Global Macro Watch

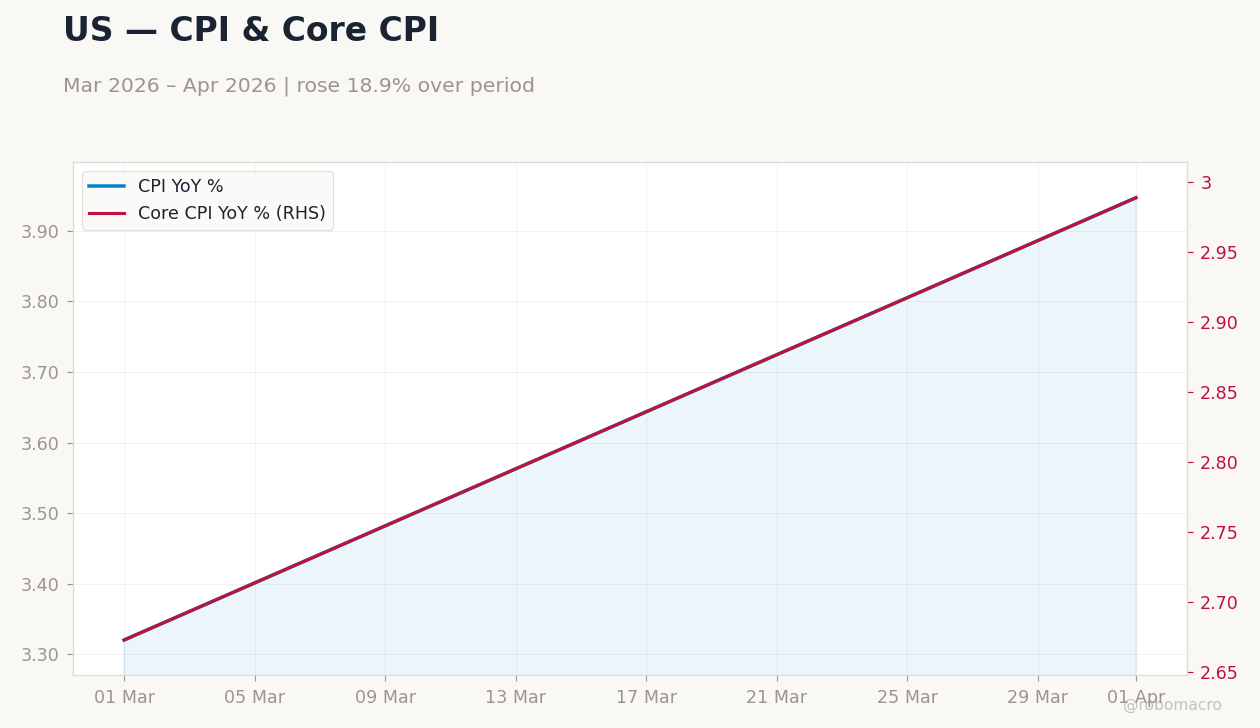

BETA- US CPI and PPI both exceeded forecasts, confirming the clearest inflation upside surprise of the week and reversing prior-week oil-relief momentum.

- Brent crude climbed 4.85% to 109.26, providing fiscal support to exporters while raising imported-inflation risks for importers.

