US Macro Daily(Beta Mode)

Equities Rise as U.S. Eases Iran Oil Sanctions

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,481.86 | +0.83% |

| Nasdaq 100 | 30,242.74 | +1.93% |

| Dow Jones | 51,642.53 | +0.29% |

| Russell 2000 | 2,959.35 | +1.42% |

| USD/JPY | 161.45 | +0.01% |

| EUR/USD | 1.14 | -0.50% |

| GBP/USD | 1.32 | +0.10% |

| Gold | 4,140.30 | -0.99% |

| WTI Crude | 73.78 | -1.39% |

| Bitcoin | 62,290.00 | -2.60% |

| US 2Y Treasury | 4.19% | -0.24% |

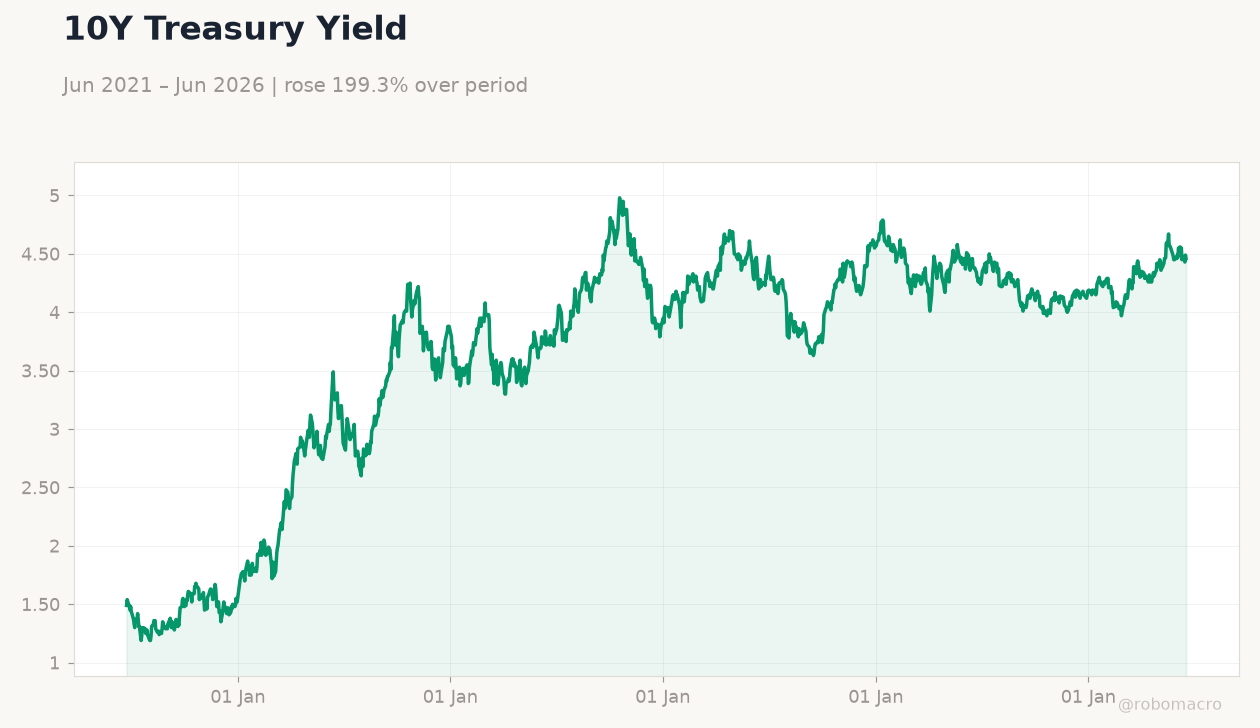

| US 10Y Treasury | 4.46% | -0.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Waller | - | - | - |

