US Macro Daily(Beta Mode)

Tech Rally Lifts Equities as Yields Fall

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,440.43 | +1.18% |

| Nasdaq 100 | 29,774.75 | +2.25% |

| Dow Jones | 52,182.74 | +0.59% |

| Russell 2000 | 3,010.42 | +0.01% |

| USD/JPY | 162.40 | +0.38% |

| EUR/USD | 1.14 | +0.13% |

| GBP/USD | 1.32 | +0.15% |

| Gold | 4,028.60 | +0.16% |

| WTI Crude | 71.00 | +0.35% |

| Bitcoin | 58,322.08 | -3.02% |

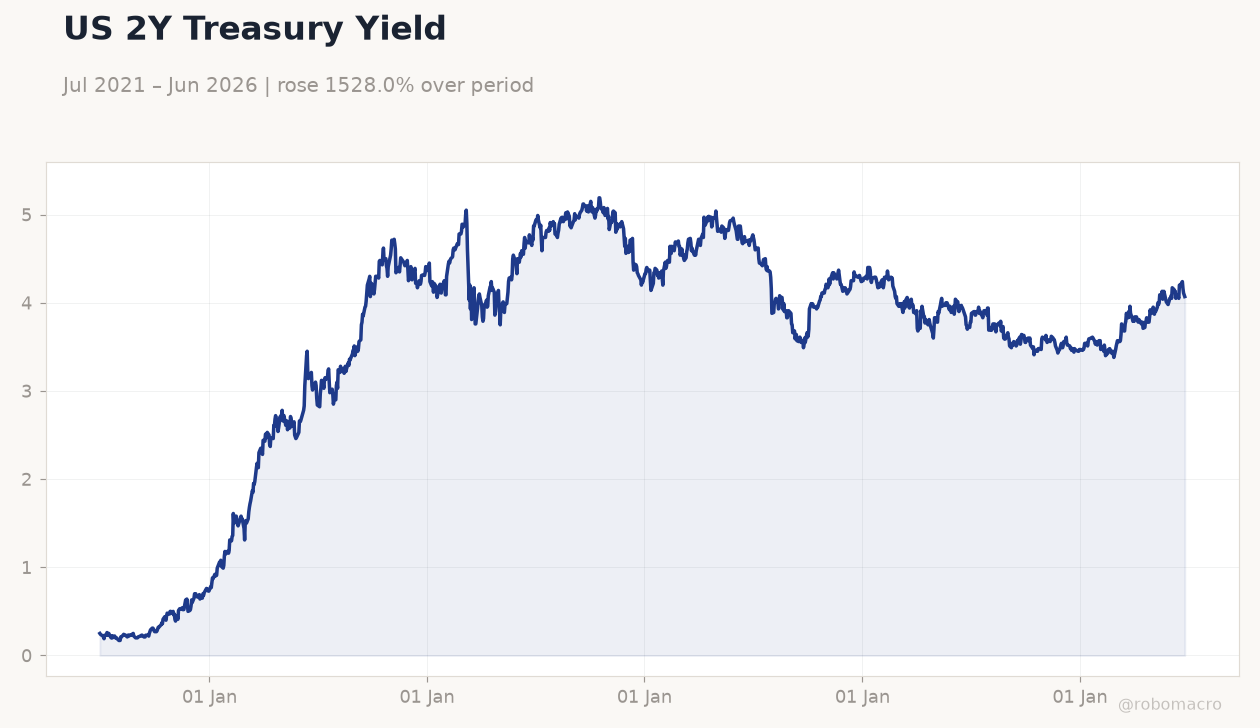

| US 2Y Treasury | 4.07% | -0.49% |

| US 10Y Treasury | 4.38% | -0.45% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Dallas Fed Manufacturing Index | 0.40 | - | 0 |

US 2Y Treasury Yield | Type: macro_line | Yield (%): 4.07 (2026-06-26) | Range: 0.17–5.19 | Trend(6pt): 0.25,4.07,4.2,3.97,4.09,4.07

