weakness.

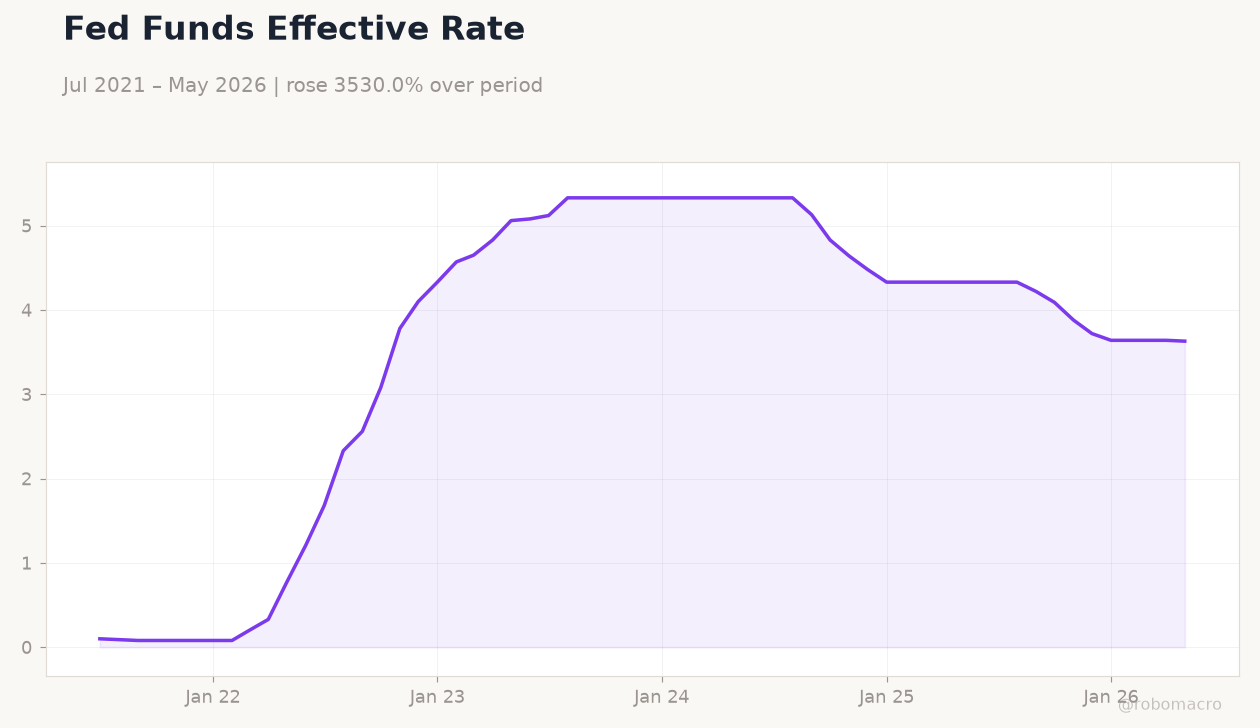

- Equities fell nearly 1% as the Fed held rates at 3.63% and raised 2026 inflation projections.

Yesterday's Recap

Retail sales control group advanced 0.7% m/m while ex-autos sales gained 0.8%, both exceeding forecasts and reinforcing consumer strength. Housing starts collapsed to 1.177 million and building permits slipped to 1.413 million, confirming sharp contraction in residential activity. Industrial production rose just 0.1% m/m and the Empire State manufacturing index dropped to 5.7, pointing to softening factory momentum.

Equities closed lower with the S&P 500 down 1.21% at 7,420.10 and the Nasdaq 100 off 0.99%. The dollar strengthened, lifting USD/JPY to 160.94 while EUR/USD fell to 1.15. Treasury yields declined modestly, with the 10-year at 4.43% and the 2-year at 4.05%.

Gold dropped 2.26% to 4,260.30 amid the firmer dollar.

The Day Ahead

The Philadelphia Fed Manufacturing Index is due at 8:30 a.m. ET. Markets will also digest the June FOMC projections released after the June 16-17 meeting.

Focus will remain on incoming inflation prints and labor-market updates to gauge the path of policy. Treasury auctions and any follow-up comments from regional Fed presidents could influence rate expectations. Oil prices may react to global supply developments following the US-Iran developments.

Other Economic Notes

The unemployment rate stands at 4.30%, providing the Fed with room to assess labor-market cooling without immediate alarm. CPI inflation at 2.31% year-over-year remains above the 2% target, supporting the committee’s cautious stance. Stronger retail data reduces the urgency for near-term easing while persistent housing weakness may eventually weigh on growth.

Market pricing continues to reflect limited cuts for 2026 despite the retail beat.

Global Macro News

A major European pension fund reduced US exposure citing technology concentration risks, potentially pressuring equity inflows. Oil prices fell below $80 after a US-Iran peace deal eased supply concerns and allowed Iranian tankers to exit the Hormuz area. <i>↓ p.2</i>