US Macro Daily(Beta Mode)

Warsh Eases Inflation Fears Ahead of Jobs Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,483.23 | -0.22% |

| Nasdaq 100 | 29,809.13 | -1.54% |

| Dow Jones | 52,305.24 | -0.03% |

| Russell 2000 | 3,012.59 | -0.39% |

| USD/JPY | 161.04 | -0.98% |

| EUR/USD | 1.15 | +0.34% |

| GBP/USD | 1.34 | +0.83% |

| Gold | 4,138.60 | +1.73% |

| WTI Crude | 67.55 | -1.50% |

| Bitcoin | 61,477.38 | +2.46% |

| US 2Y Treasury | 4.14% | +0.98% |

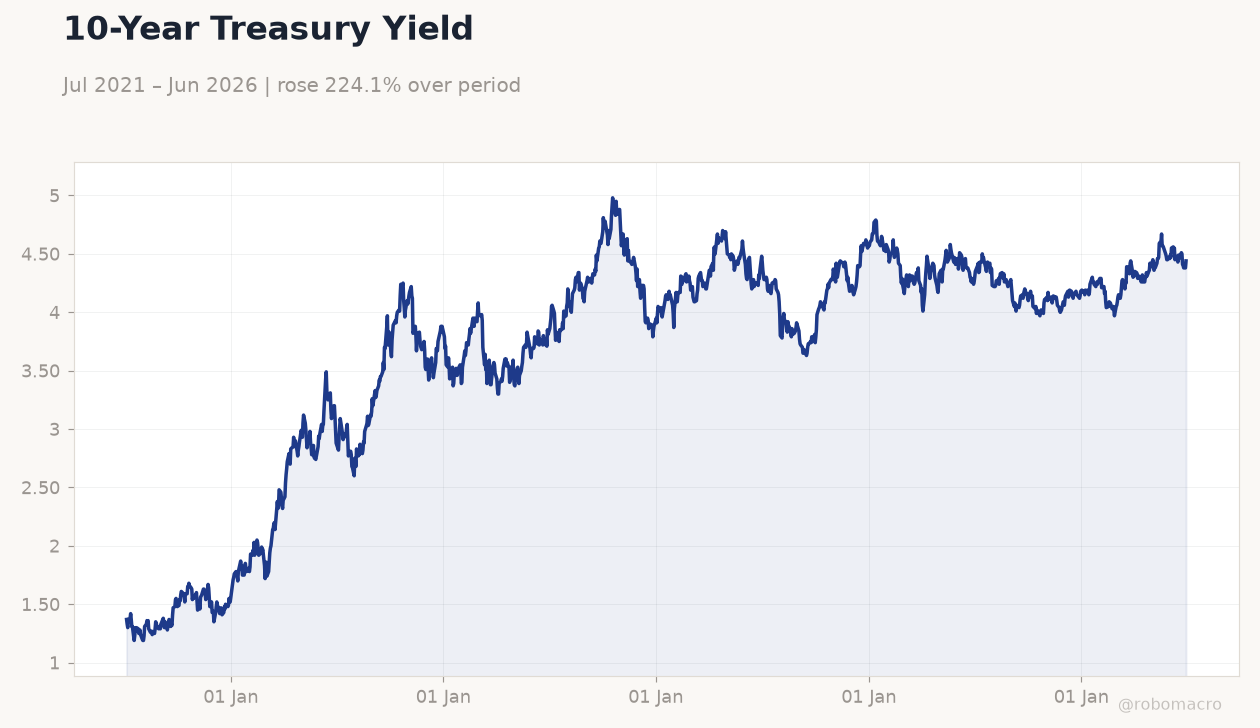

| US 10Y Treasury | 4.44% | +1.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Dallas Fed Manufacturing Index | 0.40 | - | 0 |

| S&P/Case-Shiller Home Price Year-over-Year | 0.90 | 0.90 | 1.10 |

| Chicago PMI | 62.70 | 58.10 | 56.70 |

| JOLTs Job Openings | 7.6m | 7.3m | 7.6m |

| Cb Consumer Confidence | 90.60 | - | 91.20 |

| API Weekly Crude Oil Stocks | -765,000 | -4.1m | -6.1m |

| MBA 30-Year Mortgage Rate | 6.59 | - | 6.57 |

| ADP Employment Change | 122,000 | 113,000 | 98,000 |

| Fed Chair Warsh Speech | - | - | - |

| ISM Manufacturing PMI | 54 | 54 | 53.30 |

10-Year Treasury Yield | Type: macro_line | 10Y Yield %: 4.44 (2026-06-30) | Range: 1.19–4.98 | Trend(6pt): 1.37,3.83,3.88,4.23,4.38,4.44

