US Macro Daily(Beta Mode)

PMIs Surge, Equities Advance as Yields Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,481.86 | +0.83% |

| Nasdaq 100 | 30,242.74 | +1.93% |

| Dow Jones | 51,642.53 | +0.29% |

| Russell 2000 | 2,959.35 | +1.42% |

| USD/JPY | 161.68 | +0.07% |

| EUR/USD | 1.13 | -0.74% |

| GBP/USD | 1.32 | -0.67% |

| Gold | 4,077.50 | -1.27% |

| WTI Crude | 71.78 | -1.95% |

| Bitcoin | 62,370.00 | -0.48% |

| US 2Y Treasury | 4.24% | +1.19% |

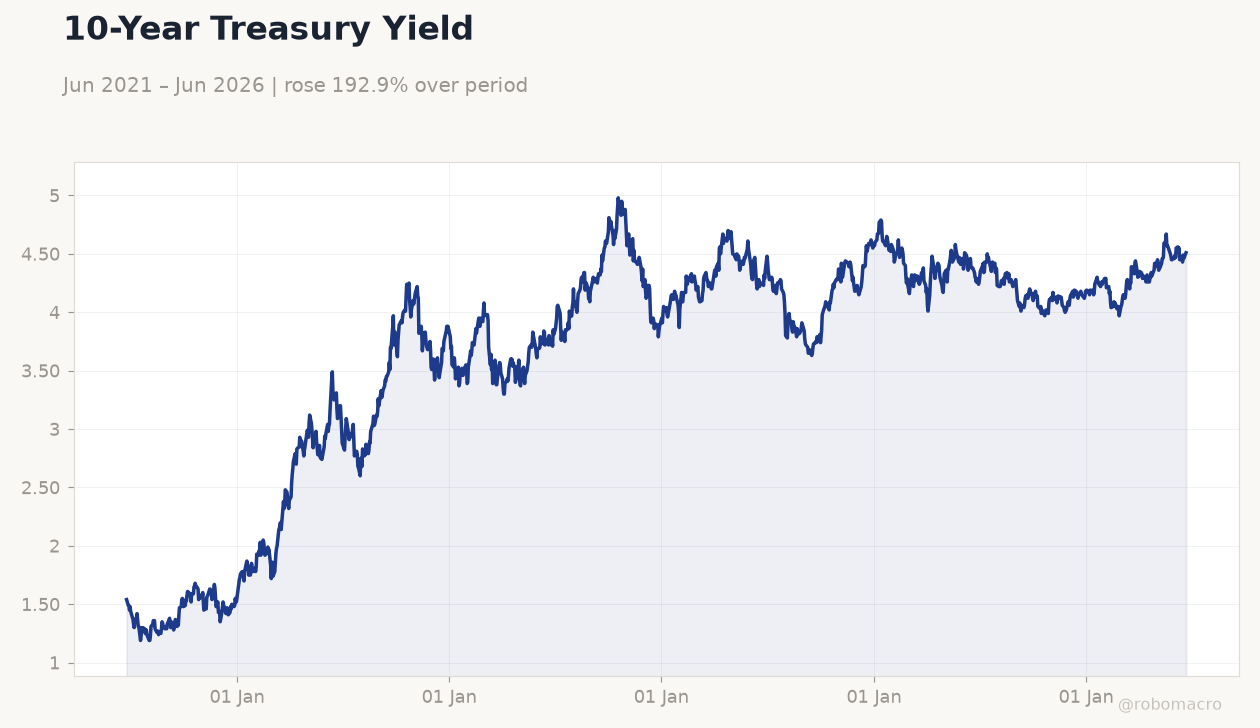

| US 10Y Treasury | 4.51% | +1.12% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Waller | - | - | - |

| ADP Employment Change Weekly | 26,500 | - | 30,750 |

| S&P Global Composite PMI Flash | 51.50 | - | 52.20 |

| S&P Global Manufacturing PMI Flash | 55.10 | 54.80 | 55.70 |

| S&P Global Services PMI Flash | 50.70 | 51 | 51.30 |

| MBA 30-Year Mortgage Rate | 6.60 | - | - |

10-Year Treasury Yield | Type: macro_line | Percent: 4.51 (2026-06-22) | Range: 1.19–4.98 | Trend(6pt): 1.54,3.7,3.86,4.25,4.46,4.51

10-Year Treasury Yield | Type: macro_line | Percent: 4.51 (2026-06-22) | Range: 1.19–4.98 | Trend(6pt): 1.54,3.7,3.86,4.25,4.46,4.51

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Balance | -190,700m | -217,500m | 04:30 |

| New Home Sales | 622,000 | 640,000 | 06:00 |

| New Home Sales Month-over-Month | -6.20 | - | 06:00 |

| EIA Weekly Crude Oil Inventory | -8.3m | -3.9m | 06:30 |

| EIA Weekly Gasoline Inventory | -906,000 | - | 06:30 |

| Fed Bank Stress Test Results | - | - | 12:00 |

- S&P Global Composite PMI rose to 52.2 from 51.5, with manufacturing at 55.7 versus consensus 54.8.

- Equities gained, led by Nasdaq 100 up 1.93% to 30,242.74 while 10Y yields climbed to 4.51%.

- ADP employment change printed 30,750, above the prior 26,500, signaling labor resilience.

Yesterday's Recap

US data releases showed stronger-than-expected activity on June 23. S&P Global Manufacturing PMI Flash reached 55.7 versus consensus 54.8, while services PMI hit 51.3. ADP Employment Change came in at 30,750, lifting the prior reading.

Equity markets responded positively, with the S&P 500 advancing 0.83% to 7,481.86 and Russell 2000 gaining 1.42%. Treasury yields moved higher, with the 2Y at 4.24% and 10Y at 4.51%. The USD/JPY edged up 0.07% to 161.68 while EUR/USD fell 0.74% to 1.13.

Gold declined 1.27% to 4,077.50 amid the risk-on tone.

The Day Ahead

Attention turns to June 24 releases including New Home Sales expected at 640,000 and the Current Account Balance. EIA crude and gasoline inventory data will follow at 6:30 ET. The Federal Reserve Bank Stress Test Results at noon could influence bank capital expectations.

Markets will also monitor any follow-through from Fed Governor Waller’s June 22 speech. Tomorrow brings high-impact Core PCE and Durable Goods Orders, setting the tone for inflation and growth views.

Other Economic Notes

Labor market data continue to show moderate strength with unemployment at 4.3%. CPI inflation stands at 2.31% year-over-year, keeping price pressures contained near target. The Fed Funds Rate remains at 3.63%, supporting a data-dependent policy stance.

Treasury yields have risen across the curve, reflecting improved growth signals from PMI prints. Equity breadth improved as small-caps outperformed amid the positive risk sentiment.

Global Macro News

International developments carry limited direct spillovers to US assets. Iran’s central bank rejected any obligation to buy US farm goods, adding minor uncertainty to agricultural trade flows. Gulf states face calls to support Iranian reconstruction with an estimated $300 billion package.

Algeria and Namibia exited the FATF grey list after AML improvements, easing regional compliance risks. <i>↓ p.2</i>