US Macro Daily(Beta Mode)

Warsh Holds Rates as Housing Starts Slump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,481.86 | +0.83% |

| Nasdaq 100 | 30,242.74 | +1.93% |

| Dow Jones | 51,642.53 | +0.29% |

| Russell 2000 | 2,959.35 | +1.42% |

| USD/JPY | 161.28 | +0.42% |

| EUR/USD | 1.15 | -0.35% |

| GBP/USD | 1.32 | -0.48% |

| Gold | 4,170.80 | -1.26% |

| WTI Crude | 75.87 | -0.95% |

| Bitcoin | 62,444.09 | -0.72% |

| US 2Y Treasury | 4.20% | +3.70% |

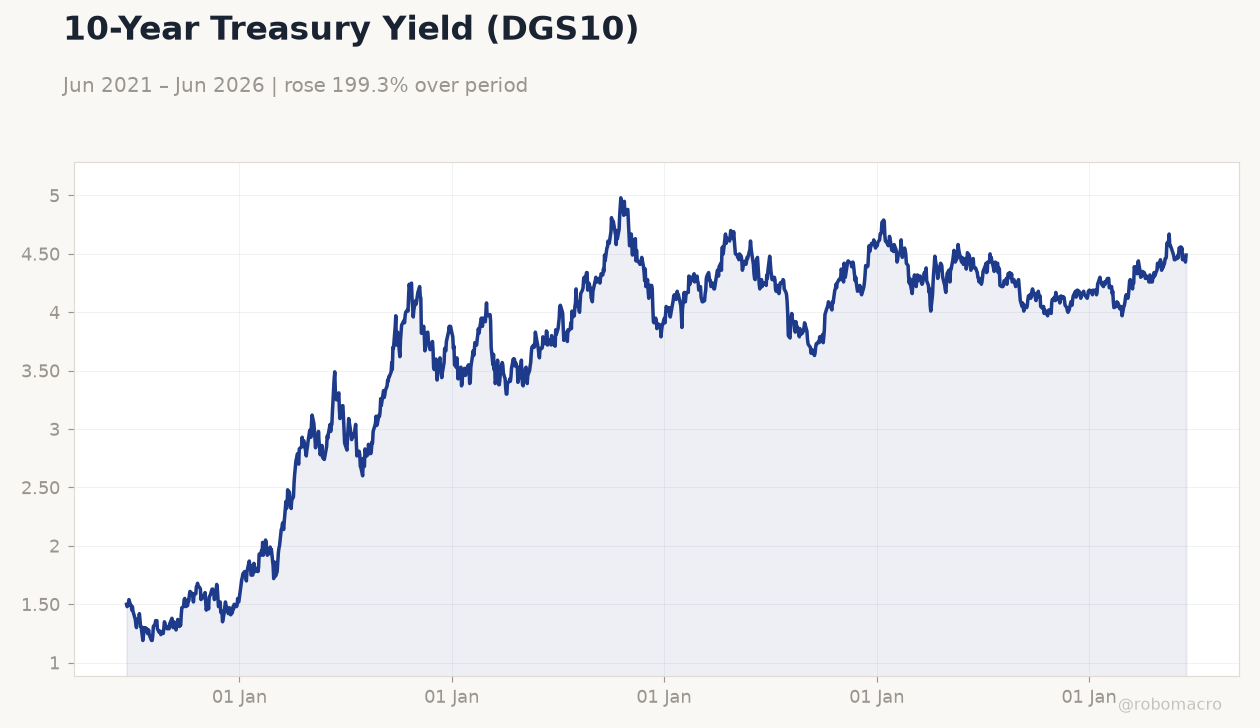

| US 10Y Treasury | 4.49% | +1.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NY Empire State Manufacturing Index | 19.60 | 14 | 5.70 |