US 2Y Treasury Yield | Type: macro_line | Yield (%): 4.07 (2026-06-26) | Range: 0.17–5.19 | Trend(6pt): 0.25,4.07,4.2,3.97,4.09,4.07

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-30) | |||

| S&P/Case-Shiller Home Price Year-over-Year | 0.80 | - | 05:00 |

| Chicago PMI | 62.70 | 60 | 05:45 |

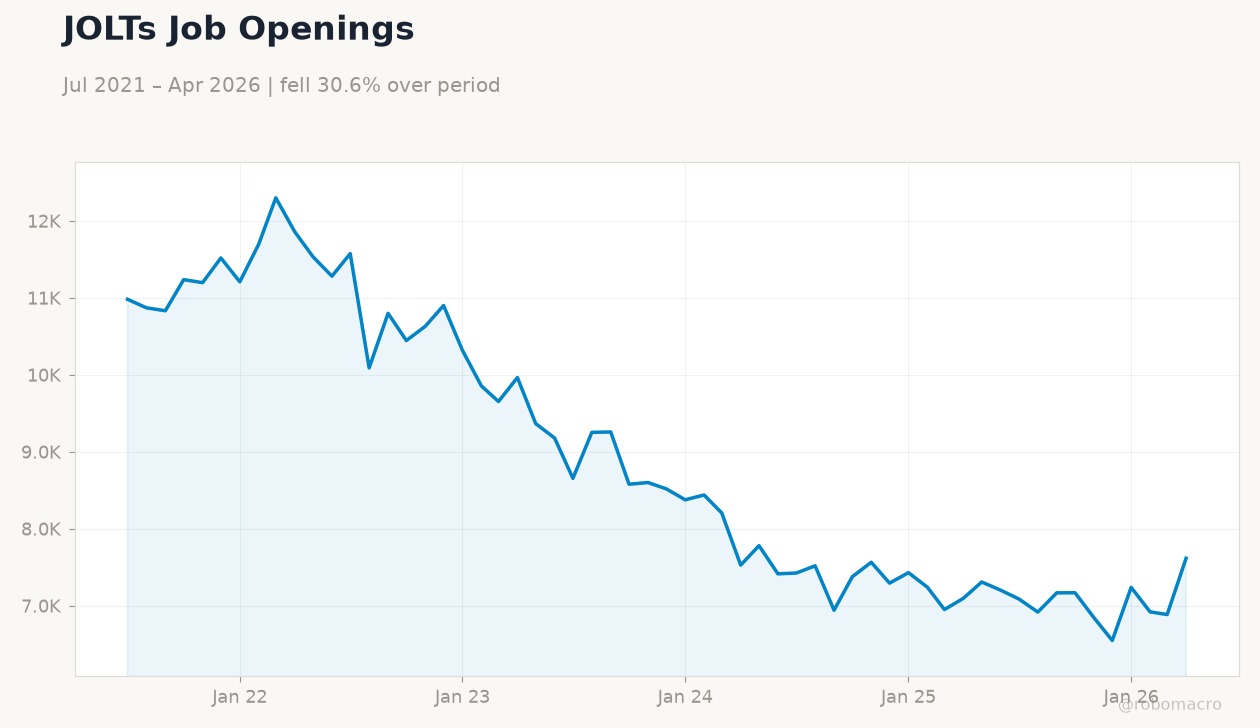

| JOLTs Job Openings | 7.6m | 7.3m | 06:00 |

| Cb Consumer Confidence | 93.10 | - | 06:00 |

| API Weekly Crude Oil Stocks | -765,000 | - | 12:30 |

| Wednesday (2026-07-01) | |||

| MBA 30-Year Mortgage Rate | 6.59 | - | 03:00 |

| ADP Employment Change | 122,000 | 113,000 | 04:15 |

| Fed Chair Warsh Speech | - | - | 05:00 |

- S&P 500 rose 1.18% to 7,440.43 while Nasdaq 100 gained 2.25% on tech rebound.