10-Year Treasury Yield | Type: macro_line | 10Y Yield %: 4.44 (2026-06-30) | Range: 1.19–4.98 | Trend(6pt): 1.37,3.83,3.88,4.23,4.38,4.44

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-07-02) | |||

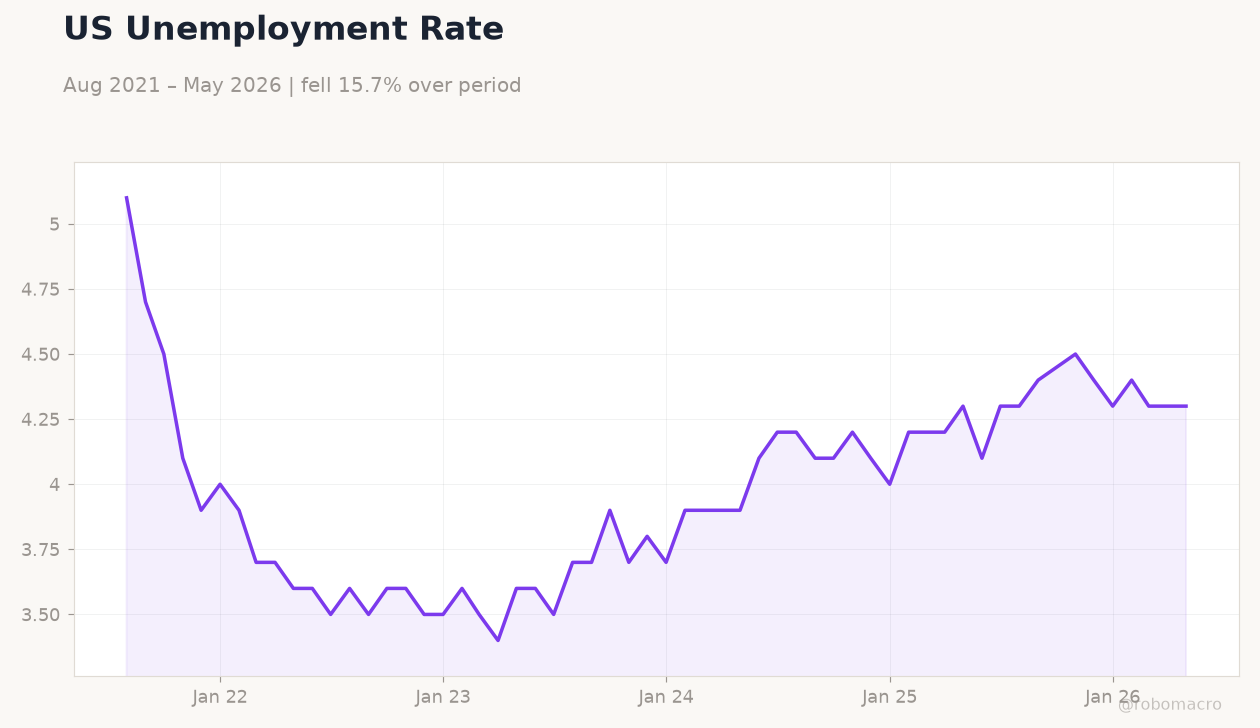

| Headline Unemployment Rate | 4.30 | 4.30 | 04:30 |

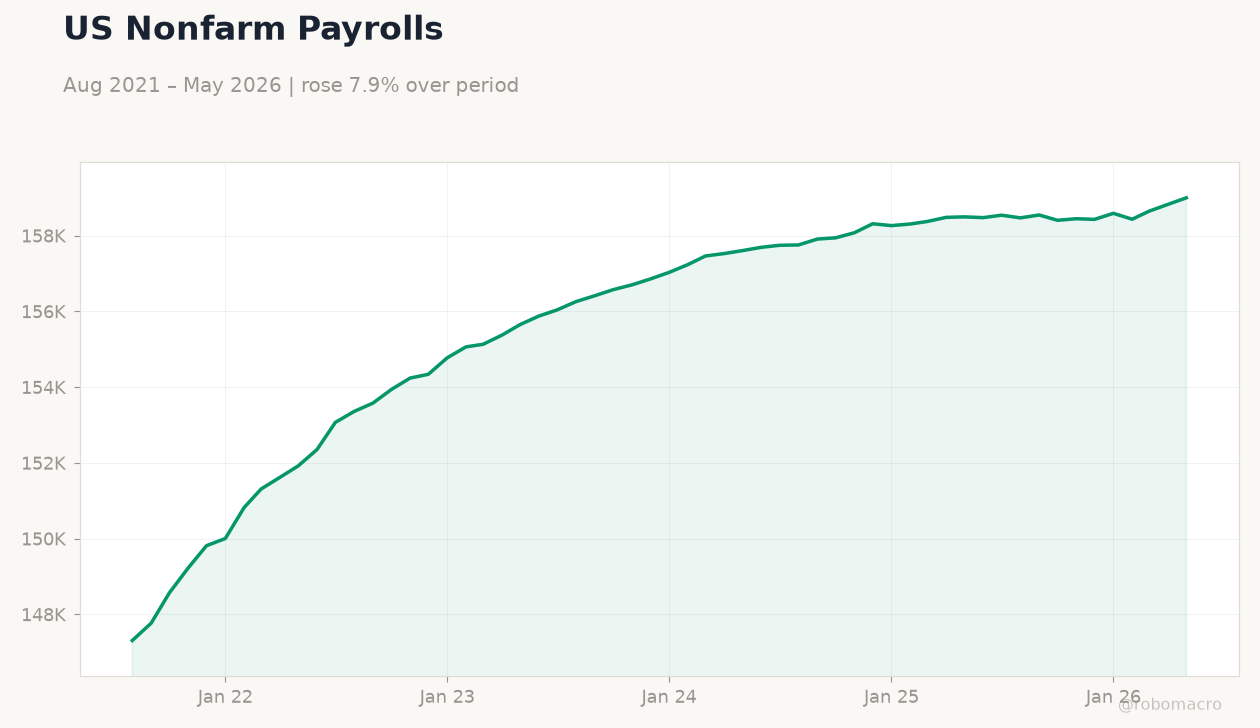

| Payroll Jobs Growth | 172,000 | 110,000 | 04:30 |

| Annual Wage Growth | 3.40 | 3.50 | 04:30 |

| Labor Force Participation | 61.80 | - | 04:30 |

| Monthly Wage Growth | 0.30 | 0.30 | 04:30 |

| Weekly Jobless Claims | 215,000 | 220,000 | 04:30 |

| Factory Orders Month-over-Month | 4.80 | -2.10 | 06:00 |

- JOLTs job openings beat expectations while Chicago PMI contracted sharply.

- Treasury yields rose as Fed Chair Warsh signaled lower inflation risks.

- ADP employment missed forecasts, adding caution before Friday’s payrolls.

Yesterday's Recap

US data released June 30 showed resilience in housing and labor demand alongside softening manufacturing sentiment. S&P/Case-Shiller home prices rose 1.1% year-over-year, above the 0.9% consensus. JOLTs job openings climbed to 7.594 million versus 7.3 million expected, while Chicago PMI fell to 56.7 from 62.7.

Consumer confidence edged higher to 91.2. Equity markets closed mixed with the S&P 500 down 0.22% and Nasdaq 100 falling 1.54%. The 10-year Treasury yield increased 1.37% to 4.44%, and gold advanced 1.73% to $4,138.60.

Oil inventories declined more than forecast, pushing WTI crude down 1.50% to $67.55.