| Industrial Production Month-over-Month | 0.90 | 0.30 | 0.10 |

| NAHB Housing Market Index | 37 | 36 | 35 |

| ADP Employment Change Weekly | 29,000 | - | 25,500 |

| Building Permits Prel | 1.4m | 1.4m | 1.4m |

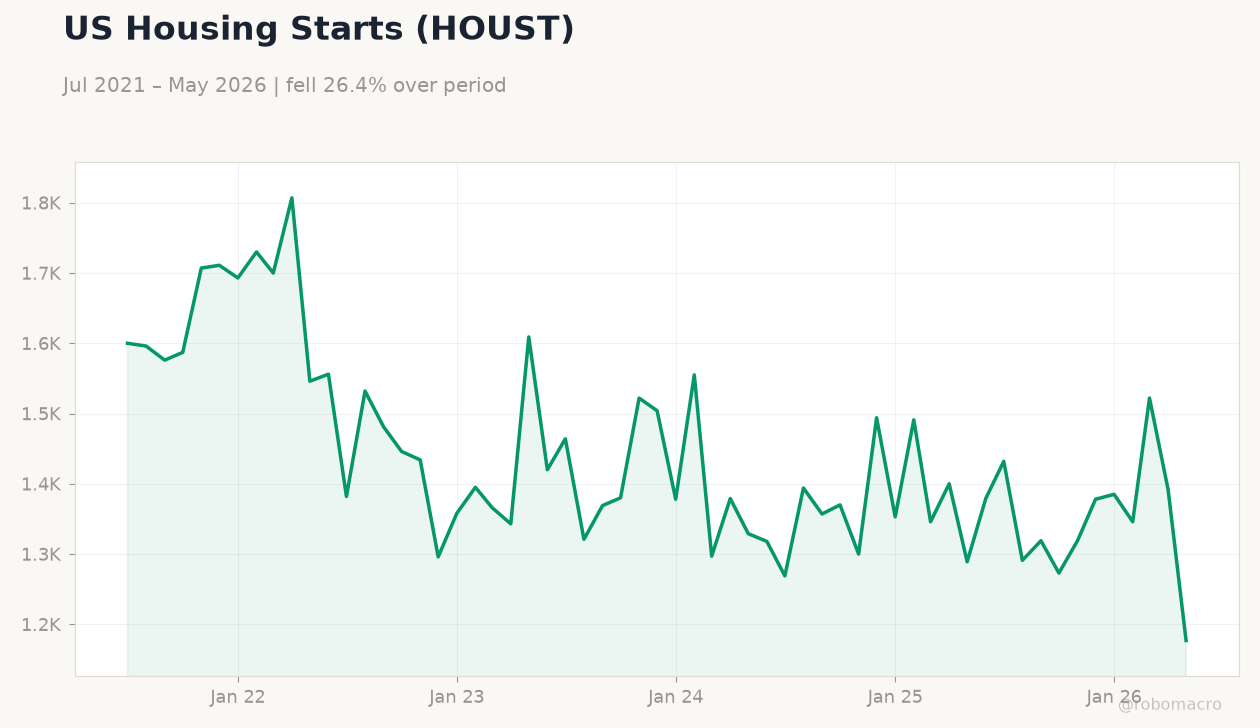

| Housing Starts Level | 1.4m | 1.4m | 1.2m |

| Building Permits Month-over-Month Prel | 4.40 | - | -0.70 |

| Export Prices Month-over-Month | 3.50 | 1.20 | 1.30 |

| Housing Starts Month-over-Month | -8.50 | - | -15.40 |

| Import Prices Month-over-Month | 2 | 1 | 1.90 |

10-Year Treasury Yield (DGS10) | Type: macro_line | Percent: 4.49 (2026-06-17) | Range: 1.19–4.98 | Trend(5pt): 1.5,3.49,3.95,4.24,4.49

10-Year Treasury Yield (DGS10) | Type: macro_line | Percent: 4.49 (2026-06-17) | Range: 1.19–4.98 | Trend(5pt): 1.5,3.49,3.95,4.24,4.49

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- US housing starts plunged 15.4% to 1.177 million in May, well below the 1.43 million consensus, while building permits fell 0.7%.

