US Macro Daily(Beta Mode)

Waller Speech Looms as Equities Advance

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,481.86 | +0.83% |

| Nasdaq 100 | 30,242.74 | +1.93% |

| Dow Jones | 51,642.53 | +0.29% |

| Russell 2000 | 2,959.35 | +1.42% |

| USD/JPY | 161.73 | +0.28% |

| EUR/USD | 1.15 | -0.01% |

| GBP/USD | 1.32 | +0.26% |

| Gold | 4,223.60 | -0.01% |

| WTI Crude | 75.32 | -1.67% |

| Bitcoin | 64,039.67 | +1.27% |

| US 2Y Treasury | 4.20% | +3.70% |

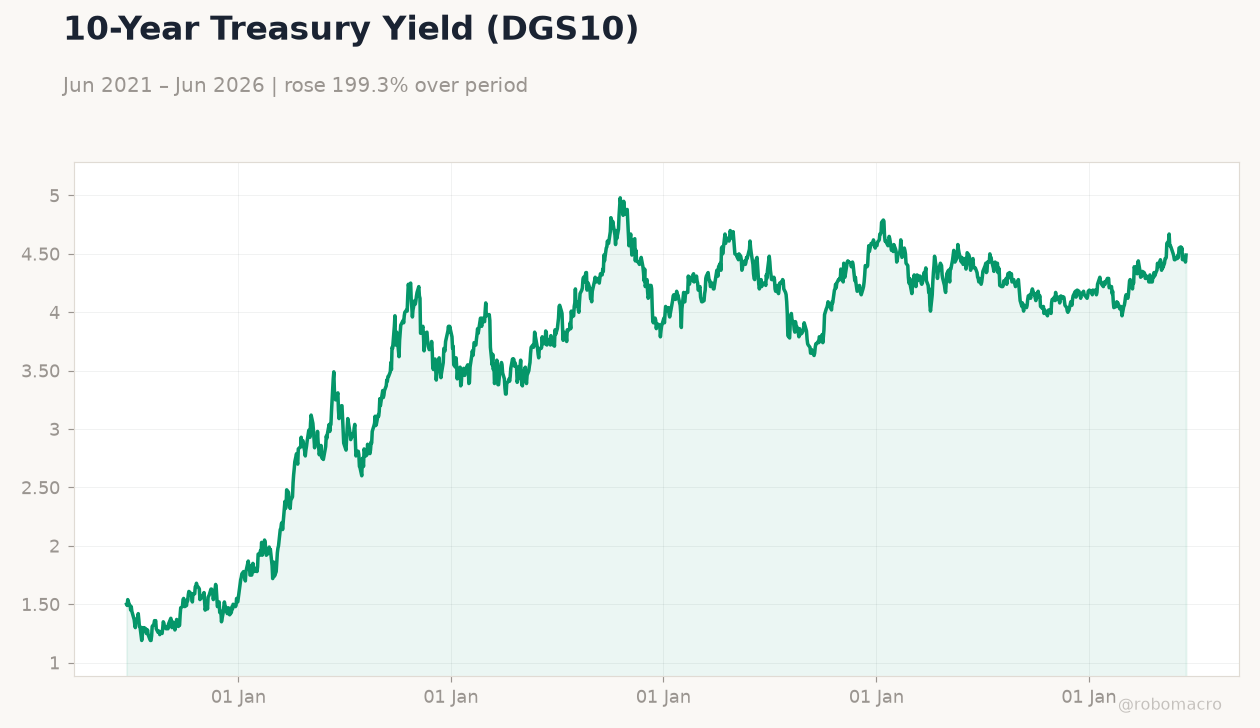

| US 10Y Treasury | 4.49% | +1.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

