US Macro Daily(Beta Mode)

Weak June Jobs Lift Rate-Cut Odds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,483.24 | +0.00% |

| Nasdaq 100 | 29,329.21 | -1.61% |

| Dow Jones | 52,900.07 | +1.14% |

| Russell 2000 | 2,996.11 | -0.55% |

| USD/JPY | 161.21 | -0.82% |

| EUR/USD | 1.14 | +0.62% |

| GBP/USD | 1.34 | +0.53% |

| Gold | 4,184.80 | +1.75% |

| WTI Crude | 68.25 | -0.64% |

| Bitcoin | 61,948.40 | +0.75% |

| US 2Y Treasury | 4.17% | +0.72% |

| US 10Y Treasury | 4.48% | +0.90% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Dallas Fed Manufacturing Index | 0.40 | - | 0 |

| S&P/Case-Shiller Home Price Year-over-Year | 0.90 | 0.90 | 1.10 |

| Chicago PMI | 62.70 | 58.10 | 56.70 |

| JOLTs Job Openings | 7.6m | 7.3m | 7.6m |

| Cb Consumer Confidence | 90.60 | - | 91.20 |

| API Weekly Crude Oil Stocks | -765,000 | -4.1m | -6.1m |

| MBA 30-Year Mortgage Rate | 6.59 | - | 6.57 |

| ADP Employment Change | 122,000 | 113,000 | 98,000 |

| Fed Chair Warsh Speech | - | - | - |

| ISM Manufacturing PMI | 54 | 54 | 53.30 |

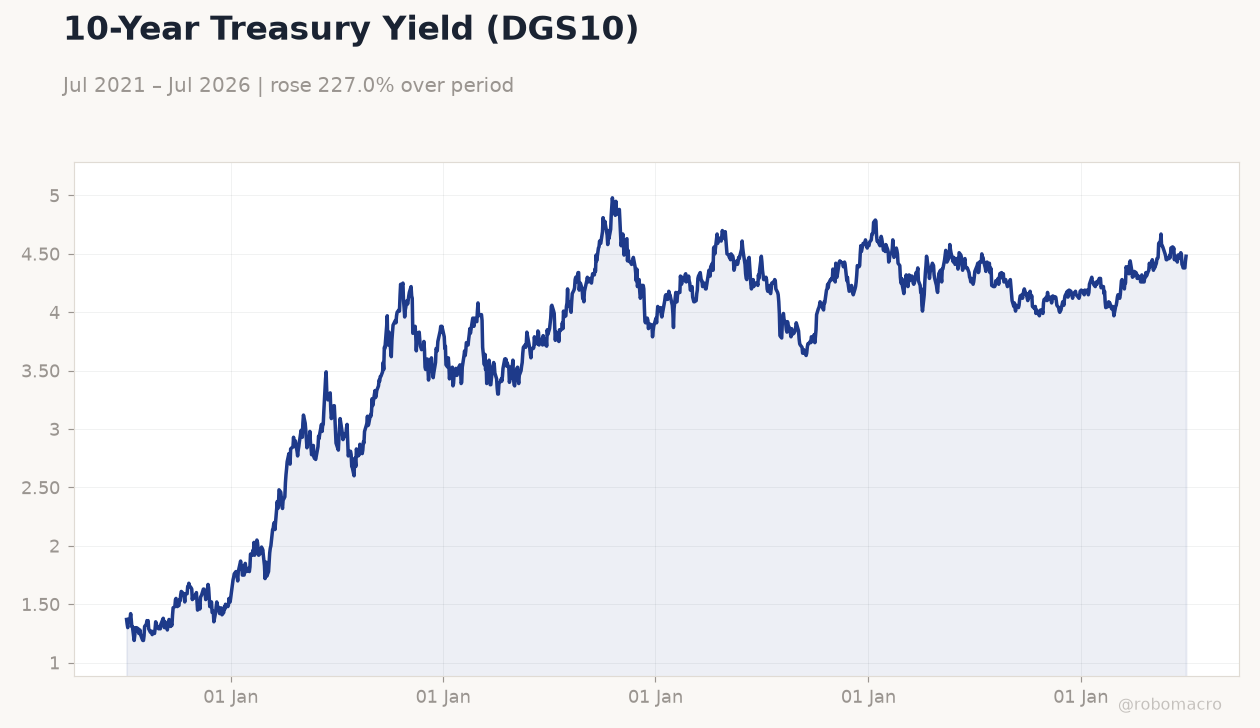

10-Year Treasury Yield (DGS10) | Type: macro_line | Percent: 4.48 (2026-07-01) | Range: 1.19–4.98 | Trend(6pt): 1.37,3.83,3.88,4.23,4.38,4.48

