US Macro Daily(Beta Mode)

Fed Independence Upheld Amid Soft Factory Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,354.02 | -0.05% |

| Nasdaq 100 | 29,118.24 | -1.09% |

| Dow Jones | 51,876.11 | -0.09% |

| Russell 2000 | 3,010.08 | +0.07% |

| USD/JPY | 161.91 | +0.08% |

| EUR/USD | 1.14 | +0.37% |

| GBP/USD | 1.33 | +0.48% |

| Gold | 4,029.40 | -1.21% |

| WTI Crude | 70.26 | +1.49% |

| Bitcoin | 60,253.25 | +1.21% |

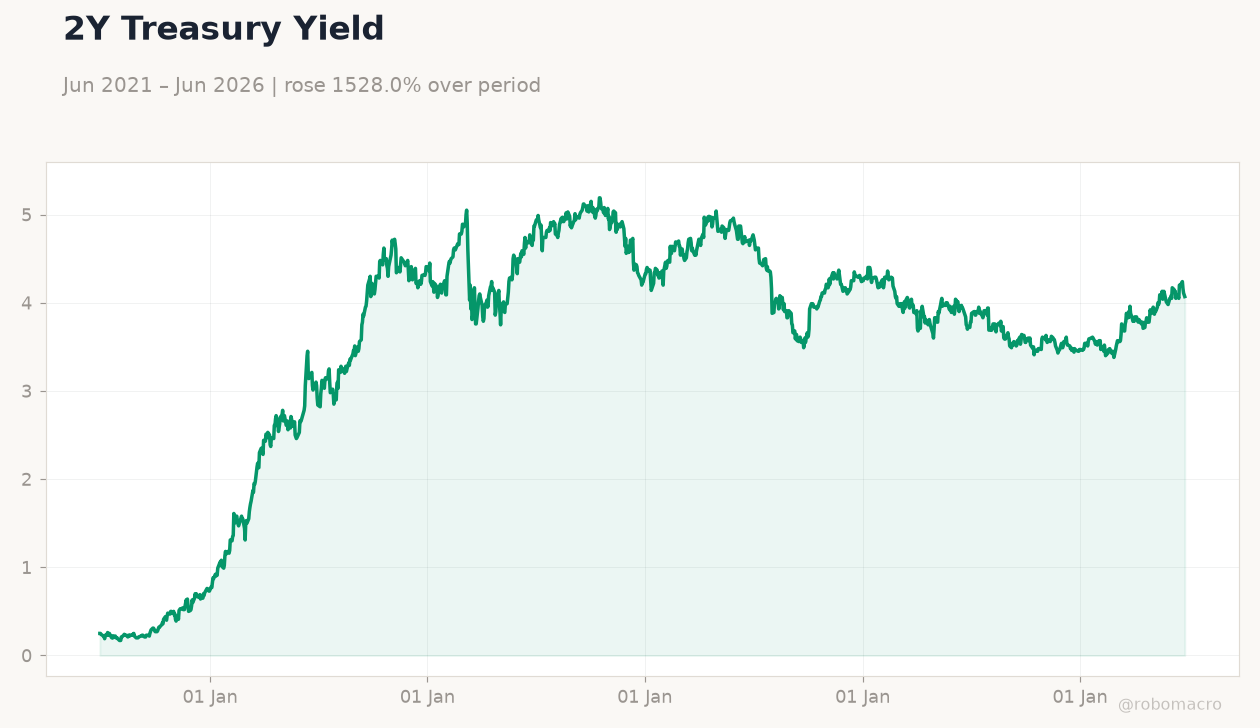

| US 2Y Treasury | 4.07% | -0.49% |

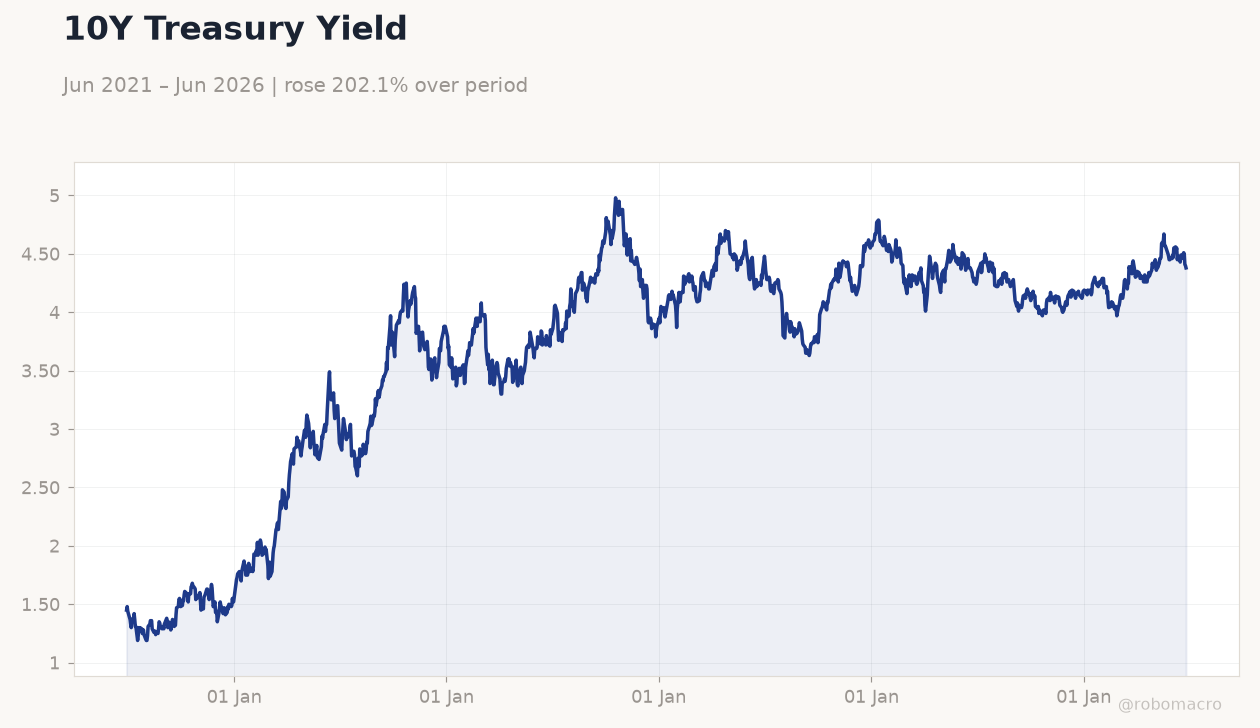

| US 10Y Treasury | 4.38% | -0.45% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Dallas Fed Manufacturing Index | 0.40 | - | 0 |

10Y Treasury Yield | Type: macro_line | Percent: 4.38 (2026-06-26) | Range: 1.19–4.98 | Trend(6pt): 1.45,3.97,3.89,4.35,4.41,4.38

10Y Treasury Yield | Type: macro_line | Percent: 4.38 (2026-06-26) | Range: 1.19–4.98 | Trend(6pt): 1.45,3.97,3.89,4.35,4.41,4.38

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-30) | |||

| S&P/Case-Shiller Home Price Year-over-Year | 0.80 | - | 05:00 |

| Chicago PMI | 62.70 | 60 | 05:45 |

| JOLTs Job Openings | 7.6m | 7.3m | 06:00 |

| Cb Consumer Confidence | 93.10 | - | 06:00 |

| API Weekly Crude Oil Stocks | -765,000 | - | 12:30 |

| Wednesday (2026-07-01) | |||

| MBA 30-Year Mortgage Rate | 6.59 | - | 03:00 |

| ADP Employment Change | 122,000 | 113,000 | 04:15 |

| Fed Chair Warsh Speech | - | - | 05:00 |

- Dallas Fed Manufacturing Index printed at 0, below prior 0.4, signaling softening factory activity.

- Equities closed mixed with S&P 500 down 0.05% at 7,354.02 while 10-year Treasury yields fell 4.5 bp to 4.38%.

- JOLTs Job Openings and ISM Manufacturing PMI headline the day-ahead calendar with potential to shift rate-cut odds.

Yesterday's Recap