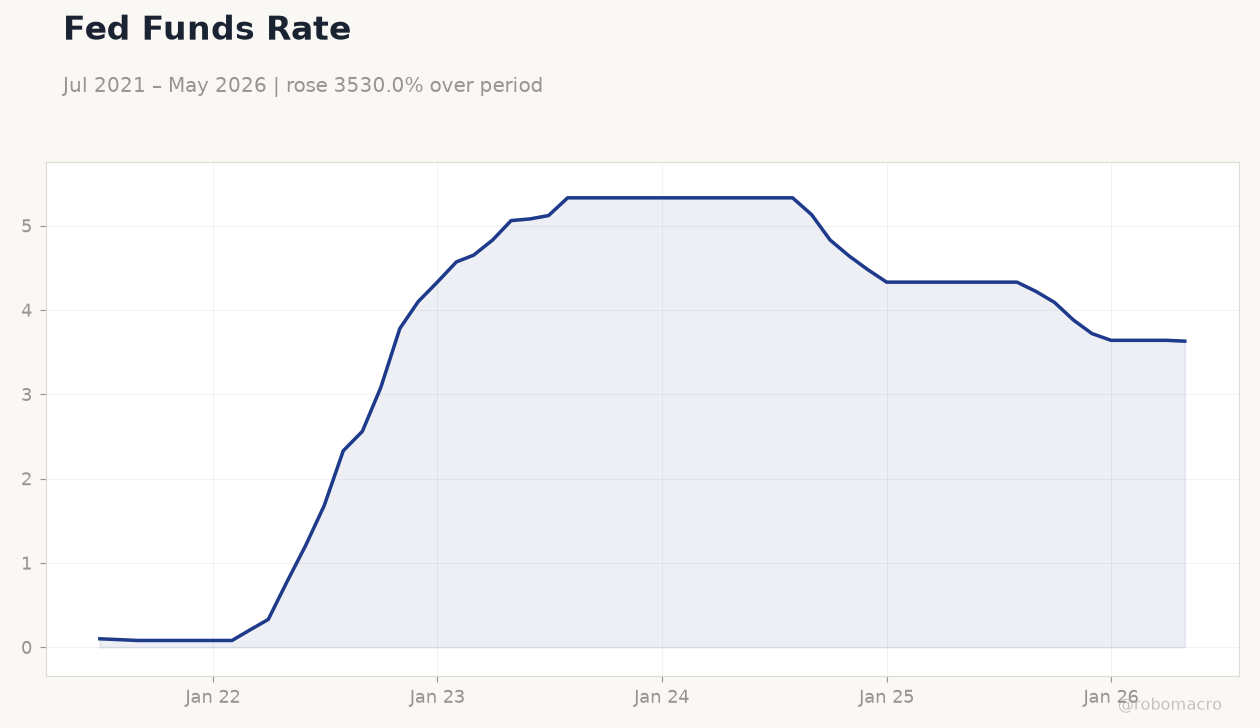

Fed Funds Rate | Type: macro_line | %: 3.63 (2026-05-01) | Range: 0.08–5.33 | Trend(6pt): 0.1,2.56,5.33,4.33,3.64,3.63

Fed Funds Rate | Type: macro_line | %: 3.63 (2026-05-01) | Range: 0.08–5.33 | Trend(6pt): 0.1,2.56,5.33,4.33,3.64,3.63

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change Weekly | 25,500 | - | 04:15 |

| S&P Global Composite PMI Flash | 51.50 | - | 05:45 |

| S&P Global Manufacturing PMI Flash | 55.10 | 54.80 | 05:45 |

| S&P Global Services PMI Flash | 50.70 | 51 | 05:45 |

| API Weekly Crude Oil Stocks | -8.3m | - | 12:30 |

- S&P 500 rose 0.83% and Nasdaq 100 gained 1.93% as US eased Iran oil sanctions, sending WTI crude down 1.39% to $73.78.

- US 10-year Treasury yield fell 0.67% to 4.46% while 2-year yield declined 0.24% to 4.19%, reflecting lower growth and inflation expectations.