The Day Ahead

Markets will focus on the July 2 employment report, with consensus calling for 4.3% unemployment and 110,000 payroll gains. ADP private employment rose only 98,000 in June, below the 113,000 estimate. ISM manufacturing PMI slipped to 53.3 from 54.0, with the employment sub-index improving modestly to 49.7.

Fed Chair Warsh is scheduled to speak at the ECB forum, where further comments on inflation and policy independence are expected. Treasury yields are likely to remain sensitive to any shifts in rate-cut expectations.

Other Economic Notes

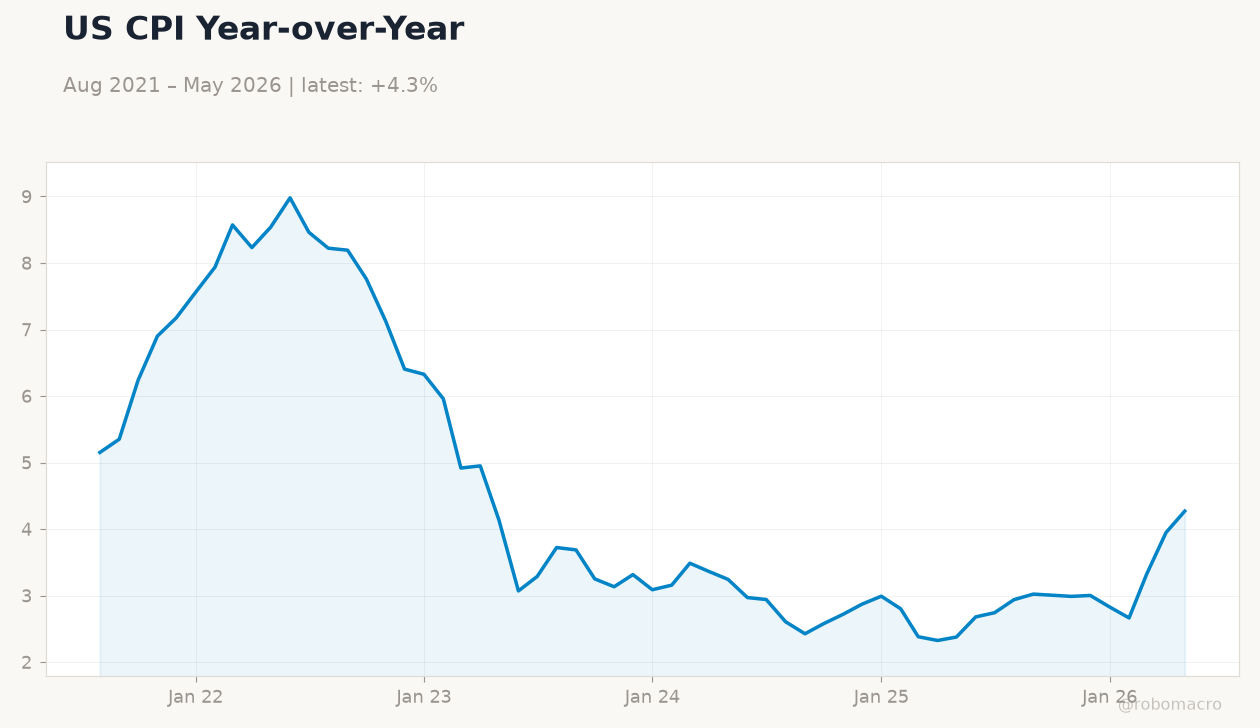

The labor market remains above full employment with the unemployment rate at 4.30%. CPI inflation stands at 2.31% year-over-year, still above the Fed’s 2% target. The federal funds rate sits at 3.63%, leaving real policy rates restrictive.

Recent inventory draws in crude and gasoline suggest tighter energy supply that could support headline inflation readings. Equity breadth narrowed as technology shares lagged despite the broader market holding near record levels.

Global Macro News

European equities outperformed US indices in June amid diverging growth trajectories. UK defense spending plans totaling £300 billion over four years may lift euro-area yields further. Eurozone bond yields tracked US Treasuries higher ahead of the American jobs report.

<i>↓ p.2</i>