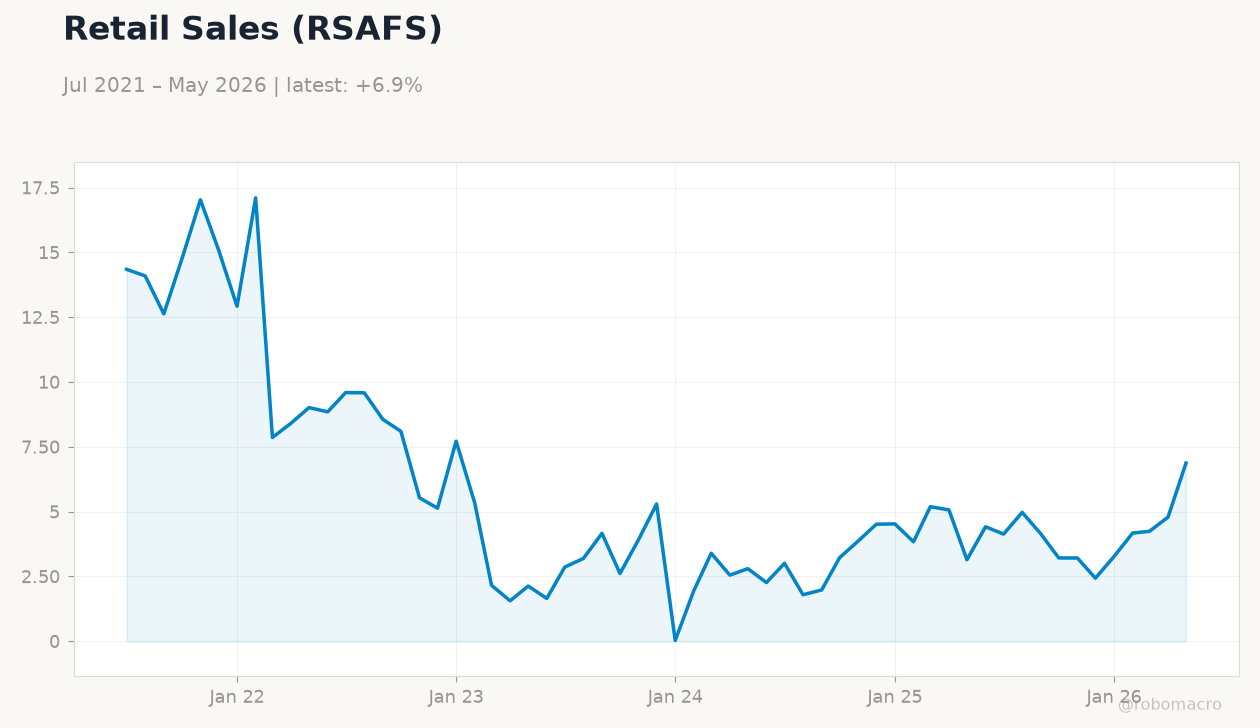

- Retail sales rose 0.9% month-over-month, beating the 0.5% forecast and signaling resilient consumer spending outside autos.