The Dallas Fed Manufacturing Index fell to 0 on June 28, missing the prior reading of 0.4 and pointing to weaker regional factory conditions. Equity markets finished narrowly mixed as the S&P 500 slipped 0.05% to 7,354.02, the Nasdaq 100 dropped 1.09%, and the Dow Jones declined 0.09%. The Russell 2000 edged up 0.07%.

Treasury yields declined across the curve, with the 2-year note falling 4.9 bp to 4.07% and the 10-year note declining 4.5 bp to 4.38%. The dollar strengthened modestly against the yen while EUR/USD rose 0.37% to 1.14. Gold fell 1.21% to $4,029.40 per ounce and WTI crude gained 1.49% to $70.26.

The Day Ahead

S&P/Case-Shiller Home Price YoY and Chicago PMI are due at 5:00 a.m. and 5:45 a.m. ET, respectively, followed by JOLTs Job Openings and Conference Board Consumer Confidence at 6:00 a.m.

API crude oil inventory data arrives at 12:30 p.m. ET. Markets will also monitor any follow-through commentary on Federal Reserve independence after the Supreme Court blocked President Trump’s attempt to remove Governor Lisa Cook.

These releases could alter expectations for the 3.63% Fed funds rate path.

Other Economic Notes

US CPI inflation stands at 2.31% YoY while the unemployment rate is 4.30%, keeping the policy backdrop balanced. Treasury market pricing reflects reduced odds of near-term easing given the still-resilient labor market. Equity investors continue to focus on AI-driven earnings growth even as regional manufacturing data soften.

Oil prices remain sensitive to Middle East supply risks that could feed into headline inflation prints.

Global Macro News

Fresh US-Iran strikes tested the 60-day truce and raised energy supply concerns after the Strait of Hormuz closure talks stalled. Baltic states urged the EU to accelerate the Russian oil import ban amid these disruptions. The dollar-yen pair faced headwinds from Middle East uncertainty and persistent US inflation concerns.

<i>↓ p.2</i>