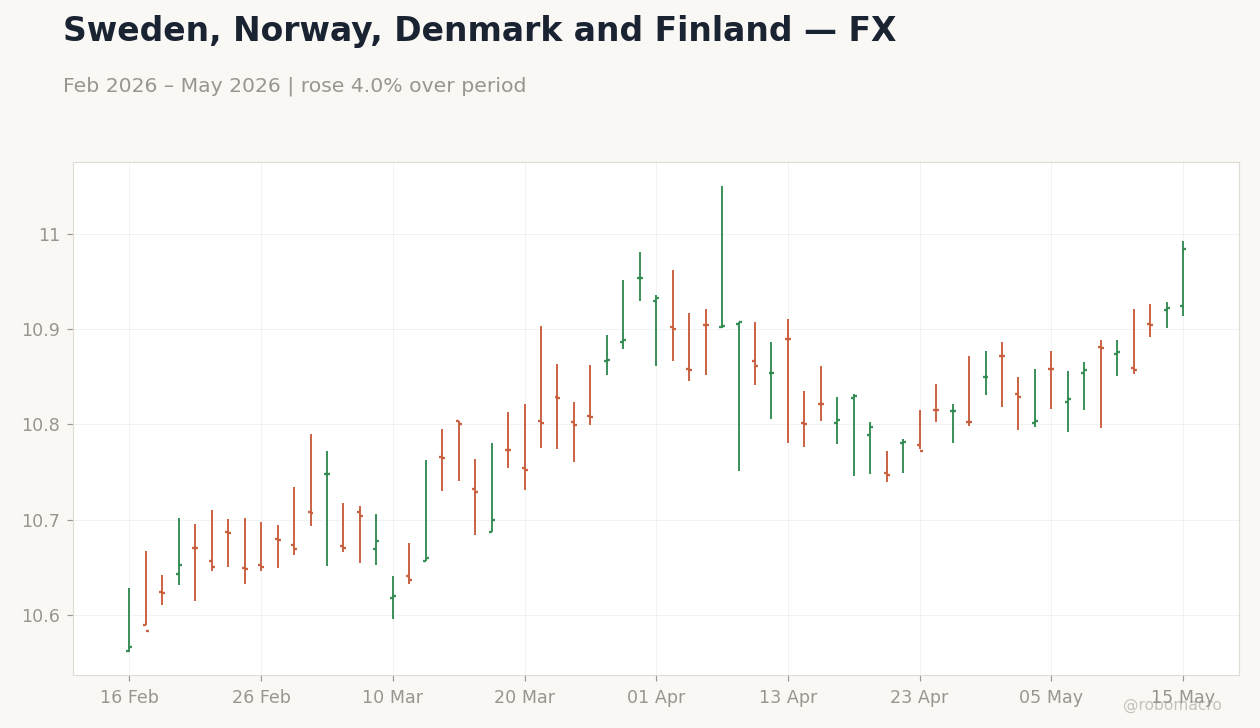

- Norges Bank delivered a surprise hike while the BoJ flagged near-term rate discussions, underscoring divergent DM policy vigilance.

- DXY rose 1.5% to 99.27 as Treasury 10-year yields climbed 23bp to 4.59%, driving broad equity weakness and EM currency pressure.

We enter the third week of May 2026 with the global cycle shifting from the oil-relief narrative that dominated the prior period. Last week’s sharp Brent decline had eased near-term inflation concerns and supported risk assets; this week’s reversal, with Brent advancing 4.85% to 109.26, has reintroduced upside price pressure at precisely the moment US inflation data surprised to the high side. The data suggests the expansion remains intact yet faces a fresh test: resilient demand continues to meet tighter energy supply, pushing headline and upstream prices higher and forcing investors to reassess the timing of monetary easing. Across regions, the dominant thread is therefore one of re-pricing rather than outright contraction, with markets now embedding fewer cuts and higher terminal rates than they did seven days earlier.