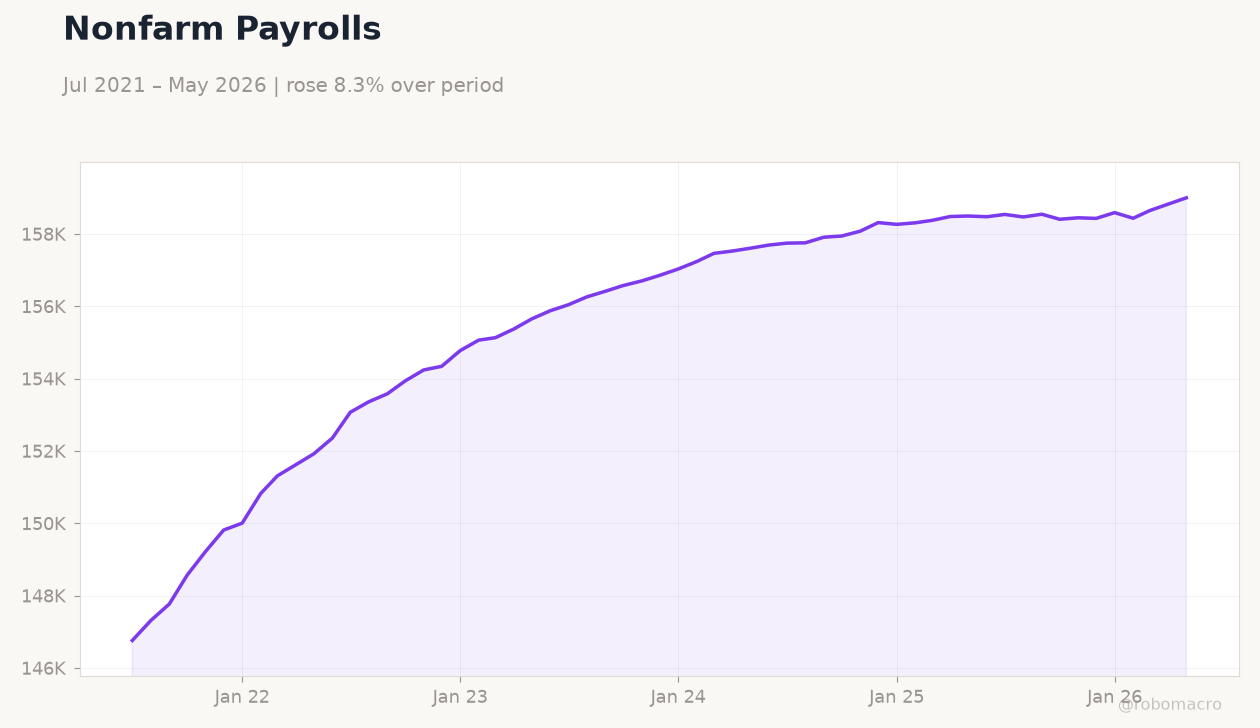

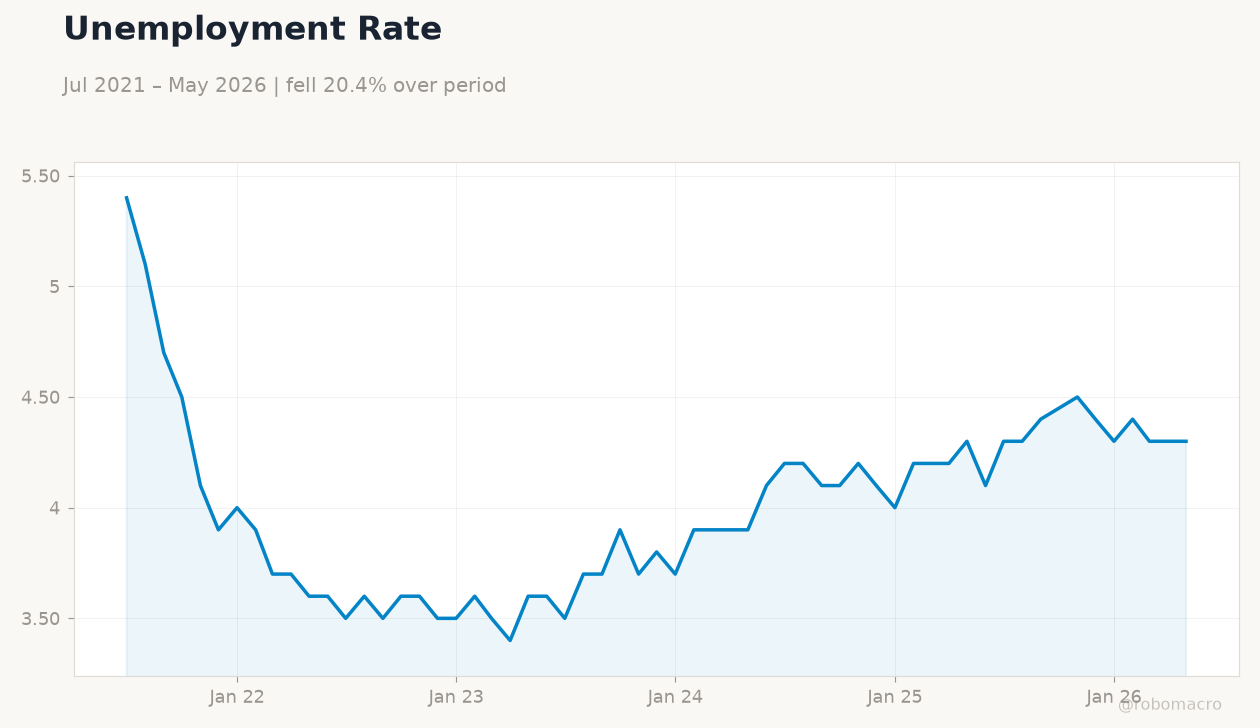

- ADP employment data and S&P Global flash PMIs headline today’s releases, with Fed funds rate steady at 3.63% and unemployment at 4.30%.

Yesterday's Recap

US equity indices posted solid gains on June 22 as news of temporary US sanctions relief on Iranian oil exports lifted sentiment and pressured energy prices lower. The S&P 500 closed at 7,481.86 while the Nasdaq 100 surged to 30,242.74, outperforming the Dow Jones which rose only 0.29%. Treasury yields declined across the curve, with the 10-year note falling to 4.46%, as investors priced reduced supply risks and softer inflation pressures.

Fed Governor Waller delivered remarks that offered no new policy signals, leaving markets focused on the upcoming PMI prints. Gold slipped 0.99% to $4,140.30 and Bitcoin fell 2.60% amid broad risk-on flows. The death of former Fed Chair Alan Greenspan at age 100 prompted retrospective commentary on past monetary regimes but had limited immediate market impact.

The Day Ahead

Markets will focus on the 5:45 a.m. ET release of S&P Global flash PMIs, with manufacturing expected at 54.8 and services at 51.0. ADP weekly employment change at 4:15 a.m.

will provide an early labor-market read ahead of Friday’s official data. API crude inventories at 12:30 p.m. and tomorrow’s EIA figures will keep energy traders engaged.

New home sales and the current account balance due Wednesday offer additional housing and external-balance context. Fed Bank Stress Test results at noon tomorrow could influence bank-sector positioning.

Other Economic Notes

With CPI at 2.31% and unemployment at 4.30%, the data backdrop remains consistent with a soft-landing scenario. Treasury yield compression suggests markets anticipate the Fed will maintain the 3.63% policy rate for longer. Equity breadth improved as small-caps outperformed, with the Russell 2000 rising 1.42%.

Oil-price relief from Iran sanctions should support consumer spending and corporate margins in coming months.