- US 10-year Treasury yield fell 4.5 bp to 4.38% as Dallas Fed index printed zero.

- JOLTs job openings and ISM manufacturing PMI headline the next two sessions.

Yesterday's Recap

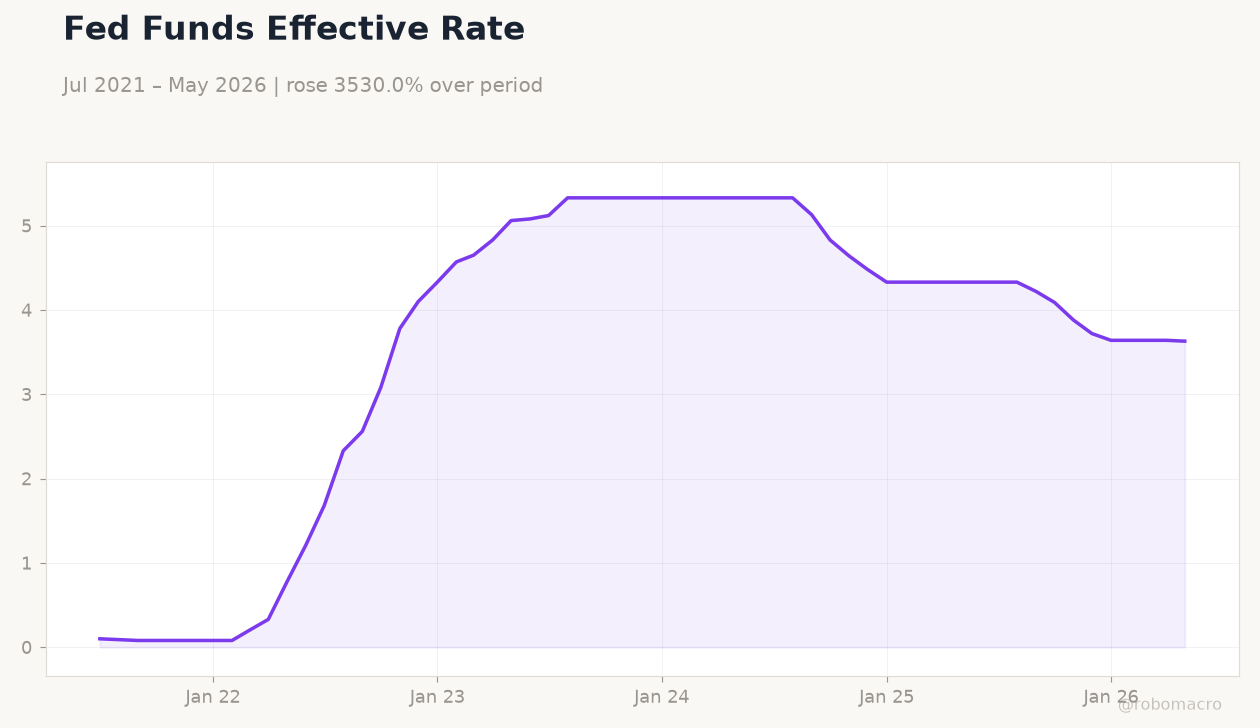

Equities advanced after the Dallas Fed Manufacturing Index registered zero versus the prior 0.4 reading, signaling softer regional factory conditions. The S&P 500 closed at 7,440.43, up 1.18%, while the Nasdaq 100 surged 2.25% to 29,774.75 on renewed buying in large-cap technology names. Treasury yields declined across the curve, with the 2-year note falling 4.9 bp to 4.07% and the 10-year note easing 4.5 bp to 4.38%.

The dollar firmed modestly, lifting USD/JPY 0.38% to 162.40. WTI crude edged 0.35% higher to $71.00 amid reports of upcoming US-Iran talks. Bitcoin declined 3.02% to $58,322.08, underperforming risk assets.

The Day Ahead

S&P/Case-Shiller home prices and Chicago PMI are due at 5:00 a.m. and 5:45 a.m. ET tomorrow, followed by JOLTs job openings and consumer confidence at 6:00 a.m.