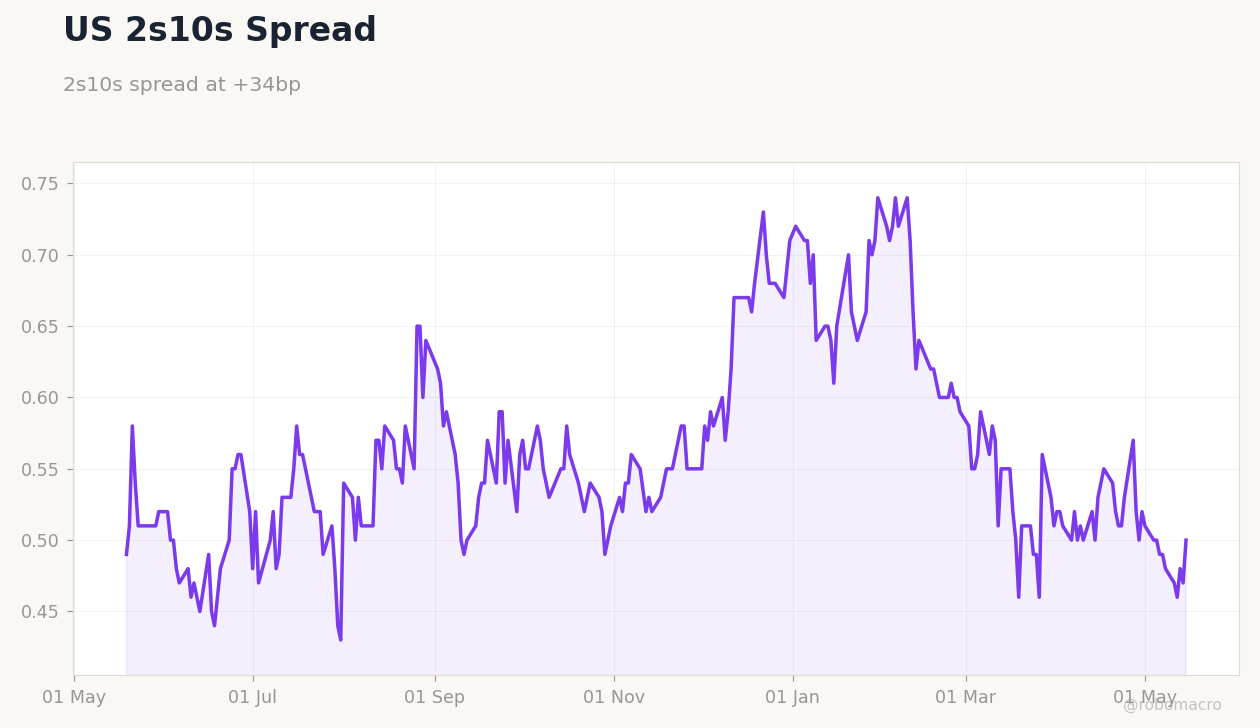

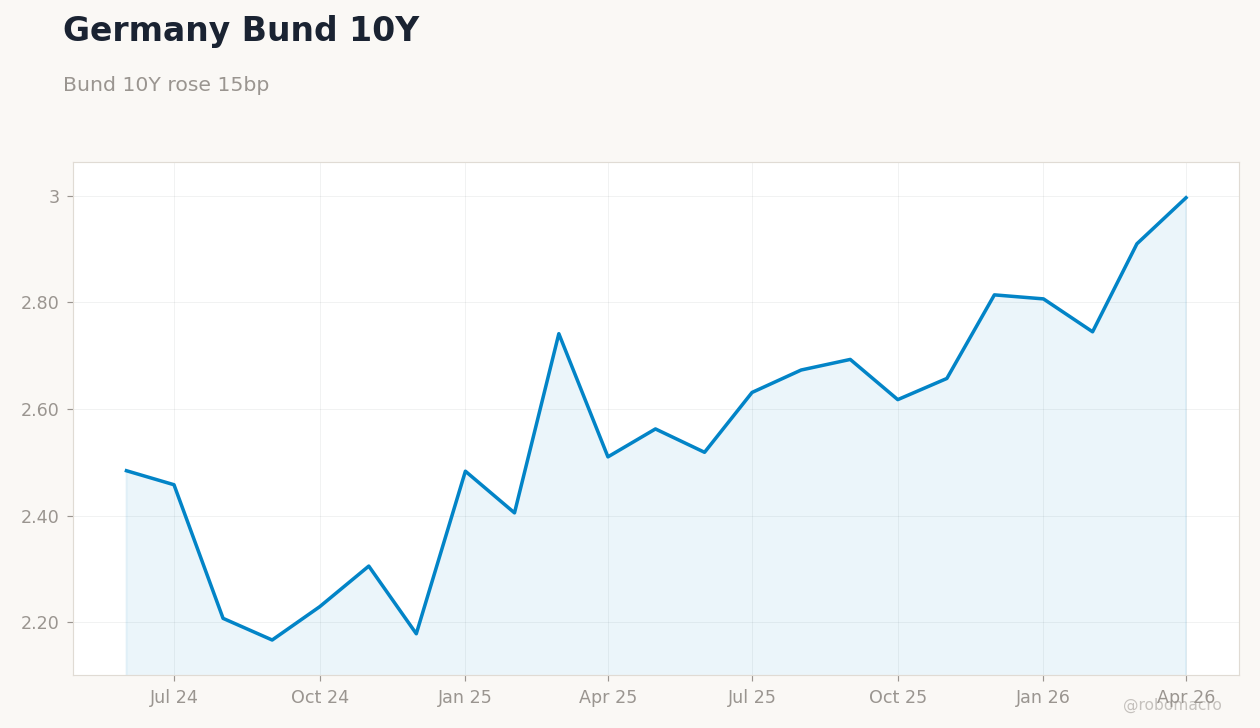

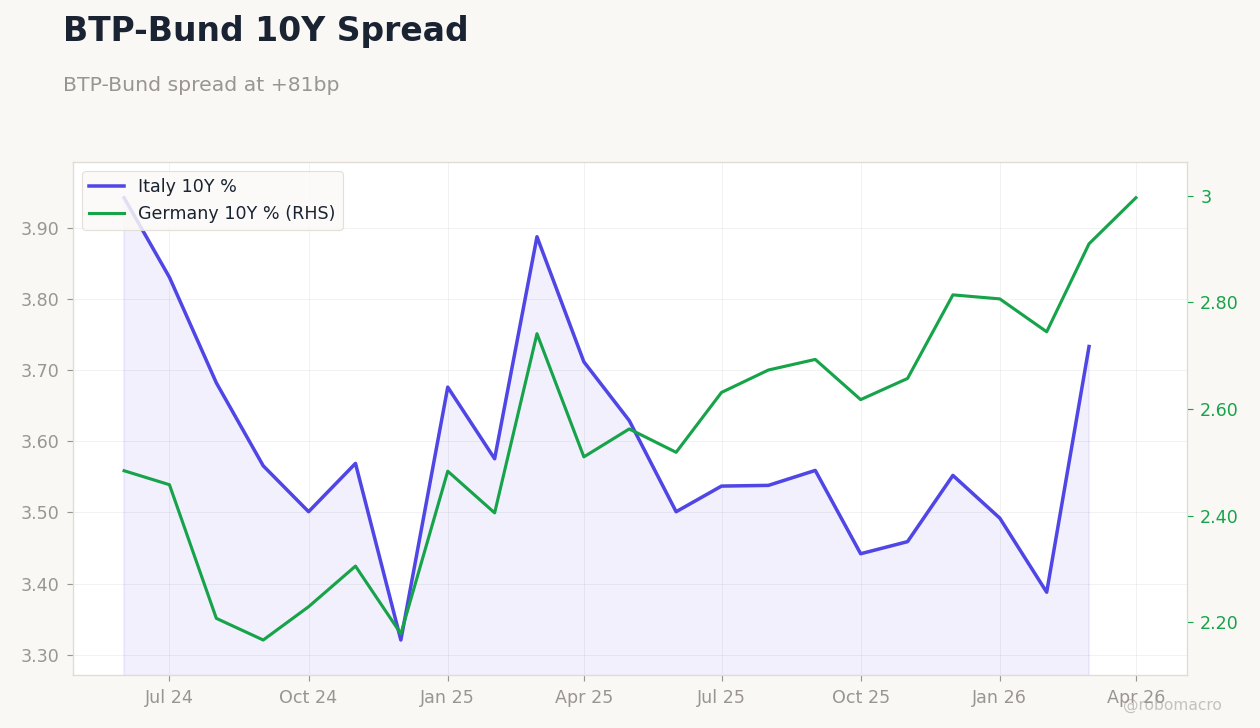

In developed markets the read-across is clearest in the United States and the Nordic bloc. US CPI and PPI both beat expectations, with upstream pressures particularly pronounced, while Federal Reserve speakers maintained a data-dependent stance without softening their vigilance language. This combination lifted the 2-year Treasury yield 24bp to 4.26% and the 10-year 23bp to 4.59%, steepening the curve and pushing the S&P 500 to a modest 0.1% weekly gain that masked broader rotation away from rate-sensitive sectors. Across the Atlantic, Norges Bank surprised with a policy-rate increase that drove EUR/NOK lower mid-week, while Sweden and Norway 10-year yields also moved higher. The Bank of England left Bank Rate unchanged and the BoJ highlighted ongoing rate-hike deliberations, pushing Japan’s 10-year yield up 23bp to 2.70%. The common DM signal is therefore one of selective tightening or extended holds rather than coordinated easing, even as labor-market data in Canada showed job losses and a rising unemployment rate that kept BoC cut expectations alive.

Published every Sunday afternoon 100% AI-generated — not financial advice