US Macro Daily(Beta Mode)

JOLTS Beat, ISM Misses as Warsh Signals Caution

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,499.36 | +0.79% |

| Nasdaq 100 | 30,276.35 | +1.68% |

| Dow Jones | 52,319.20 | +0.26% |

| Russell 2000 | 3,024.37 | +0.46% |

| USD/JPY | 162.53 | +0.38% |

| EUR/USD | 1.14 | -0.33% |

| GBP/USD | 1.33 | +0.18% |

| Gold | 4,085.00 | +1.54% |

| WTI Crude | 68.22 | -1.84% |

| Bitcoin | 60,117.92 | +2.66% |

| US 2Y Treasury | 4.10% | +0.74% |

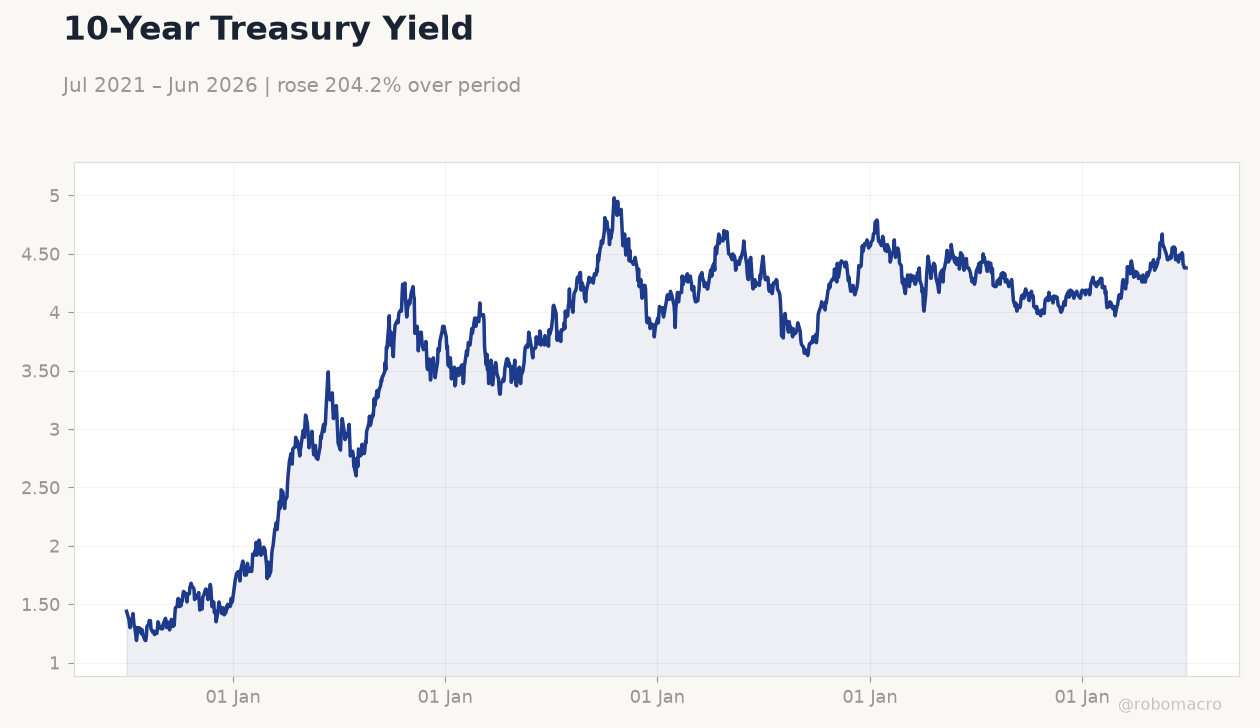

| US 10Y Treasury | 4.38% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Dallas Fed Manufacturing Index | 0.40 | - | 0 |