10-Year Treasury Yield (DGS10) | Type: macro_line | Percent: 4.48 (2026-07-01) | Range: 1.19–4.98 | Trend(6pt): 1.37,3.83,3.88,4.23,4.38,4.48

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

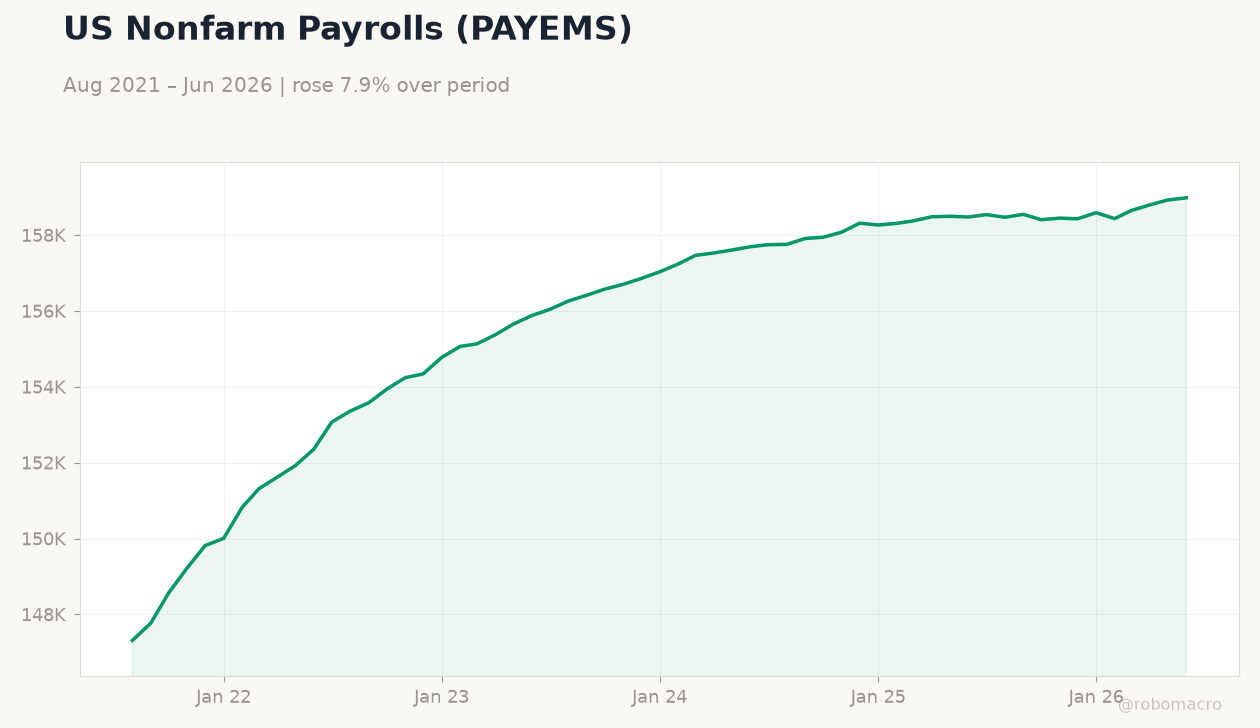

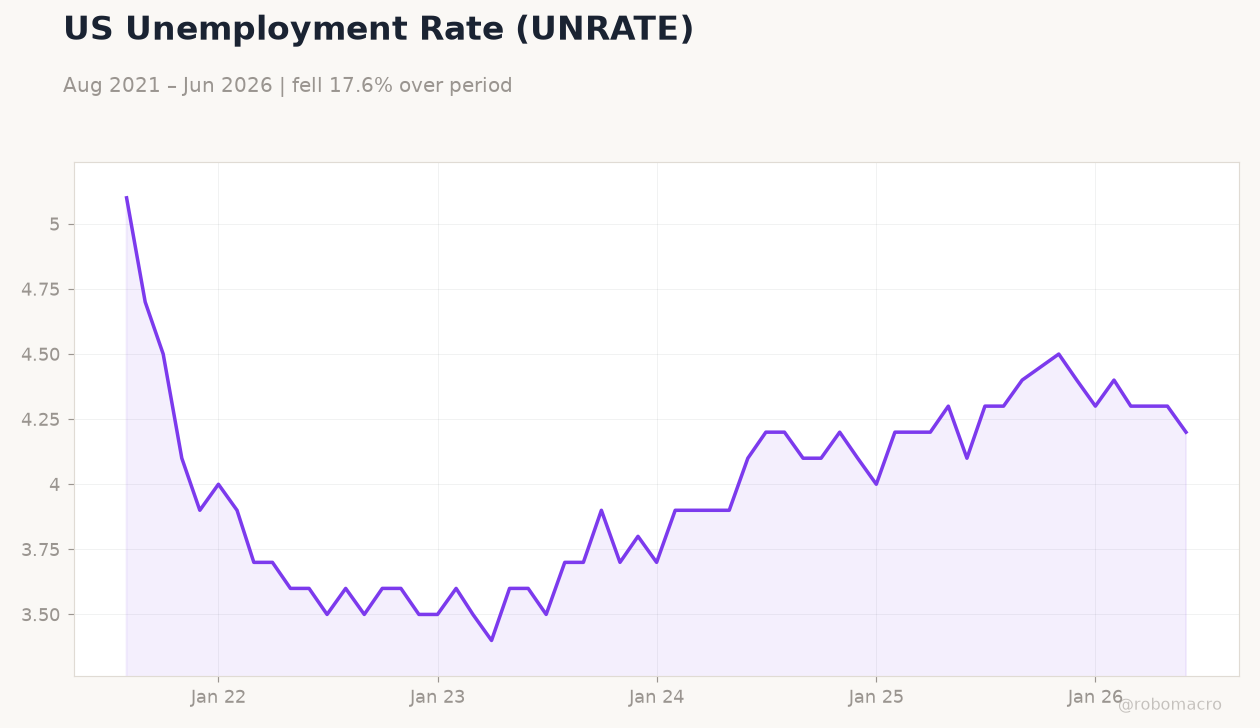

- US nonfarm payrolls rose just 57k in June versus 110k expected, with unemployment falling to 4.2%

- ISM manufacturing slipped to 53.3 while ADP employment printed 98k, confirming labor softening

- Equities mixed as Dow rose 1.14% and Nasdaq fell 1.61%; gold climbed 1.75% amid higher Treasury yields

Yesterday's Recap

June payrolls growth of 57k missed forecasts by a wide margin while the unemployment rate edged down to 4.2%. ADP private payrolls added only 98k, and ISM manufacturing eased to 53.3 with the employment sub-index at 49.7. JOLTs job openings held near 7.594 million and Case-Shiller home prices rose 1.1% year-over-year.

Markets reacted with the Dow Jones advancing 1.14% to 52,900 while the Nasdaq 100 declined 1.61%. The 10-year Treasury yield rose 0.90% to 4.48% and gold advanced 1.75% to $4,184.80 as the dollar index retreated. WTI crude fell 0.64% to $68.25.

The Day Ahead

No major US data releases are scheduled for July 3 ahead of the Independence Day holiday. Markets will digest the weak payrolls print and watch for any follow-up commentary from regional Fed officials. Thin pre-holiday volume is likely to keep equity and FX volatility contained.

Treasury futures and gold will remain sensitive to any shift in rate-cut pricing. Positioning for next week’s inflation and retail sales prints will begin to build.

Other Economic Notes

The sharp June payrolls miss reinforces the view that labor-market cooling is underway even as unemployment sits at 4.2%. Earlier weakness in Chicago PMI and ISM new orders points to softening demand across manufacturing. Mortgage rates eased to 6.57%, providing modest support to housing activity.

Oil inventory draws and lower gasoline stocks added downward pressure on energy prices, further reducing near-term inflation risks.

Global Macro News

Canada posted its strongest monthly growth since last summer, supporting North American demand for US exports. Mexico and Canada are exploring alternatives after US officials declined to renew USMCA provisions, raising longer-term trade uncertainty. Tesla’s 25% European sales rebound highlights resilient external demand despite softer US hiring.

India’s rapid expansion was cited by US officials as a benchmark, underscoring competitive pressures on American growth. <i>↓ p.2</i>