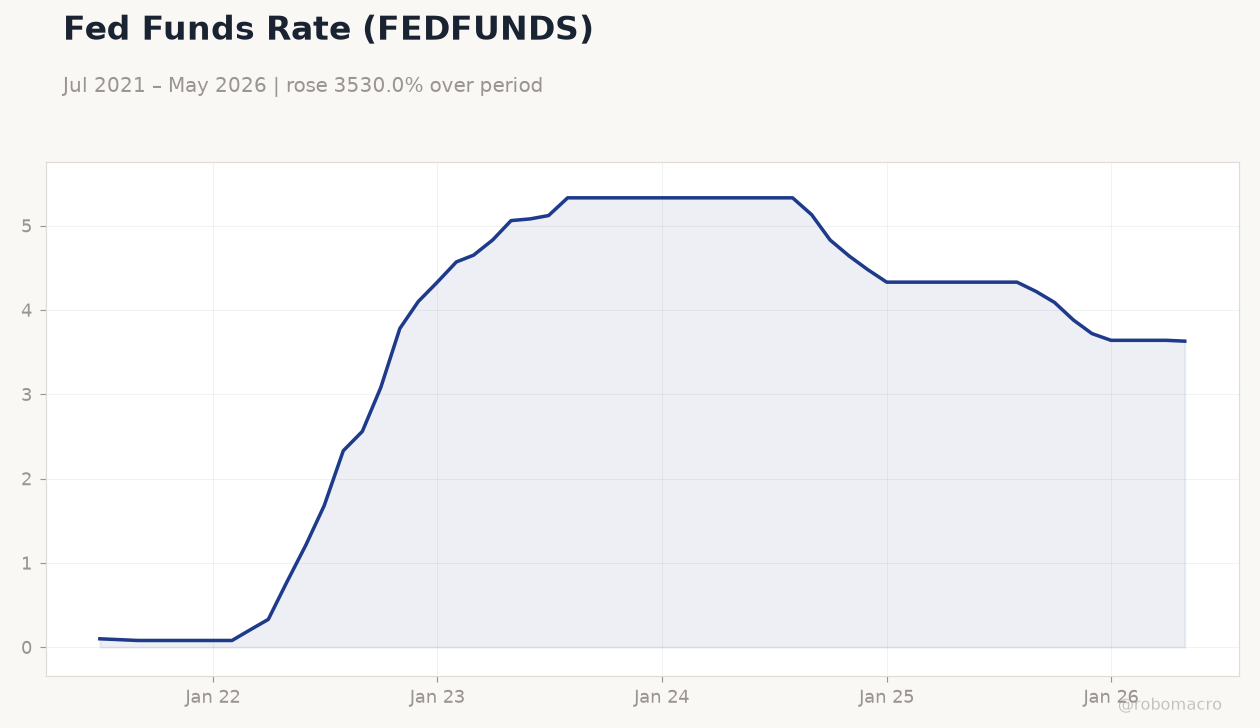

Fed Funds Rate (FEDFUNDS) | Type: macro_line | Percent: 3.63 (2026-05-01) | Range: 0.08–5.33 | Trend(6pt): 0.1,2.56,5.33,4.33,3.64,3.63

Fed Funds Rate (FEDFUNDS) | Type: macro_line | Percent: 3.63 (2026-05-01) | Range: 0.08–5.33 | Trend(6pt): 0.1,2.56,5.33,4.33,3.64,3.63

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Speech by Fed's Waller | - | - | 05:00 |

| Tuesday (2026-06-23) | |||

| ADP Employment Change Weekly | 25,500 | - | 04:15 |

| S&P Global Composite PMI Flash | 51.50 | - | 05:45 |

| S&P Global Manufacturing PMI Flash | 55.10 | 54.80 | 05:45 |

| S&P Global Services PMI Flash | 50.70 | 51 | 05:45 |

| API Weekly Crude Oil Stocks | -8.3m | - | 12:30 |

| Wednesday (2026-06-24) | |||

| MBA 30-Year Mortgage Rate | 6.60 | - | 03:00 |

| Current Account Balance | -190,700m | -225,000m | 04:30 |

- S&P 500 rose 0.83% to 7,481.86 while Nasdaq 100 gained 1.93% on tech strength

- US 2-year yield climbed 3.7 bp to 4.20% and 10-year rose 1.35 bp to 4.49%

- Fed's Waller delivers remarks today ahead of tomorrow's PMI releases

Yesterday's Recap

US equity markets posted solid gains on June 21 with the S&P 500 advancing 0.83% to close at 7,481.86 and the Nasdaq 100 surging 1.93% to 30,242.74. The Dow Jones added 0.29% while the Russell 2000 climbed 1.42%. Treasury yields moved higher across the curve, with the 2-year note reaching 4.20% and the 10-year settling at 4.49%.