| S&P/Case-Shiller Home Price Year-over-Year | 0.90 | 0.90 | 1.10 |

| Chicago PMI | 62.70 | 58.10 | 56.70 |

| JOLTs Job Openings | 7.6m | 7.3m | 7.6m |

| Cb Consumer Confidence | 90.60 | - | 91.20 |

| API Weekly Crude Oil Stocks | -765,000 | -4.1m | -6.1m |

| MBA 30-Year Mortgage Rate | 6.59 | - | 6.57 |

| ADP Employment Change | 122,000 | 113,000 | 98,000 |

| Fed Chair Warsh Speech | - | - | - |

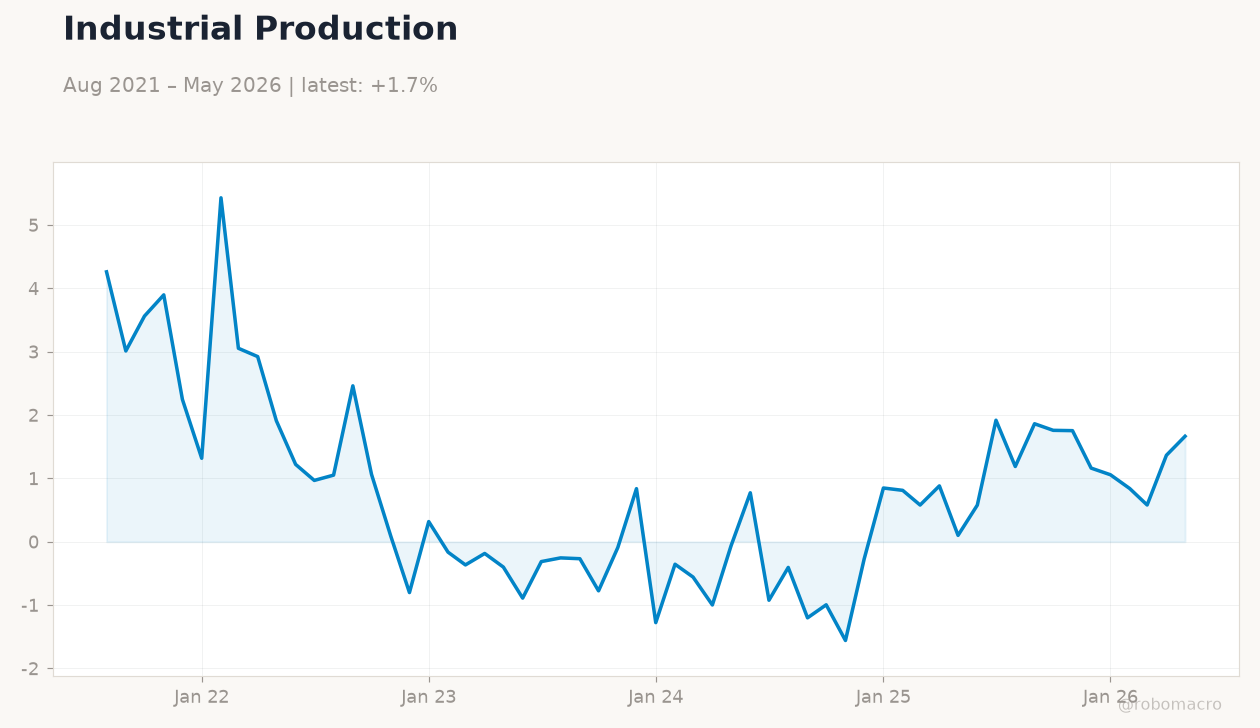

| ISM Manufacturing PMI | 54 | 54 | 53.30 |

10-Year Treasury Yield | Type: macro_line | %: 4.38 (2026-06-29) | Range: 1.19–4.98 | Trend(5pt): 1.44,3.76,3.84,4.27,4.38

10-Year Treasury Yield | Type: macro_line | %: 4.38 (2026-06-29) | Range: 1.19–4.98 | Trend(5pt): 1.44,3.76,3.84,4.27,4.38