ADP private payrolls and ISM manufacturing PMI headline Wednesday, with Fed Chair Warsh speaking at the ECB forum at 5:00 a.m. Oil inventory data from API and EIA will round out the calendar through Thursday. Markets will watch for any deviation from consensus on labor demand and factory activity.

Other Economic Notes

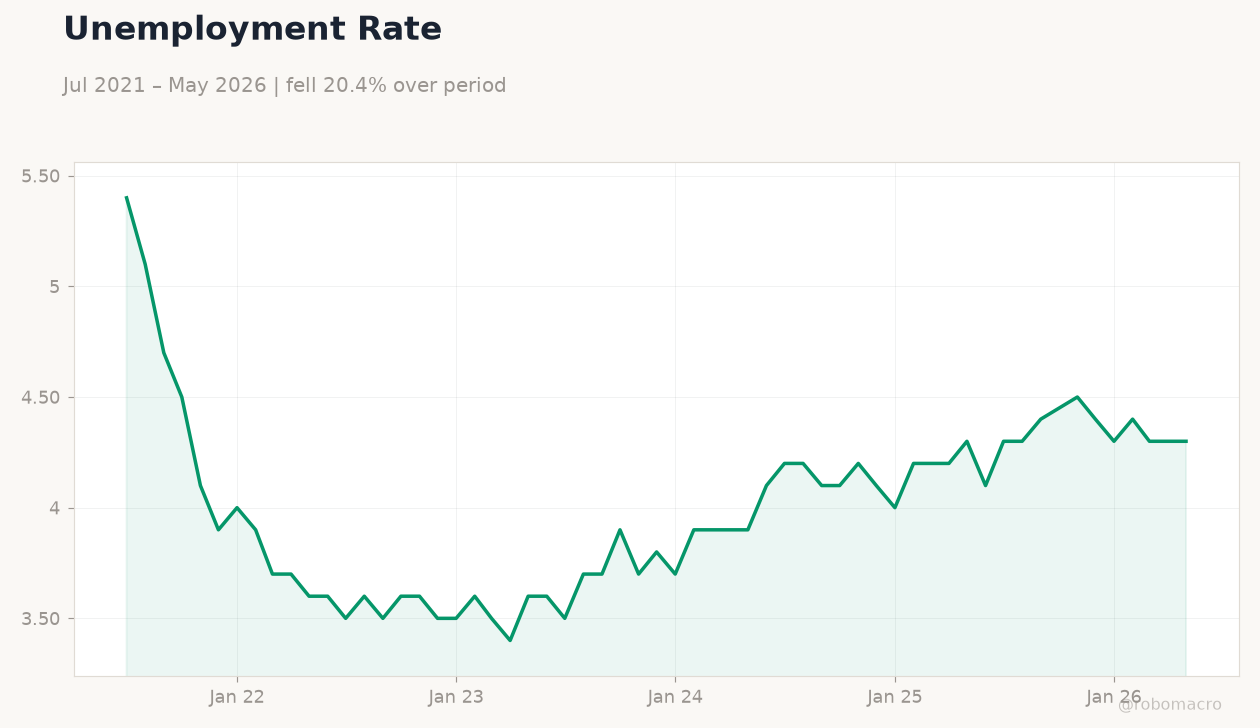

Corporate profit margins remain above historical averages, supporting equity valuations despite elevated index levels. The unemployment rate stands at 4.3% while CPI inflation prints 2.31% year-over-year, keeping the policy backdrop data-dependent. Treasury market liquidity has improved as foreign demand for US notes stays firm amid narrower rate differentials.

Equity futures point to continued outperformance in growth sectors ahead of the holiday-shortened week.

Global Macro News

Oil prices ticked higher after Iran and the United States scheduled further talks to ease recent tensions. The euro and sterling posted modest gains against the dollar, with EUR/USD at 1.14 and GBP/USD at 1.32. Global equity indices followed the US lead higher on optimism over AI-driven productivity gains.

<i>↓ p.2</i>