WTI crude fell 1.67% to 75.32 amid inventory data, and the dollar firmed modestly against the yen at 161.73. Gold held steady near 4,223.60 while Bitcoin rose 1.27% to 64,039.67. No major data releases occurred yesterday, leaving market focus on the upcoming Fed address.

The Day Ahead

Fed Governor Waller speaks at 5:00 a.m. ET today on monetary policy topics. Tomorrow brings ADP employment figures, S&P Global flash PMIs for manufacturing and services, and API crude stock data.

Wednesday features new home sales, the current account balance, and Federal Reserve bank stress test results. Markets will parse the PMI prints for signs of growth momentum ahead of the stress test release. No additional Fed speakers are scheduled through midweek.

Other Economic Notes

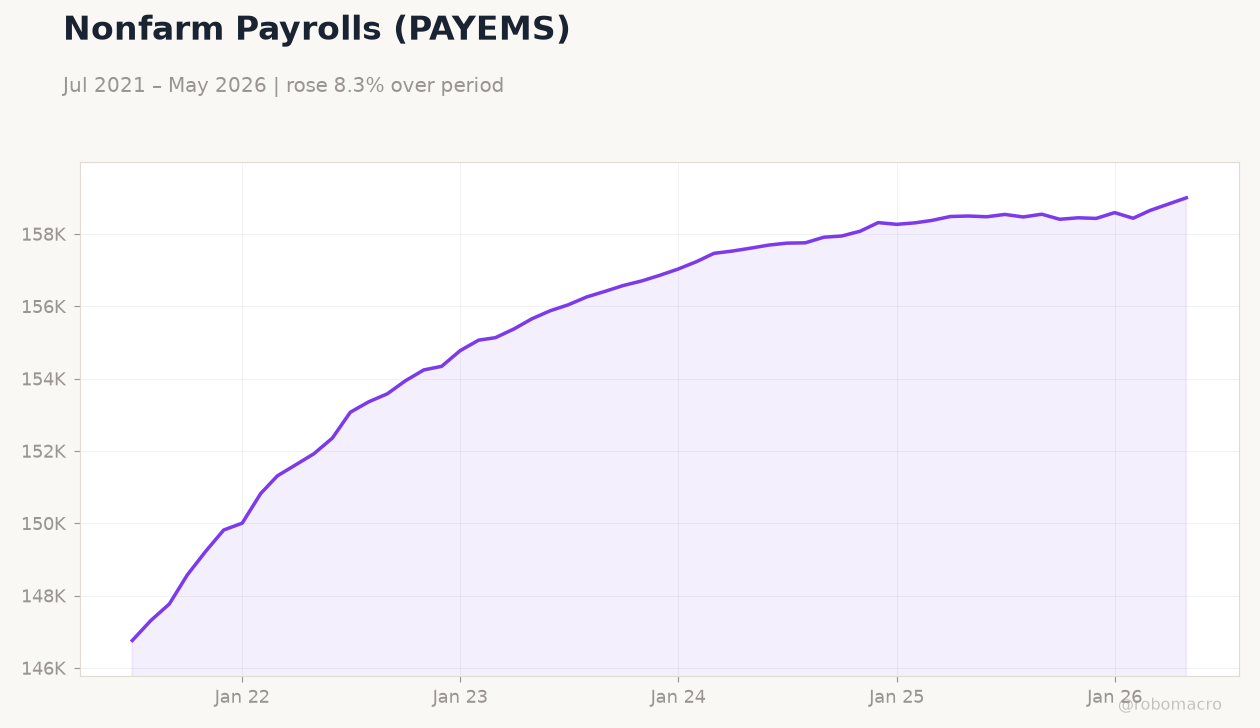

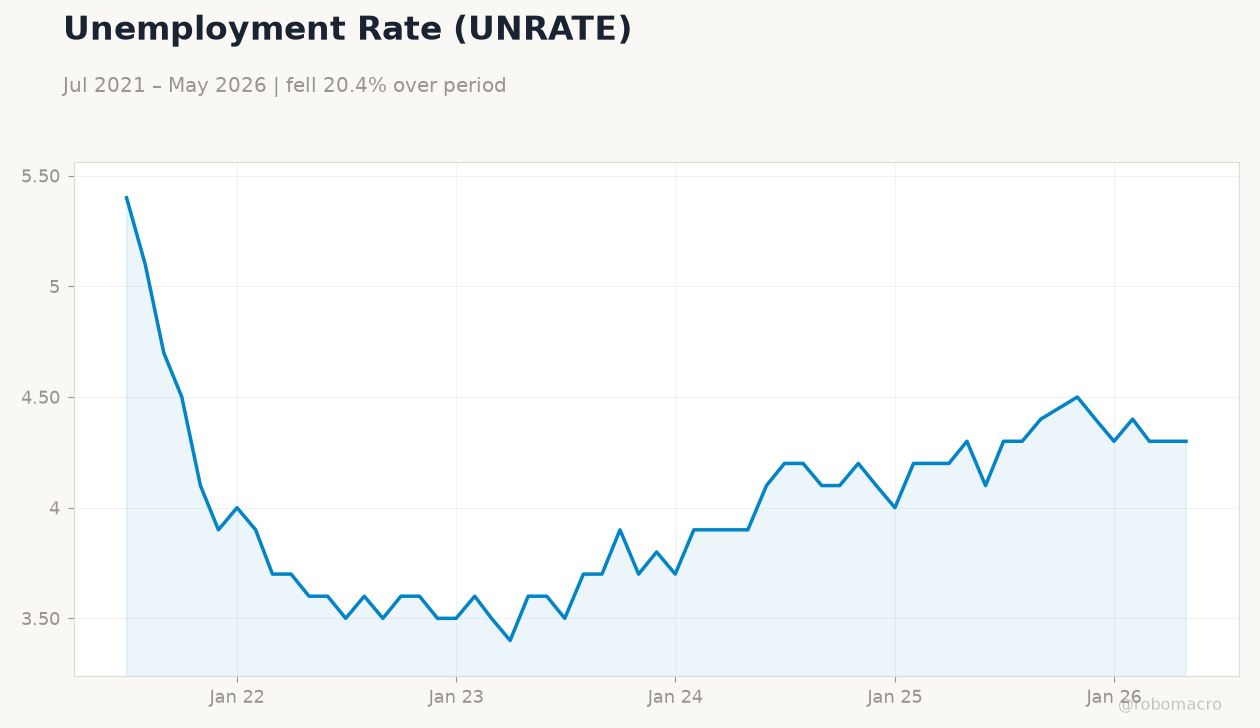

The Fed funds rate sits at 3.63% while headline CPI inflation registers 2.31% year-over-year. Unemployment remains at 4.30%, consistent with a labor market that has cooled gradually without sharp deterioration. Equity and rate markets continue to price a soft-landing path with limited volatility.

Treasury curves reflect measured expectations for policy stability through the summer.

Global Macro News

South African rates received support following a US-brokered peace agreement that eased regional risk premia. Canada faces calls for Bank of Canada easing to support growth amid slowing domestic indicators. The ECB held rates steady while trimming its 2026 growth forecast, adding to external demand uncertainty for US exports.

China’s PMI edged higher but remained below the expansion threshold, signaling persistent manufacturing weakness. Australia’s central bank confronts a trade-off between inflation control and recession risks.