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-07-02) | |||

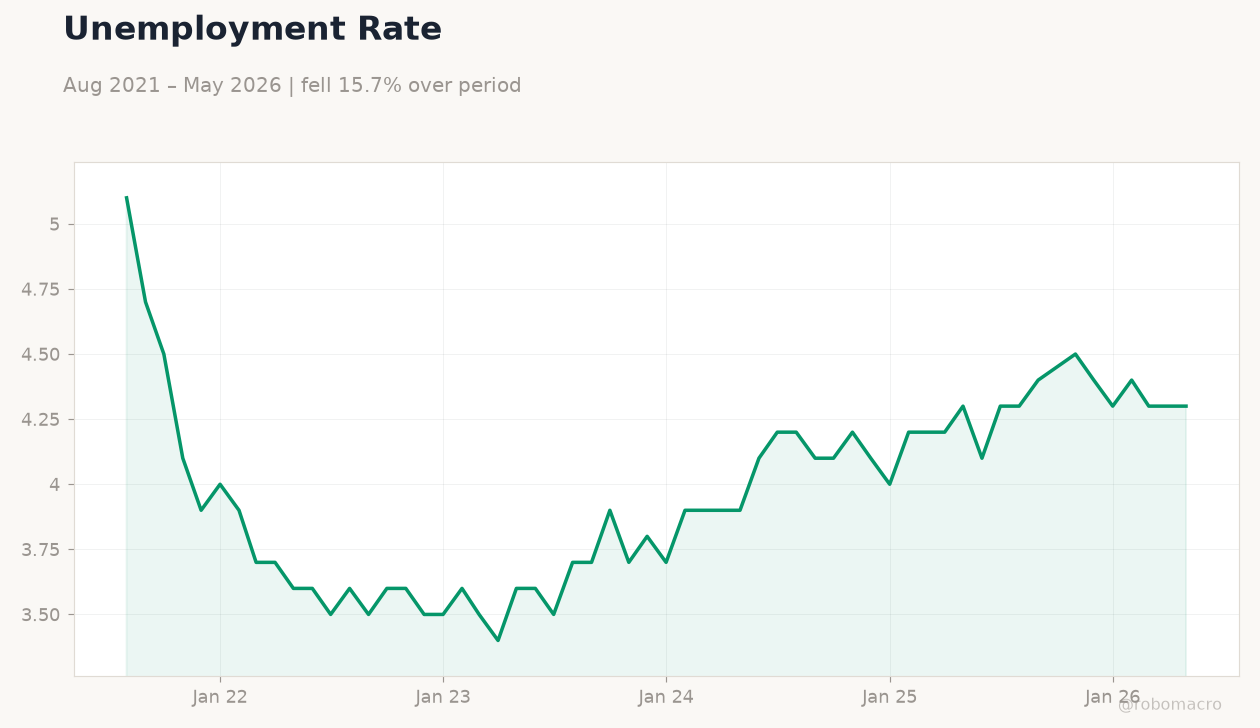

| Headline Unemployment Rate | 4.30 | 4.30 | 04:30 |

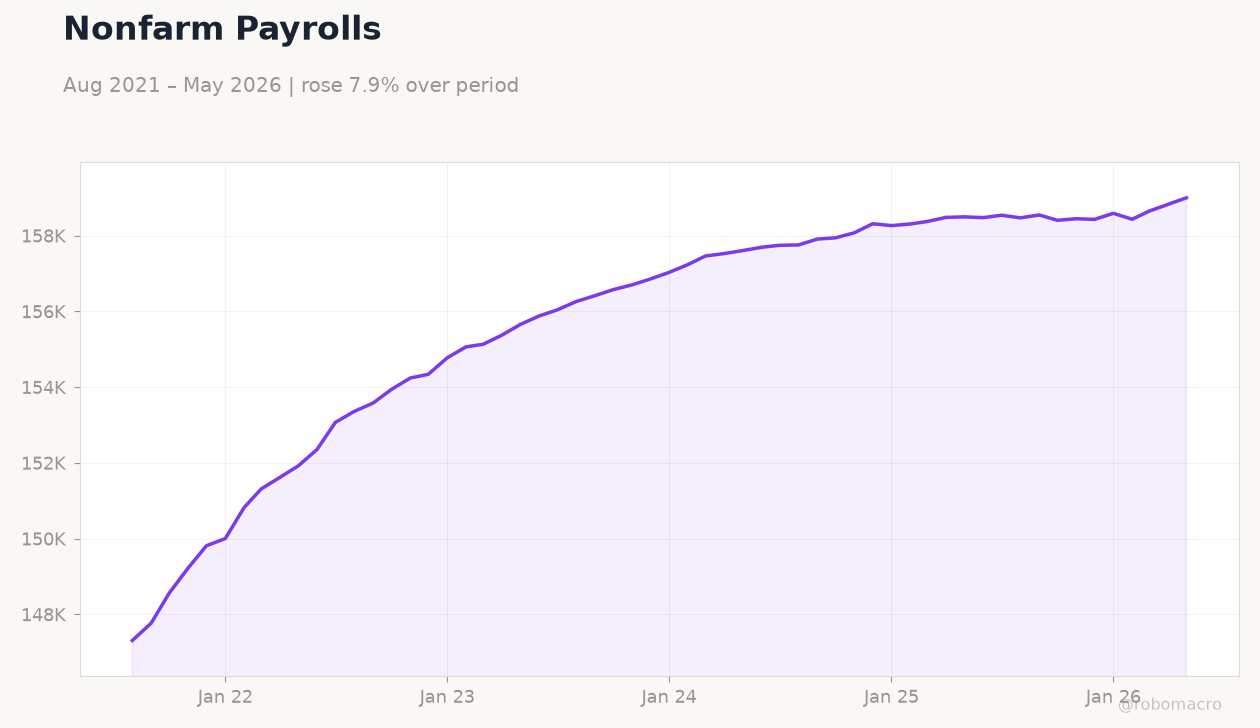

| Payroll Jobs Growth | 172,000 | 110,000 | 04:30 |

| Annual Wage Growth | 3.40 | 3.50 | 04:30 |

| Labor Force Participation | 61.80 | - | 04:30 |

| Monthly Wage Growth | 0.30 | 0.30 | 04:30 |

| Weekly Jobless Claims | 215,000 | 220,000 | 04:30 |

| Factory Orders Month-over-Month | 4.80 | -2.10 | 06:00 |

- JOLTs job openings rose to 7.594 million, beating consensus of 7.3 million and signaling labor resilience.

- Chicago PMI dropped to 56.7 versus 58.1 expected, while Case-Shiller home prices accelerated to 1.1% y/y.

- S&P 500 gained 0.79% and Nasdaq 100 rose 1.68% as investors digested mixed data and Warsh remarks.

Yesterday's Recap

US data on June 30 showed labor demand holding up better than expected. JOLTs job openings reached 7.594 million against a 7.3 million consensus, while consumer confidence edged up to 91.2. Chicago PMI fell sharply to 56.7 from 62.7 previously, missing forecasts, and Case-Shiller home prices climbed to 1.1% y/y.

Equity markets advanced with the S&P 500 closing at 7,499.36 and Nasdaq 100 at 30,276.35. The 2-year Treasury yield rose 3 basis points to 4.10% while the 10-year held at 4.38%. WTI crude fell 1.84% to 68.22 amid inventory builds, and gold climbed 1.54% to 4,085.

ADP employment came in at 98,000, below the 113,000 consensus.

The Day Ahead

Markets await the July 2 jobs report at 8:30 a.m. ET, with payroll growth and the 4.3% unemployment rate in focus. ISM manufacturing details and any follow-up from Chair Warsh’s European Central Bank forum remarks could influence rate expectations.

Treasury auctions and oil inventory updates may add volatility to yields and energy prices. Fed speakers are limited, keeping attention on incoming labor data and its implications for the 3.63% fed funds rate.

Other Economic Notes

Home price gains and steady consumer confidence point to resilient household balance sheets despite higher borrowing costs. Manufacturing employment improved modestly in the ISM survey, yet overall factory activity cooled. Oil inventory draws and gasoline stock declines suggest tightening supply conditions that could support prices later in the summer.

Broader equity leadership by small caps and technology shares reflects optimism over growth without immediate recession signals.

Global Macro News

European indices outperformed US peers in June amid diverging policy paths. Brazil and regional partners highlighted Argentina’s widening travel deficit, indirectly pressuring USD demand in Latin America. CMA CGM’s $1.4 billion acquisition of FedEx supply-chain assets signals continued consolidation in global logistics.

<i>↓ p.2</i>