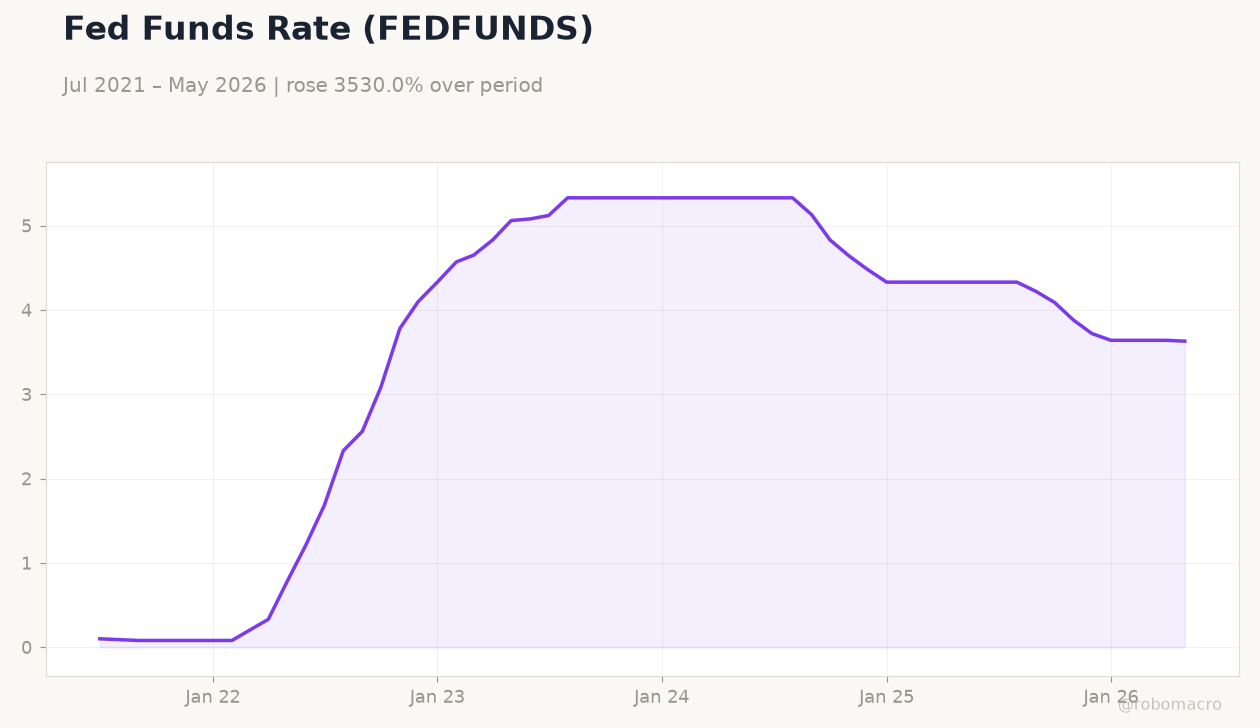

- New Fed Chair Kevin Warsh kept the policy rate at 3.63% and adopted a hawkish tone, lifting near-term rate expectations.

Yesterday's Recap

US data delivered a clear split between weak housing and firm consumption. Housing starts collapsed 15.4% month-over-month to 1.177 million, the largest miss in months, while building permits slipped to 1.413 million. Industrial production rose just 0.1%, below the 0.3% consensus, and the NY Empire State Manufacturing Index dropped to 5.7 from 19.6.

Retail sales, however, printed 0.9% month-over-month versus 0.5% expected, with the control group also beating at 0.7%. Equity markets rallied, with the S&P 500 gaining 0.83% to 7,481.86 and the Nasdaq 100 surging 1.93%. Treasury yields rose across the curve, the 2-year climbing to 4.20% and the 10-year to 4.49%, while gold fell 1.26% to $4,170.80.

The Day Ahead

Markets will focus on weekly jobless claims and regional manufacturing surveys for fresh labor and growth signals. Housing-market data weakness may keep pressure on rate-sensitive sectors. USD/JPY near 161.28 and EUR/USD at 1.15 suggest continued dollar strength after the hawkish Fed shift.

Oil prices at $75.87 remain sensitive to any OPEC+ supply signals. Equity positioning favors tech after the Nasdaq outperformance, while short-end yields could stay elevated if inflation concerns linger.

Other Economic Notes

The economy shows a pronounced two-speed pattern, with AI-driven investment outpacing consumption. Unemployment at 4.3% and CPI at 2.31% year-over-year leave the Fed with limited room to ease. Retail resilience supports the view that policy remains restrictive but not yet damaging to spending.

Treasury market volatility has increased as investors reprice the path of rates under the new leadership.

Global Macro News

European shares retreated after the hawkish US Fed signal, with investors reassessing rate differentials. A major UK pension fund reduced US exposure citing tech concentration risks. The ECB left rates unchanged while lowering its 2026 growth forecast.

Oil prices eased on expectations of higher OPEC+ output. <i>↓ p.2</i>